Property-backed loans charge between 3% and 6% p.a., roughly half the cost of unsecured business loans at 7% to 12% p.a.

A property-backed business loan allows business owners to use residential or commercial property as collateral to access business financing at significantly lower interest rates than unsecured loans. By pledging property, whether a private home, condo, shophouse, office or industrial unit, businesses can borrow larger amounts up to $30 million, enjoy longer tenures up to 25 to 30 years and pay interest rates of about 3% to 6% p.a.

Property-backed business loans are offered by selected banks and alternative lenders in Singapore. This page explains how property-backed financing works, compares lender options and helps determine whether securing a business loan against property is the right choice for your situation.

A property-backed business loan uses real estate as collateral to secure business financing. The property serves as security for the lender, so if the business defaults, the lender can sell the property to recover the loan. In exchange, lenders can offer lower rates, higher loan amounts and longer repayment periods than unsecured business loans.

Loan amount depends on property value and existing mortgages. Typical LTV is 60% to 80% of valuation, with own-use properties sometimes reaching 80% to 90% and investment properties commonly limited to 60% to 70%.

Formula: Maximum Loan = (LTV% x Property Value) - Existing Mortgage.

Property collateral dramatically reduces lender risk. If default occurs, the lender has a property asset to recover funds from, so rates are usually around 3% to 6% p.a. compared with 7% to 12% p.a. for unsecured business loans.

Property-backed loans charge between 3% and 6% p.a., roughly half the cost of unsecured business loans at 7% to 12% p.a.

Borrow up to $30 million based on property value. Unsecured business loans typically cap at $500,000 to $700,000.

Repay over 15 to 30 years, reducing monthly payments. Unsecured loans usually max out at 5 to 7 years.

Your property secures the loan, which improves pricing but means failure to repay can put the property at risk.

Property-backed business loans offer the lowest interest rates available for business financing, often half the cost of unsecured loans. But the trade-off is that your property is on the line. For an unsecured loan, the worst outcome is damaged credit and personal guarantee claims. For a secured loan, the worst outcome is losing your property.

Before pledging your property, ask yourself if the money you borrow is going to generate returns exceeding the loan cost and if you can service this loan even if the business revenue drops 30 to 50%. Also consider whether you have alternative assets or income to protect the property if the business struggles. The lower rate is only valuable if you do not end up losing your property asset. ![]()

![]()

Property-Backed Business Loan Eligibility

All lenders verified against Ministry of Law registry. Last updated: July 8 2026.

| Factor | Property-Backed Loan | Unsecured Business Loan |

|---|---|---|

| Interest rate | 3% to 6% p.a. | 7% to 12% p.a. |

| Maximum amount | Up to $30 million | $500,000 to $700,000 |

| Tenure | Up to 25 to 30 years | 1 to 5 years (max 7) |

| Collateral | Property pledged as security | None (personal guarantee only) |

| Approval time | 2 to 4 weeks (valuation required) | 3 to 14 days |

| Risk to borrower | Property foreclosure if default | Credit damage, personal guarantee claims |

| Monthly payment | Lower (longer tenure) | Higher (shorter tenure) |

| Best for | Large amounts, long-term needs | Smaller amounts, speed, no property |

| Loan Amount | Property-Backed (4% p.a. over 15 years) | Unsecured (9% p.a. over 5 years) |

|---|---|---|

| $500,000 | $3,698 per month = $165,640 total interest | $10,379 per month = $122,740 total interest |

| $1,000,000 | $7,397 per month = $331,460 total interest | $20,758 per month = $245,480 total interest |

Property-backed loans have lower monthly payments but higher total interest over the longer tenure. Unsecured loans cost more per month but are paid off faster. Choose based on cash flow needs and total cost tolerance.

The rate difference on a $500,000 loan is $20,000 to $30,000+ per year in interest savings compared to unsecured business term loans. The property collateral dramatically reduces lender risk.

The Enterprise Financing Scheme - Fixed Assets Loan (EFS-FAL) supports SMEs purchasing or upgrading fixed assets including commercial or industrial property, factory fit-outs, machinery and equipment.

| Feature | Details |

|---|---|

| Maximum Loan | $30 million per borrower |

| Tenure | Up to 15 years |

| Government Risk-Share | 50% standard, 70% for young enterprises |

| Interest Rate | Determined by participating bank |

| Collateral | Asset being financed |

| Property Purpose | Typical LTV | Notes |

|---|---|---|

| Own-use commercial/industrial | 80% to 90% | Higher LTV for owner-occupied business premises |

| Investment commercial/industrial | 60% to 70% | Lower LTV for rental/investment properties |

| Residential (for business loan) | 70% to 80% | Using personal property to secure business loan |

| Component | Amount |

|---|---|

| Property valuation | $2,000,000 |

| Maximum LTV | 75% |

| Maximum loan | $1,500,000 |

| Existing mortgage | ($500,000) |

| Available for business loan | $1,000,000 |

Some banks offer packages combining a commercial property loan (80% LTV) with an unsecured working capital loan (20% to 40% additional). This allows up to 100% to 120% financing, effectively zero down payment for property purchase. Hong Leong Finance offers 110% Commercial Property Plus packages.

