All Critical Factors When Deciding Between SORA and SIBOR [Definitive Guide]

![All Critical Factors When Deciding Between SORA and SIBOR [Definitive Guide]](https://www.roshi.sg/insights/wp-content/uploads/2026/01/trinh_thanh.png)

Fact-checked

Fact-checked

![All Critical Factors When Deciding Between SORA and SIBOR [Definitive Guide]](https://www.roshi.sg/insights/wp-content/uploads/2022/11/SORA-Single-Rate-Timeline-Singapore.001.jpeg)

Click Image to Zoom

At a glance...

Have you considered switching from Singapore Interbank Offered Rate (SIBOR) to Singapore Overnight Rate Average (SORA) for your home loan interest rate? If you’re wondering how this transition might affect you, keep reading to learn the five most important factors to consider.

SORA or SIBOR: What’s the difference?

The SORA rate is based on the volume-weighted average of borrowing transactions in Singapore’s unsecured overnight interbank SGD cash market.

SIBOR, on the other hand, is based on interest rates banks charge other banks for borrowing unsecured funds on the Singapore interbank cash market. This rate is based on the average bank rates, making this process less transparent than SORA.

Although the volatility of SIBOR and SORA are similar, SORA does allow consumers to compare bank loans more efficiently.

Comparing between a SIBOR and SORA benchmark rate:

Type |

SIBOR Rate |

SORA Rate |

|---|---|---|

1-month |

0.302 |

0.189 > |

3-month |

0.437 |

0.172 |

6-month |

0.593 |

0.153 |

12-month |

- |

- |

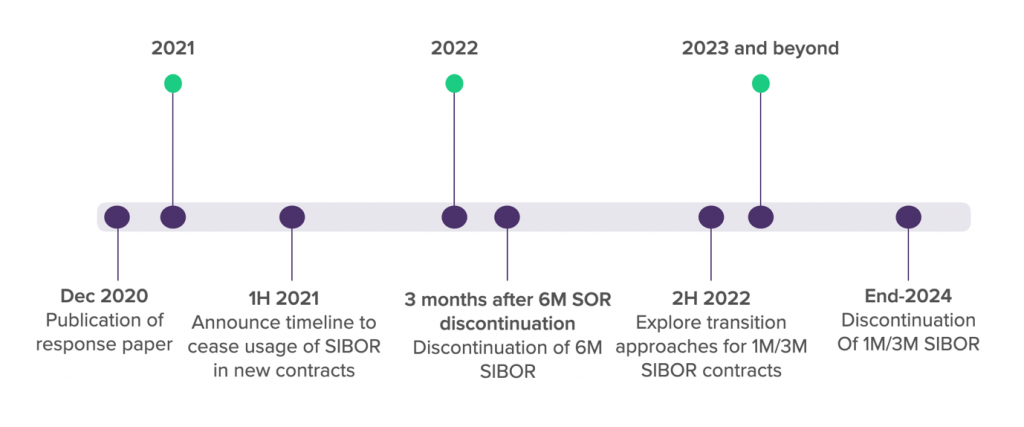

Why is SORA replacing SIBOR?

There has been a proposed shift to transition to a single rate: SORA. A SORA-based system would improve the integrity of the SGD financial market as well as benefit the customers and financial institutions. This is because the SORA system will avoid market fragmentation, aid pricing transparency, and promote financial market expansion.

The SORA rates are also considered more stable than SIBOR rates because it is based on bank transactions, and no expert or biased judgment is required for this process.

Considerations

Many banks have begun to offer SORA home loans in addition to their SIBOR-pegged loans. So far, the 3-month SORA home loan is the most popular option. The only issue is there are fewer SORA options than SIBOR options as of yet.

What is the impact on my current SIBOR-pegged home loan?

If you currently have a SIBOR home loan, you do not need to take any immediate action. Banks and financial institutions plan to convert SIBOR loans into SORA loans in the next few years. This was previously done with SOR home loans. The timeline of this transition will not immediately impact your current rate. Once your bank is ready for the shift, they will contact all customs with advanced notice before switching.

When will I be forced to switch to a SORA home loan?

Once SIBOR is no longer an option, your bank will no longer be able to offer it to you. Therefore, you will need to replace your SIBOR loan by the end of 2024. SORA home loans are still in the initial stages, and this transition will not happen immediately, so you will have plenty of time to sort out your shift. If you are unhappy with your current SIBOR loan, we suggest taking the leap and switching to SORA earlier.

What are my options if I currently have a SIBOR-pegged loan?

Due to the SIBOR-pegged loans having a low-interest rate, it may be best for you to keep your current package for the time being. Mainly because the SIBOR rates are the lowest they have been in the past seven years. We recommend waiting for word from your bank before switching to an alternative plan.

Should I refinance to a SORA-pegged home loan now?

Although SORA will significantly benefit our future, there is still much value in SIBOR. Let’s give you an example to understand why staying with SIBOR for the time being may be beneficial to you. If your current total housing loan interest rate is under 0.85%, it does not make sense to switch, as SORA’s lowest rate starts at 0.86%.

Bank |

Loan Type |

Year 1 |

|---|---|---|

Limited Promo* |

3-month SORA |

0.80% |

Limited Promo* |

1-month SORA |

0.81% |

DBS |

3-month SORA |

0.96% |

HSBC |

1-month SORA |

0.86% |

Citibank |

1-month SORA |

0.89% |

Standard Chartered |

3-month SORA |

0.86% |

OCBC |

1-month SORA |

0.96% |

Should I switch from SIBOR to a fixed-rate home loan instead of SORA

A fixed rate is stable, but despite the volatility of SIBOR, they are still a better option for homeowners looking for lower monthly payments. You also have to keep in mind that fixed-rate home loans transition to floating-rate loans after the lock-in period is over. With SIBOR, you risk a change that equates to a slightly higher interest rate, but it’s unlikely. When it comes to SORA rates, there are new rates daily, so you’ll want to keep an eye out for when the rates might benefit you to transition.

Considerations

Switching to fixed-rate loans might be good if you expect interest rates to rise for the next two to three years. Although, if the interest rates fall, you would be disadvantaged because fixed-rate loans are often pegged at a higher interest rate than SIBOR and SORA. Currently, the lowest interest rate available for SORA is 0.80%, while the lowest 2-year fixed rate is 1.05%. So, if you feel like paying slightly more each month to ease the headache of increasing interest rates, then you may prefer to get a fixed-rate loan.

Current Home Loan Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.

Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

*Today's Mortgage Rates - 02 July 2026

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 02 July 2026

Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 0 year | 1.60% |

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| RHB | 0 year | 1.70% |

| OCBC | 2 years | 1.70% |

| Bank of China | 0 year | 1.74% |

| DBS | 0 year | 1.79% |

*Today's Mortgage Rates - 02 July 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 02 July 2026