DCP interest rates range from 3.48% to 6% p.a. significantly lower than credit card rates of 26% to 28% p.a.

A Debt Consolidation Plan (DCP) is a structured repayment programme offered by banks in Singapore that allows borrowers to combine multiple unsecured debts such as credit card balances or personal loans into a single loan with one fixed monthly repayment at a lower interest rate. DCPs are regulated by the Monetary Authority of Singapore (MAS) and backed by the Association of Banks in Singapore (ABS designed specifically for borrowers whose total unsecured debt exceeds 12 times their monthly income.

This page explains how DCPs work, the eligibility requirements and which banks offer the most competitive rates. For debtors who do not meet the DCP threshold or prefer more flexibility this page also compares alternatives such as personal loans for debt consolidation and balance transfers.

A Debt Consolidation Plan (DCP) is a debt refinancing programme that combines all unsecured credit facilities such as credit cards and personal loans from multiple banks into a single loan with one participating bank. The DCP bank pays off all outstanding balances directly to other lenders, leaving the borrower with just one monthly repayment at a lower interest rate (typically 3% to 8% p.a. vs 26% to 28% for credit cards). DCPs were launched in 2017 by the ABS to help over leveraged borrowers regain control of their finances.

Once approved the DCP bank disburses funds directly to all other banks to pay off outstanding balances. Existing credit facilities with those banks will be suspended or closed. The borrower then repays only the DCP bank with fixed monthly instalments. Most DCPs include a complimentary credit card with a credit limit capped at one month's income for daily expenses.

DCP interest rates range from 3.48% to 6% p.a. significantly lower than credit card rates of 26% to 28% p.a.

Combine multiple debts into a single fixed monthly repayment no more juggling different due dates and amounts.

Repayment tenure ranges from 1 to 10 years. Longer tenure means lower monthly payments but more total interest.

DCPs are regulated by MAS and backed by the Association of Banks in Singapore (ABS) for consumer protection.

A Debt Consolidation Plan is designed for borrowers already in significant debt, specifically when unsecured debt exceeds 12 times their monthly income. If debt levels are below this threshold, DCP applications will be rejected. In such situations, a personal loan used to pay off high interest credit card balances or other unsecured debt may be more suitable. If the amount can be repaid quickly a balance transfer with 0% interest for 6 to 12 months could also be an alternative.

The key advantage of a DCP is the structured framework, existing credit facilities are suspended, preventing further borrowing and repayment is enforced through a single fixed instalment. For debtors who need discipline as much as lower rates a DCP can be the right tool to regain financial control. ![]()

![]()

All lenders verified against Ministry of Law registry. Last updated: July 6 2026.

Three ways to manage debt but each works differently.

| Debt Consolidation Plan | Personal Loan | Balance Transfer | |

|---|---|---|---|

| Purpose | Combine multiple unsecured debts into one loan | Any purpose, debt payoff, purchases or emergencies | Transfer credit card balance to a new card |

| Eligibility | Debt must exceed 12 times monthly income; income $20 to $120k | Anyone meeting income criteria | Existing credit card holders |

| Interest Rate | 3.48% to 8% p.a. (EIR 6% to 11%) | 3% to 10%+ p.a. (EIR 6% to 14%) | 0% for 6 to 12 months (promotional) |

| Maximum Amount | Total outstanding unsecured debt + 5% buffer | Up to 8 to 10x monthly income | Up to 95% of credit limit |

| Tenure | 1 to 10 years | 1 to 7 years | 6 to 12 months (promotional period) |

| Credit Facilities After | Suspended or closed | Unchanged | Unchanged |

| Credit Report Flag | "Debt Consolidation" code for 3 years | No special flag | No special flag |

| Best For | High debt (12 times income), need discipline | Moderate debt & want flexibility | Small balances, can repay within promo period |

| Scenario | Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| Credit Cards (min payment) | 26% p.a. | $2,000 | $108,000 plus |

| DCP (Standard Chartered Bank) | 3.48% p.a. (EIR 6.5%) | $794 | $6,700 |

| Savings with DCP | — | $1,206 per month | $101,300 plus |

A personal loan can be used to pay off high interest credit card balances. While rates are higher than DCPs 7% to 10% EIR, there's no special flag on the credit report and existing credit facilities remain open.

A balance transfer offers 0% interest for a promotional period typically 6 to 12 months. Ideal for smaller debts that can be cleared quickly but requires discipline any remaining balance after the promo period incurs high interest.

