EFS-WCL provides 50% to 70% government risk sharing through Enterprise Singapore, improving approval chances for eligible SMEs.

A working capital loan provides financing for day to day business operations such as payroll, rent, utilities, inventory, supplier payments and other recurring expenses. Unlike term loans used for expansion or asset purchases, working capital loans address the cash flow gaps that occur between paying expenses and receiving revenue.

In Singapore, SMEs can access working capital financing through the government backed Enterprise Financing Scheme (EFS-WCL) offering up to $500,000 with 50% to 70% government risk sharing furthermore major banks and alternative lenders also offer working capital loans This page explains how working capital loans work, compares options and covers related financing like invoice financing and business lines of credit that also serve operational cash flow needs.

Working capital is the cash a business needs to fund daily operations, basically the gap between current assets such as cash, receivables, inventory and current liabilities such as payables or short-term debt. A working capital loan provides funds specifically to cover this gap, ensuring the business can pay staff, suppliers and overheads while waiting for customers to pay.

EFS-WCL provides 50% to 70% government risk sharing through Enterprise Singapore, improving approval chances for eligible SMEs.

Borrow up to $500,000 under EFS-WCL. Bank and alternvative lender limits vary based on revenue and creditworthiness.

EFS-WCL rates range 7% to 10% p.a. EIR depending on bank assessment. Alternative lenders charge 9% to 15% for faster approval.

Choose term loan for fixed payments), revolving facility draw as needed or invoice financing tied to receivables.

A profitable business can still fail from poor cash flow management. You invoice $100,000 in sales but customers pay in 60 to 90 days while rent, payroll and suppliers are due now. This timing mismatch is exactly what working capital financing solves. The key metric is your cash conversion cycle, basically how long it takes to turn inventory and receivables into cash. If that cycle is 90 days but your payables are due in 30 days, you have a 60 day funding gap.

My advice, size your working capital facility to cover this gap not your total expenses. And choose the structure that matches your cash flow pattern. A term loan for predictable needs, a revolving facility for fluctuating needs or invoice financing if receivables are your main bottleneck. ![]()

![]()

Working Capital Loan Eligibility

All lenders verified against Ministry of Law registry. Last updated: July 2 2026.

Different structures serve different cash flow patterns.

The government backed option with risk sharing to improve approval chances.

| Working Capital Term Loan | Invoice Financing | |

|---|---|---|

| Structure | Fixed amount, fixed repayment | Tied to specific invoices |

| Interest | Charged on full loan amount | Charged only on invoices financed |

| Repayment | Monthly over 1 to 5 years | When customer pays invoice |

| Flexibility | Fixed facility | Scales with sales volume |

| Best for | Predictable ongoing needs | Businesses with long payment terms |

| Providers | Banks, digital lenders | OCBC, DBS, Funding Societies, Validus |

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I can’t thank Roshi enough for helping me find the best financial institution for my DCP! The guidance and support were absolutely amazing—everything was explained clearly and tailored to my needs. Thanks to Roshi’s help, I’m now on track and completely debt-free in just 12 months! 💪🏼 I couldn’t be happier with the outcome and highly recommend Roshi to anyone looking for smart, reliable financial advice.

With the help of the ROSHI Support link to partner, I had a great experience with EZY Loan. The online application was simple, document verification was fast, and the funds were credited on the same day. The staff were professional and explained everything clearly, with no hidden fees. Overall, an excellent and hassle-free service!

Great offers with low interest rates. Better than Lendela! Plus there is a 0.50% cashback and $20 grocery voucher upon approval and disbursement of loan!

While credit card promotions can be very attractive, knowing how to manage credit card bills is crucial. Singapore banks like DBS, UOB, and OCBC offer various payment methods for quick payments. Use options across major Singapore banks, from online banking in the comfort of your home to physical AXS machines or simply setting up auto deductions through GIRO.