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I can’t thank Roshi enough for helping me find the best financial institution for my DCP! The guidance and support were absolutely amazing—everything was explained clearly and tailored to my needs. Thanks to Roshi’s help, I’m now on track and completely debt-free in just 12 months! 💪🏼 I couldn’t be happier with the outcome and highly recommend Roshi to anyone looking for smart, reliable financial advice.

With the help of the ROSHI Support link to partner, I had a great experience with EZY Loan. The online application was simple, document verification was fast, and the funds were credited on the same day. The staff were professional and explained everything clearly, with no hidden fees. Overall, an excellent and hassle-free service!

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

While credit card promotions can be very attractive, knowing how to manage credit card bills is crucial. Singapore banks like DBS, UOB, and OCBC offer various payment methods for quick payments. Use options across major Singapore banks, from online banking in the comfort of your home to physical AXS machines or simply setting up auto deductions through GIRO.

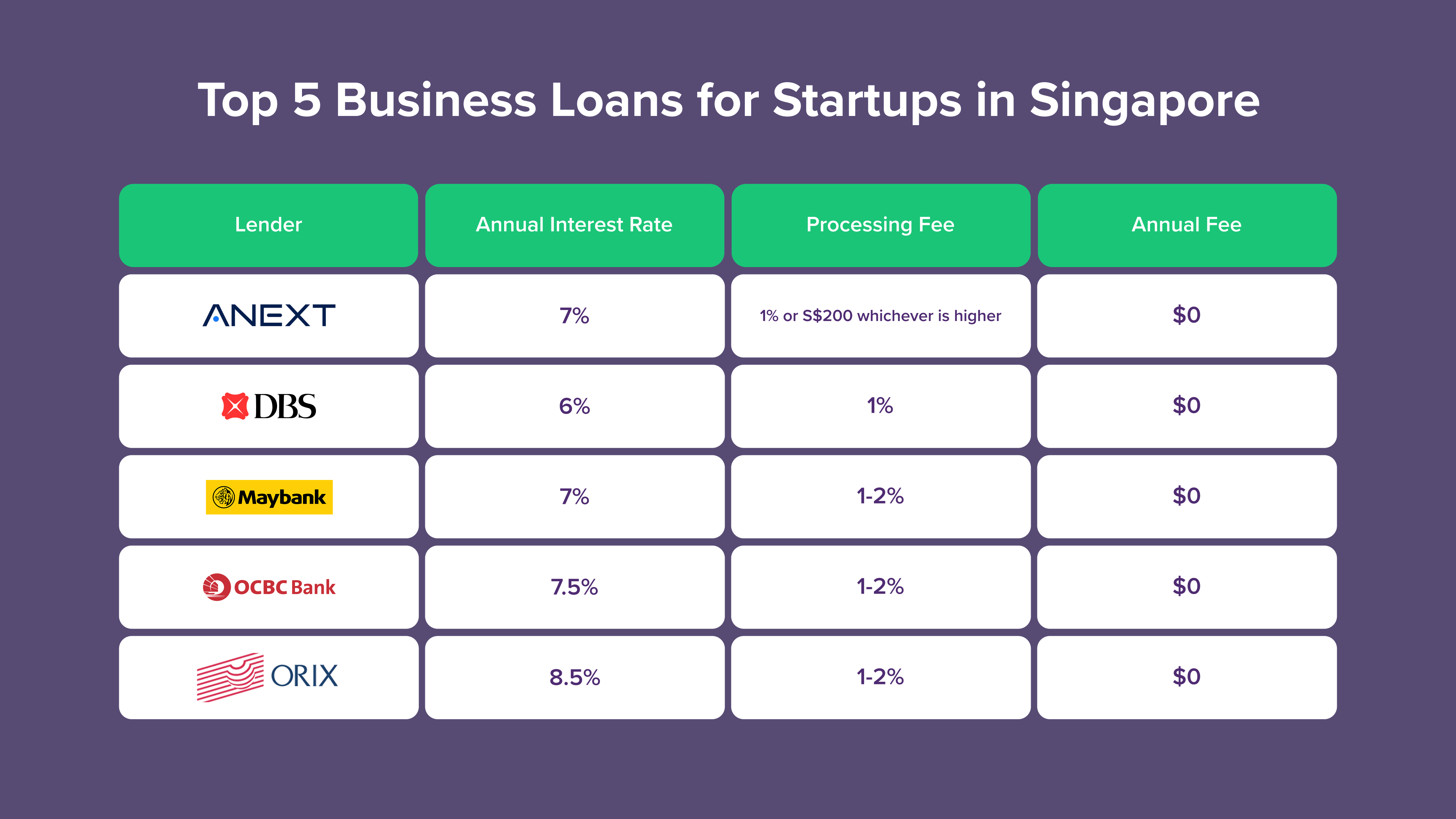

Starting a business in Singapore? Securing the right startup loan can be the spark that turns your concept into a sustainable company.

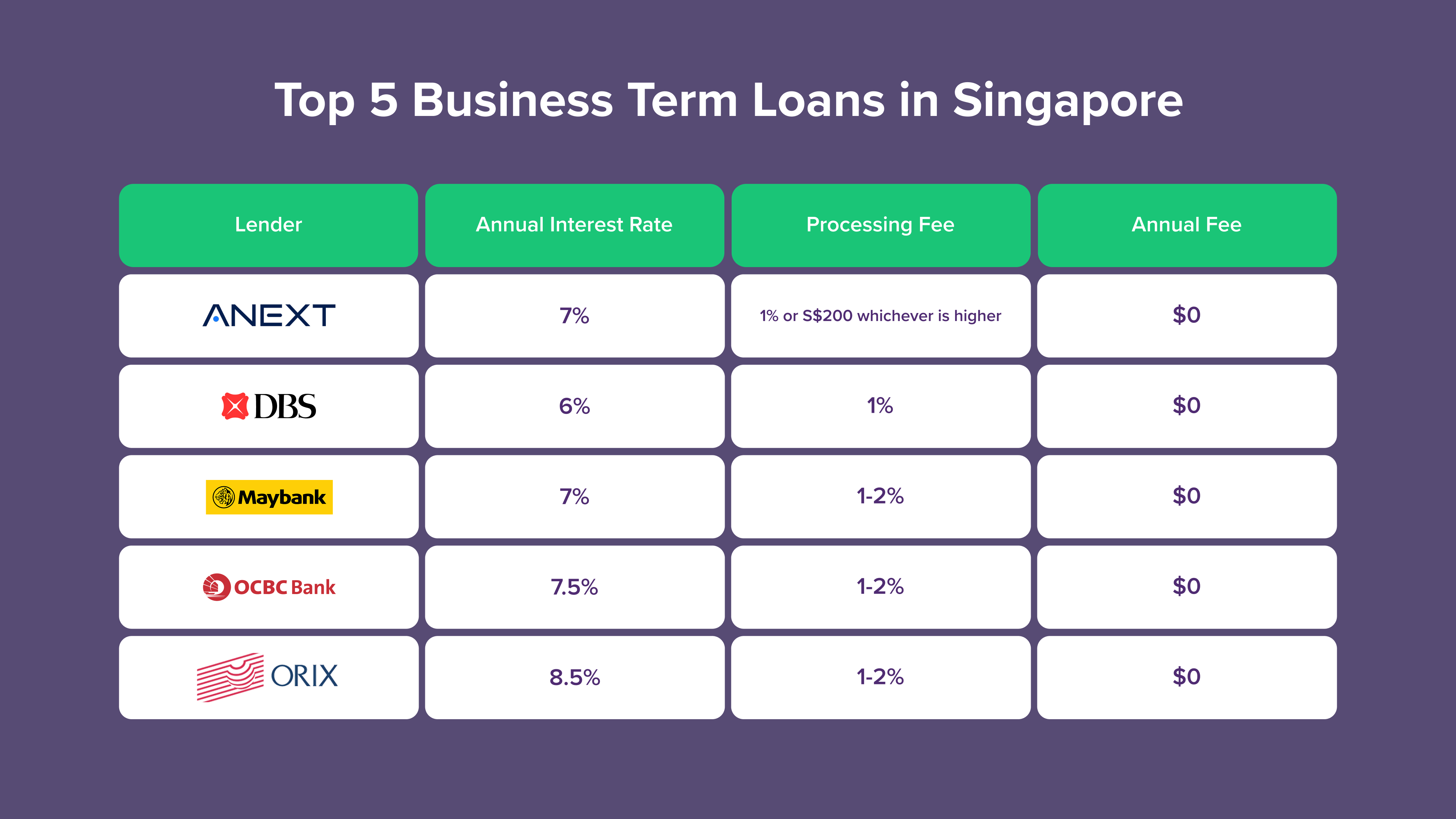

Business term loans in Singapore present a stable financing option with predictable monthly payments and competitive interest rates.