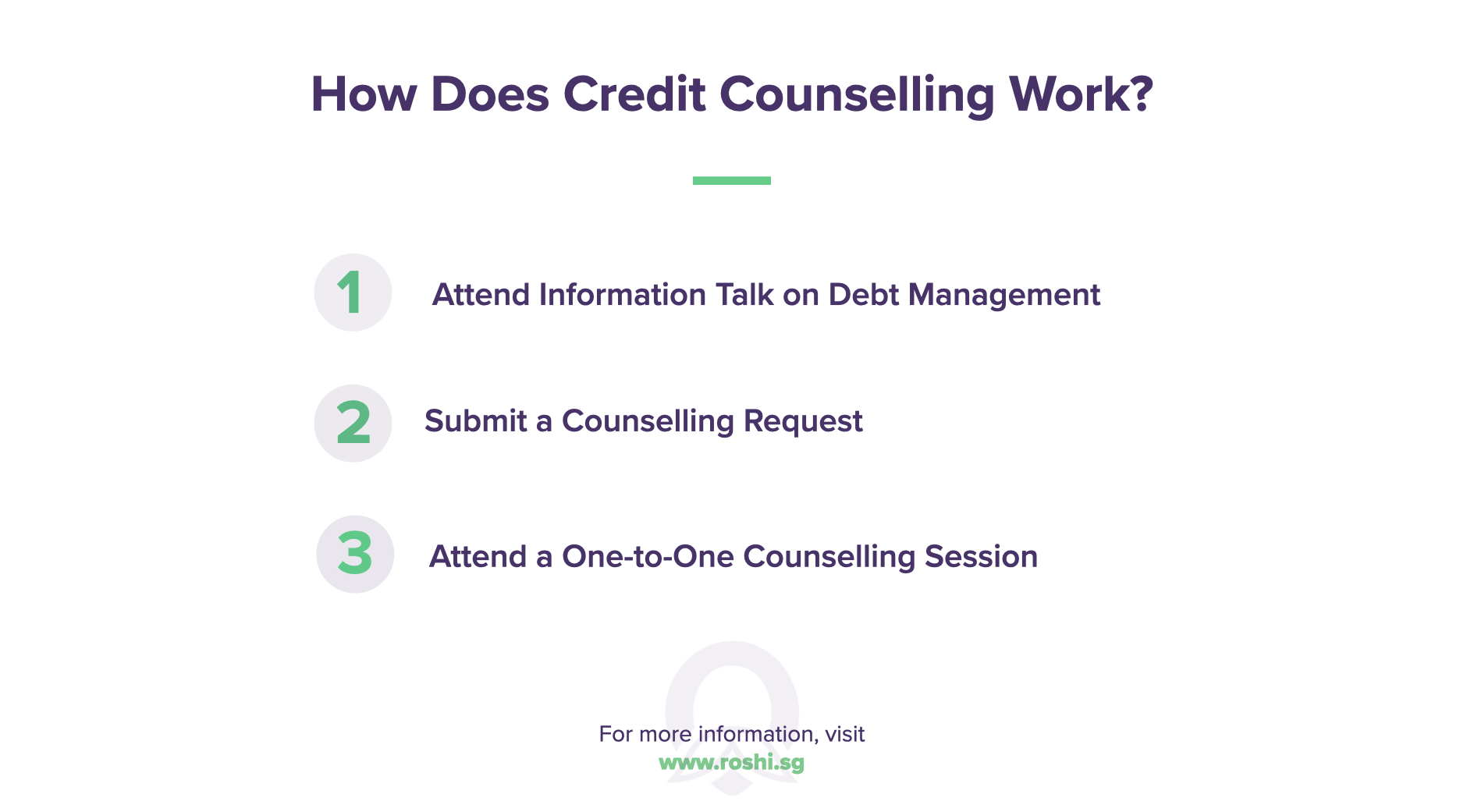

Credit Counselling Singapore (CCS) offers a Debt Management Programme (DMP) that negotiates with creditors on behalf of the borrower. This is a non-profit service for those who need structured guidance beyond what banks offer.

Bank DCPs do not cover licensed moneylender debt. Only moneylender-issued debt consolidation loans can combine both bank and moneylender debts into one facility.

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I can’t thank Roshi enough for helping me find the best financial institution for my DCP! The guidance and support were absolutely amazing—everything was explained clearly and tailored to my needs. Thanks to Roshi’s help, I’m now on track and completely debt-free in just 12 months! 💪🏼 I couldn’t be happier with the outcome and highly recommend Roshi to anyone looking for smart, reliable financial advice.

With the help of the ROSHI Support link to partner, I had a great experience with EZY Loan. The online application was simple, document verification was fast, and the funds were credited on the same day. The staff were professional and explained everything clearly, with no hidden fees. Overall, an excellent and hassle-free service!

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

Ever felt the crushing weight of debt that makes even the simplest financial decisions feel like a high-wire act?