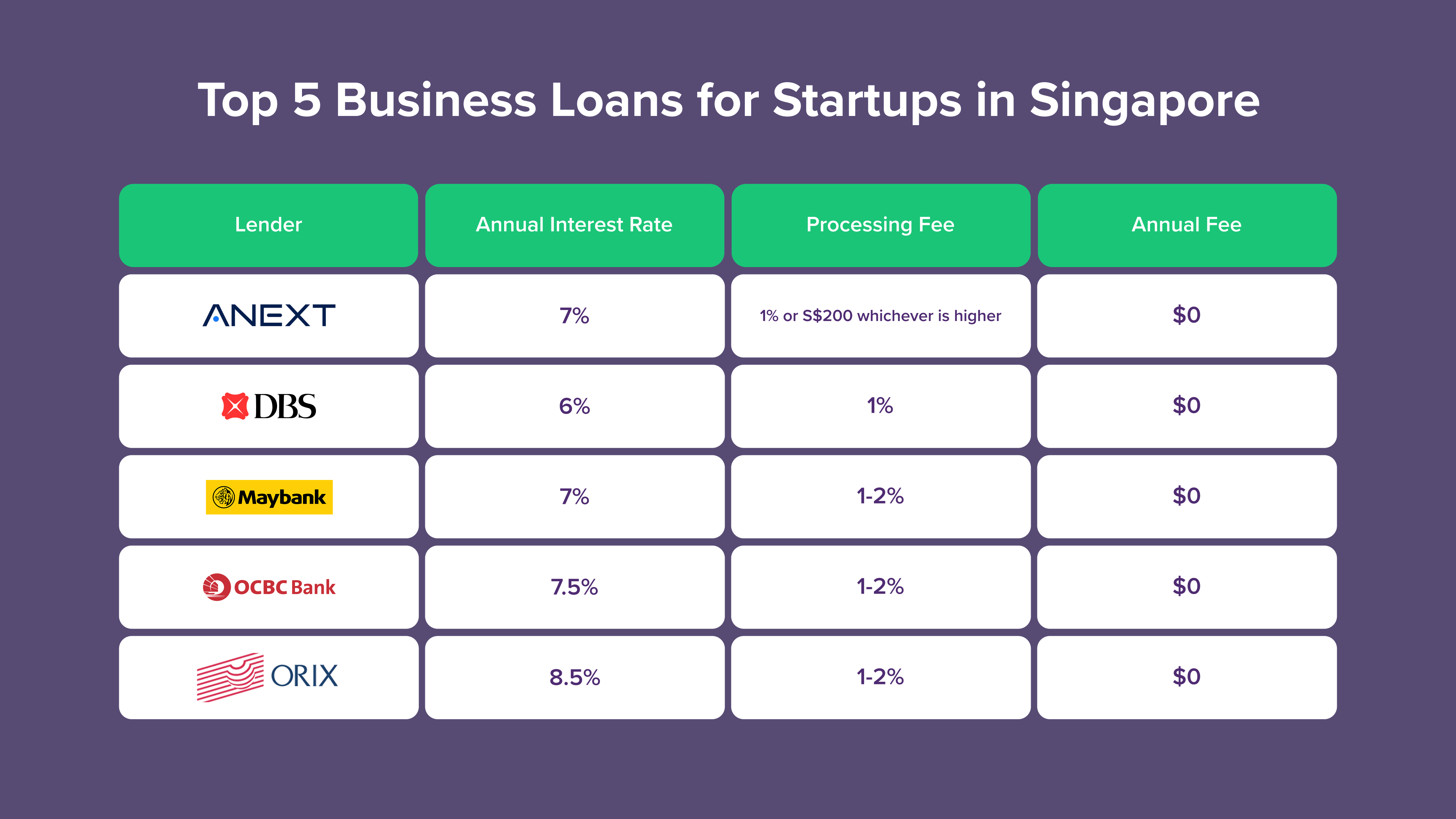

Starting a business in Singapore? Securing the right startup loan can be the spark that turns your concept into a sustainable company.