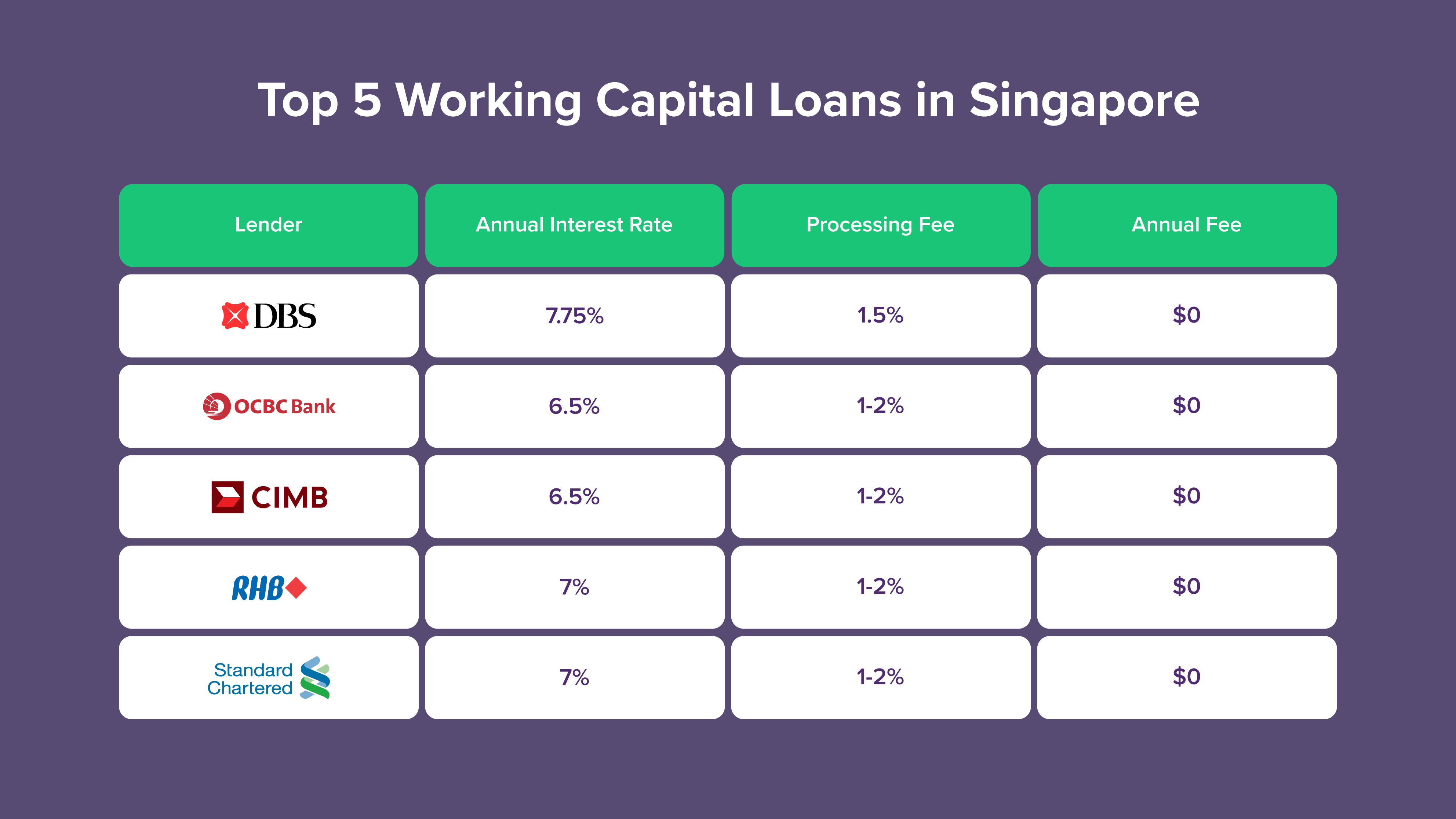

Need extra capital to manage your daily business operations? Working capital loans from Singapore’s leading banks provide a structured and low‑risk solution designed specifically for small and medium‑sized enterprises (SMEs).