![Can’t Pay Back Your Credit Card Debt? Definitive Singapore Guide [Updated 2026]](https://www.roshi.sg/wp-content/themes/roshi/images/insights/paying-off-your-credit-card-debt-guide.png)

In a time of financial challenge, it’s easy for credit card payments to get missed

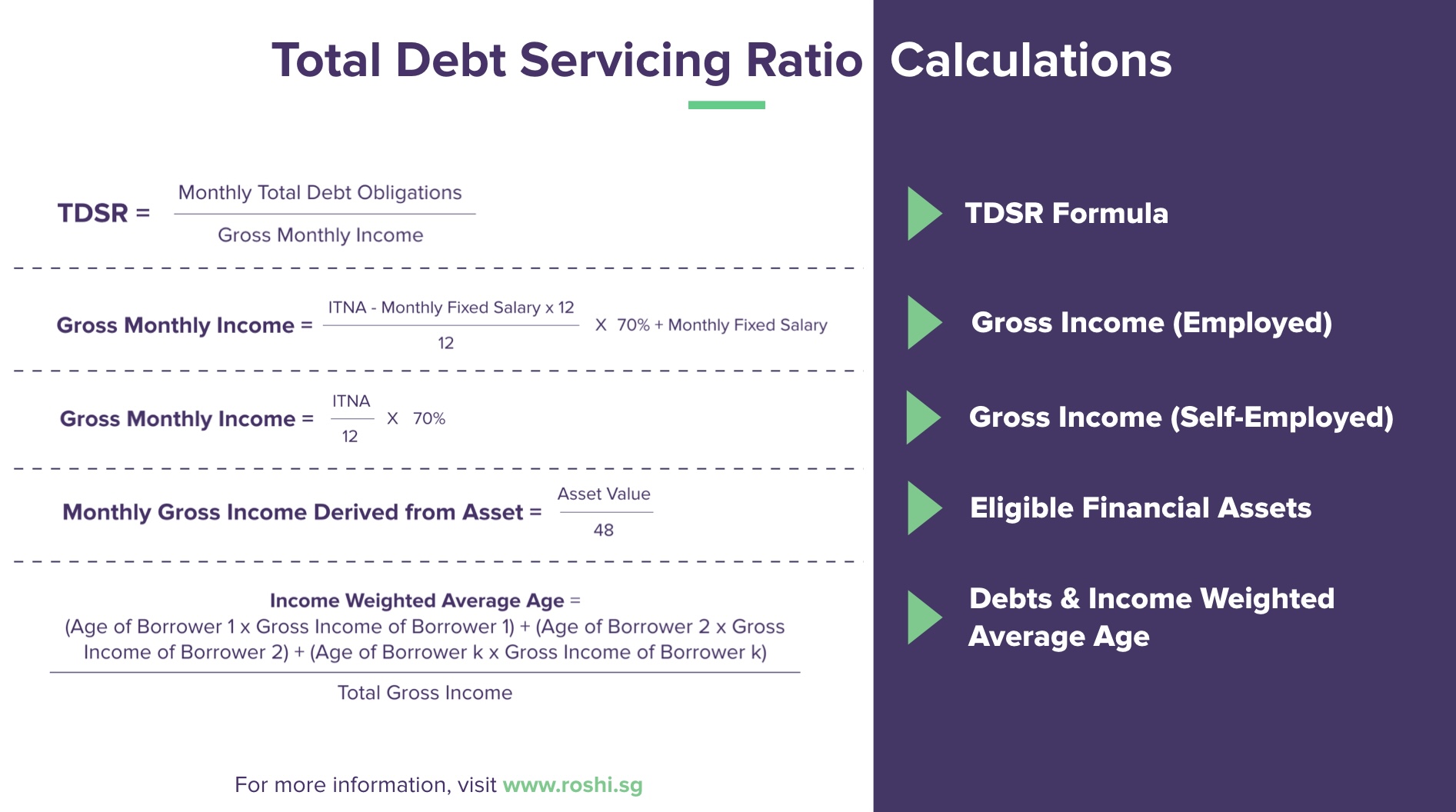

Getting a housing loan isn’t as simple a process as it was in the past. Things like a 40-year loan period is but a distant memory, and now the Total Debt Servicing Ratio (TDSR) is how we regulate a borrower’s maximum property loan eligibility, regardless of purchase or refinancing.

Many people in Singapore need to learn that credit counselling is a solution to helping them organise their finances.

A Debt Consolidation Plan is designed for borrowers whose unsecured debt exceeds 12 times their monthly income but it's not the only way to manage debt. For those who don't meet the DCP threshold, a personal loan can be used to pay off high interest credit card balances at a lower rate without the restrictions that come with a formal DCP. A balance transfer offers 0% interest for a promotional period of 6 to 12 months and works best for smaller amounts that can be cleared quickly before regular interest kicks in.

To plan a debt payoff strategy, check out our personal loan calculator that estimates monthly repayments across different amounts and tenures while our credit card repayment calculator shows how long it will take to clear existing balances based on current payment levels. For bank specific personal loan rates and features reviews are available for DBS, OCBC, UOB, Standard Chartered, HSBC, CIMB, and Maybank as well as from digital banks such as Trust Bank and GSX.

Mastering your loan moves starts with understanding the real cost of borrowing. We believe in empowering you with the right knowledge to make smart financial choices, not quick fixes that lead to debt traps. Our commitment is helping you borrow wisely and stay in control of your money.

Read Our Borrowing Guide

.Don't be a fool! #roshi #singapore #lending #borrowing

Trust the original! #roshi #singapore #lending #borrowing

.Don't be a fool! #roshi #singapore #lending #borrowing

Trust the original! #roshi #singapore #lending #borrowing

.Don't be a fool! #roshi #singapore #lending #borrowing