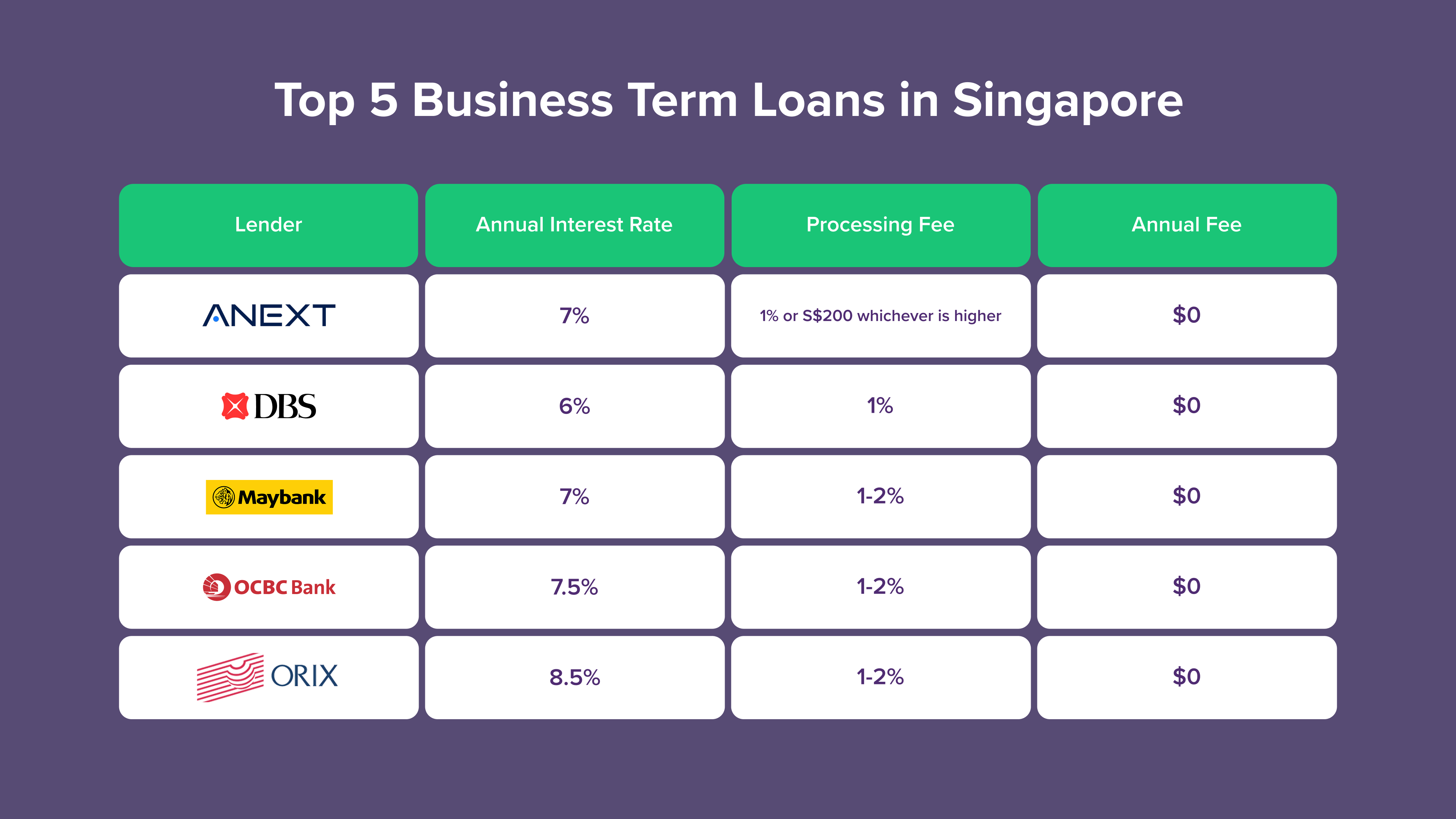

Business term loans in Singapore present a stable financing option with predictable monthly payments and competitive interest rates.