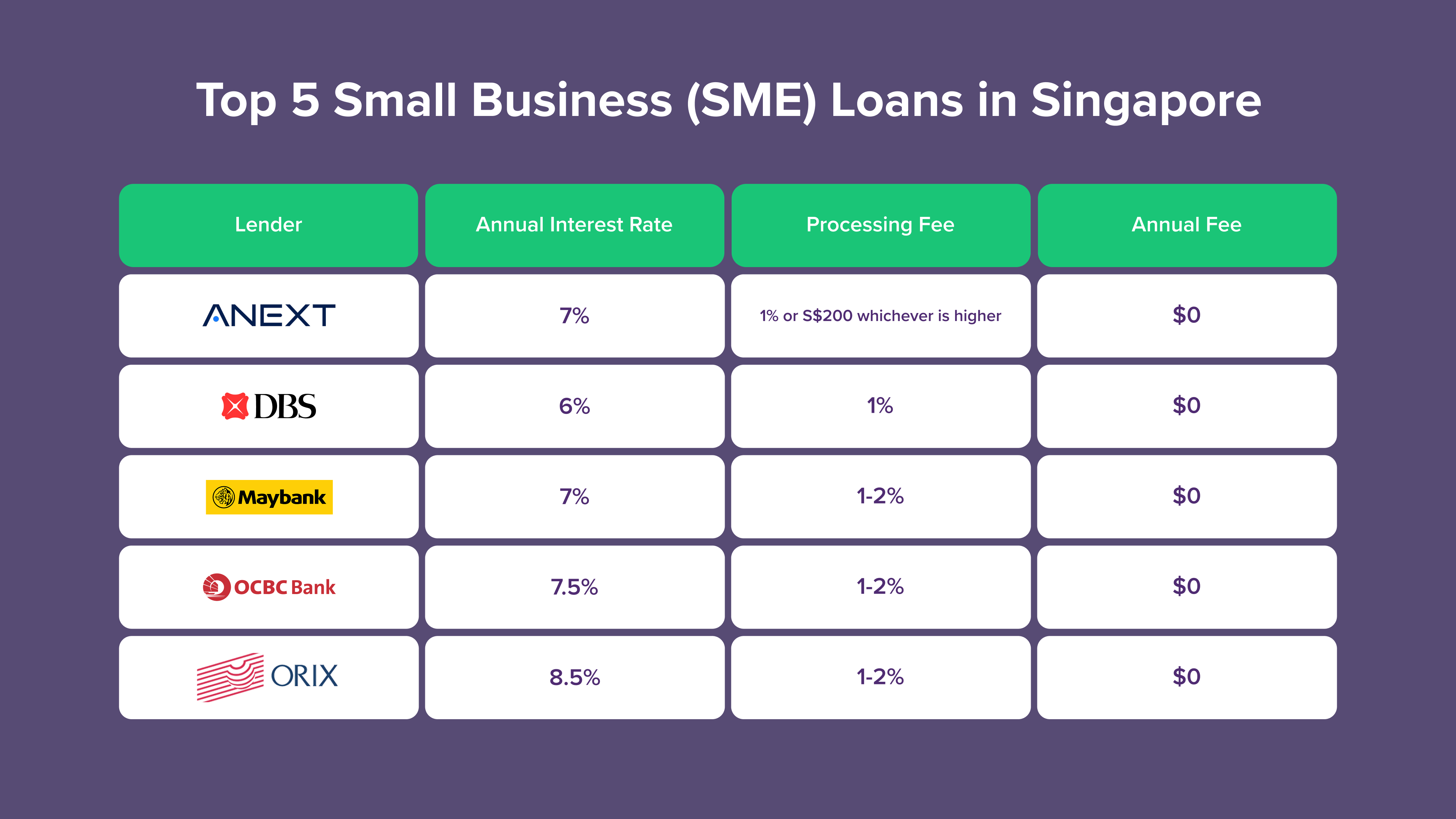

Property-backed business loans are useful for larger and longer-term funding needs, but other financing options may be more cost effective depending on timing, collateral and repayment profile. For general operational cash flow, working capital loans offer EFS-WCL government support up to $500,000 at lower rates. Small business loans provide lump-sum term financing for expansion or larger projects.

Businesses waiting on customer payments can use invoice financing to convert receivables to cash without term debt. For ongoing flexible access to funds, a business line of credit provides revolving credit without repeated applications.

Newer businesses with limited operating history can check business loans for startups. For urgent short-term gaps, bridging loans may be more suitable than pledging property for a long-tenure facility.