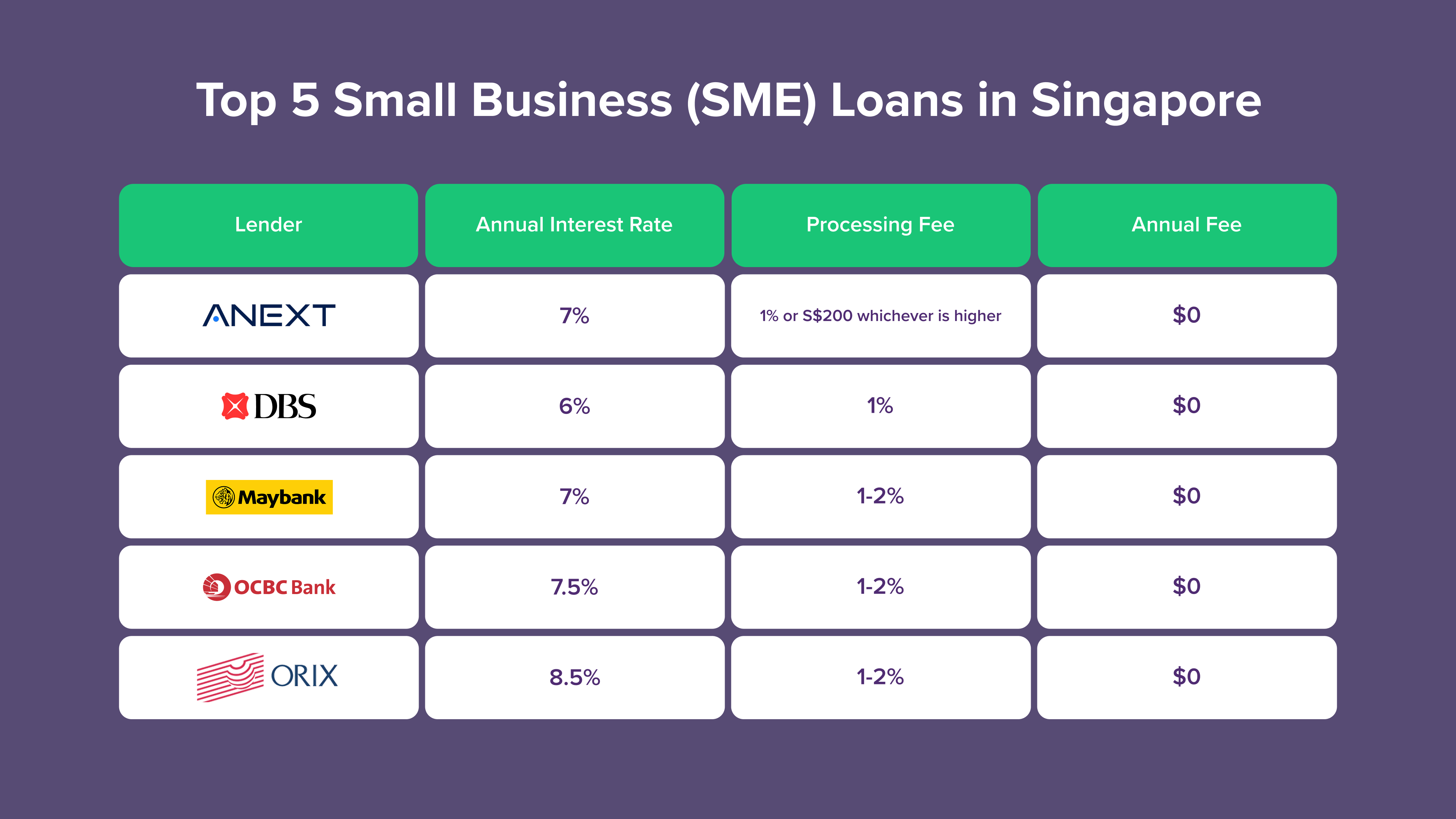

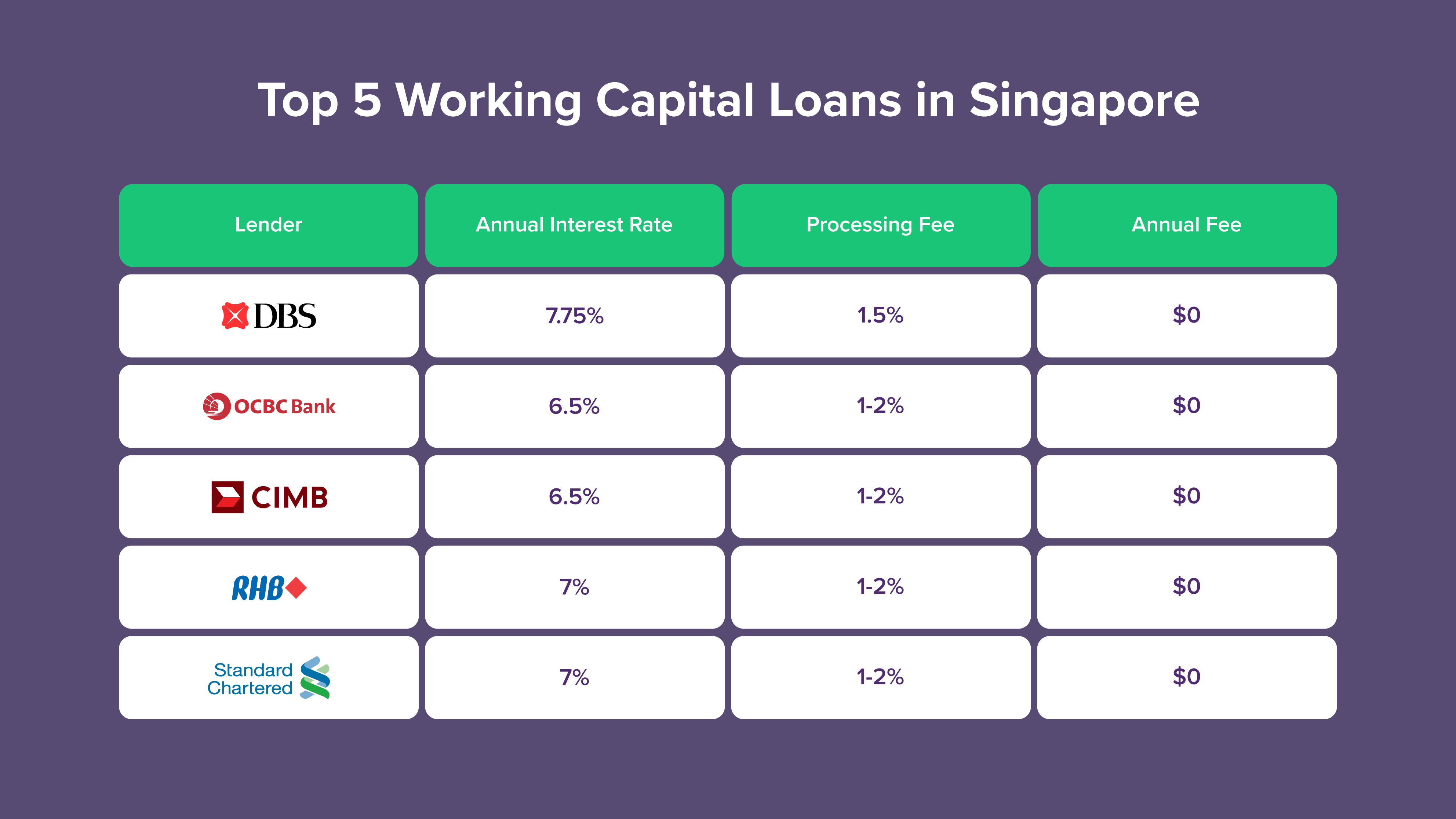

Need extra capital to manage your daily business operations? Working capital loans from Singapore’s leading banks provide a structured and low‑risk solution designed specifically for small and medium‑sized enterprises (SMEs).

Working capital loans address operational cash flow needs but depending on your business situation other financing options such as regular business term loans may be more suitable.

For a general purpose lump sum to fund expansion or larger projects, small business loans offer flexible terms. Businesses needing ongoing flexible access to funds can explore business lines of credit with revolving facilities.

For urgent short term needs while awaiting receivables or other payments, bridging loans provide temporary financing over 3 to 24 months. Companies purchasing equipment, machinery or vehicles can access equipment financing with lower rates secured against the assets.

Newer businesses with limited operating history can check business loans for startups with more accessible eligibility requirements. For bank specific working capital loan packages, bank reviews are available for DBS, OCBC, Standard Chartered, Maybank, CIMB, Ethoz and Funding Society.