HDB Loan vs Bank Loan? The Ultimate HDB Financing Comparison

Fact-checked

Fact-checked

Click Image to Zoom

At a glance…

Your home is going to be one of the biggest purchases you will ever make in your life. If you’re taking a loan to finance it, then that loan is probably going to be one of the biggest – and therefore also important. The first choice you have to make is straightforward: will you take the HDB’s concessionary loan, or apply for one from a bank? The reality is not so simple, of course. This is a decision that hinges on your financial situation, as well as your personal preferences.

If you’re averse to risk, or prefer having the possibility of paying off the loan early as an option, then the HDB loan is the better choice for you. The HDB loan requires a lower downpayment on your house and missed repayments are given more leniency. However, HDB loans have a fixed, high interest rate, which may be tougher to handle for those with a smaller cash flow budget.

On the other hand, if you would prefer a lower interest rate, bank loans may be the thing for you. Of course, that lower interest rate comes with certain terms and conditions, including but not limited to a validity of two to three years, a necessity to pay off at least 5% in cash, and an early repayment penalty of 1.5%.

It’s vital that you give due consideration before you opt for one or the other, and ROSHI is here to help you out!

First, an introduction to HDB loans. An HDB loan is a concessionary loan intended as a provision for Singaporeans. The current interest rate for an HDB loan is 2.6%, and the loan comes with restrictions.

So, you’ve decided to take the plunge and apply for a HDB flat. Congratulations! The next step: a home loan! Unless you’re one of those exceedingly affluent few who can afford to settle your entire home purchase with cash upfront, you’ll need a loan. You’ll primarily have two options for loan providers: the HDB, or a bank. To help you make your choice, let’s dive into the pros and cons of both types of loans so that you’re familiar with them.

Important Tip

Before we get started, it’s important to point out a key distinction about the loans from the HDB: obvious as it may sound, the HDB concessionary loan can only be taken if you’re purchasing a HDB property. Therefore, this comparison is only for those of you looking to buy a new HDB BTO unit, or an existing older resale unit.

The HDB concessionary loan

Before we can compare the differences between HDB and bank loans, here are some of the facts and figures for both:

- Interest rate: 2.6% p.a.; the rate is pegged at 0.1% above the current CPF OA interest rate, which right now stands at 2.5% p.a.).

- Loan-to-value (LTV) limit: Up to 90% of the purchase price for new flats. For resale flats, the limit is up to 90% of the resale price or value, depending on which is lower. If the remaining flat lease cannot cover the youngest buyer until the age of 95 at the time of application, the LTV will be prorated from the maximum 90%.

- Minimum downpayment: 10% (all of which can be covered using funds from your CPF)

- Early repayment: No penalty

- Minimum income: Would-be buyers’ total combined monthly income must be less than $14,000

The total amount offered will vary depending on the buyers’ age, monthly income, and overall financial situation. If you’ve opted to buy an uncompleted flat, such as a new BTO unit, the HDB will reassess your financial standing closer to the completion date.

Considerations

Want to know if you’re eligible for the HDB loan? Check out What Do HDB Flat Buyers Like You Need To Know About HDB Loan Eligibility (HLE) to learn more about the HDB loan eligibility criteria, and how it applies to you!

Bank loans

Any financial institution regulated by the Monetary Authority of Singapore can offer home loans. Here are some of the key points to consider:

- Interest rate: Unlike the HDB loan, bank interest rates can vary quite widely depending on many different factors, from matters like the current economic climate, down to simple details like the duration and size of the loan. Current interest rates typically range between 1.2% to 3% p.a.

- LTV limit: Up to 75%

- Minimum downpayment: 25% (of which at least 5% must be made in cash)

- Early repayment: Will incur penalties

- Minimum loan amount: Required

Key comparisons between the HDB loan vs bank loans

1. HDB’s stable interest rate vs banks’ usually lower interest rate

The HDB pegs its loan interest rate to the CPF OA’s interest rate, which has historically been a stable environment, and any changes is simply a reflection of changes to the CPF’s interest rate.

Banks, on the other hand, usually charge lower than the HDB’s 2.6% p.a. interest rate, though it varies depending on factors like the duration and amount of the loan. Given that interest rates fluctuate regularly, you’re unlikely to be guaranteed the same interest rates for more than a few years with a fixed loan package. Anything after those guaranteed years will be entirely at the whim of the interest rate climate in the future – it might get lower, if you’re fortunate, but it also might increase, potentially beyond the HDB’s stable rate. Banks may also provide additional perks to their loans in order to attract customers, though this also means there’s a wide range of loan packages out there and it can get confusing for one less knowledgeable on the details.

2. HDB’s smaller minimum downpayment amount

The biggest benefit of the HDB loan is arguably the fact that its minimum downpayment is only 10%, meaning you can take a loan of up to 90%. Combined with the fact that you can use funds from your CPF OA to cover the downpayment. Provided that you have enough in your CPF account, it is entirely possible that you may not have to fork out any cash for your home purchase.

The downpayment most banks require for you taking a loan with them is about 25% of the total price, of which at least 5% has to be made in cash, though the remainder 20% can be made with your CPF OA funds. This can be a significant upfront cost that could substantially impact any other financial commitments you intend to take in the future.

3. Early repayment penalty

Unlike a bank loan, you may pay off the HDB loan early without incurring any penalties. Why would you do that? Well, your financial situation might improve from when you first applied for the loan – you might have gotten a promotion, or be relieved from other financial obligations, thus giving you a greater repayment capacity. Doing so would reduce the total amount of interest you would need to pay on the loan and might help you to eventually pay off the entire debt sooner. With the HDB loan, there are no penalty charges if you opt to pay more instead of being committed to the repayment scheme, thus potentially allowing you to pay off the loan earlier.

Meanwhile, bank loans usually have a fixed commitment, which means it is not as easy for you to pay off your loan in advance.

4. HDB loans can be switched to a bank loan

As the HDB loan does not have a fixed period in which your commitment is locked in, you can refinance the loan through a bank further down the line. Furthermore, you can take advantage of the lower minimum downpayment at the time of your purchase, and then a few years later once you’ve paid off enough to offset the difference in principal, you could then switch to a bank loan with lower interest rates.

Important Info

Note, however, that this conversion is one way only. Once you’ve converted your HDB loan to a bank loan, you cannot then switch it back to a HDB loan, although you may have other refinancing options with other banks.

5. HDB loans are more lenient on your repayments

Bank loans will not wait, no matter how dire your circumstances become. On the other hand, an HDB loan will be more lenient and keep trying to defer your repayments for as long as possible to give you chances.

While repayment with HDB loans are more lenient, make no mistake, failing to pay off your loan will still have repercussions lying in wait.

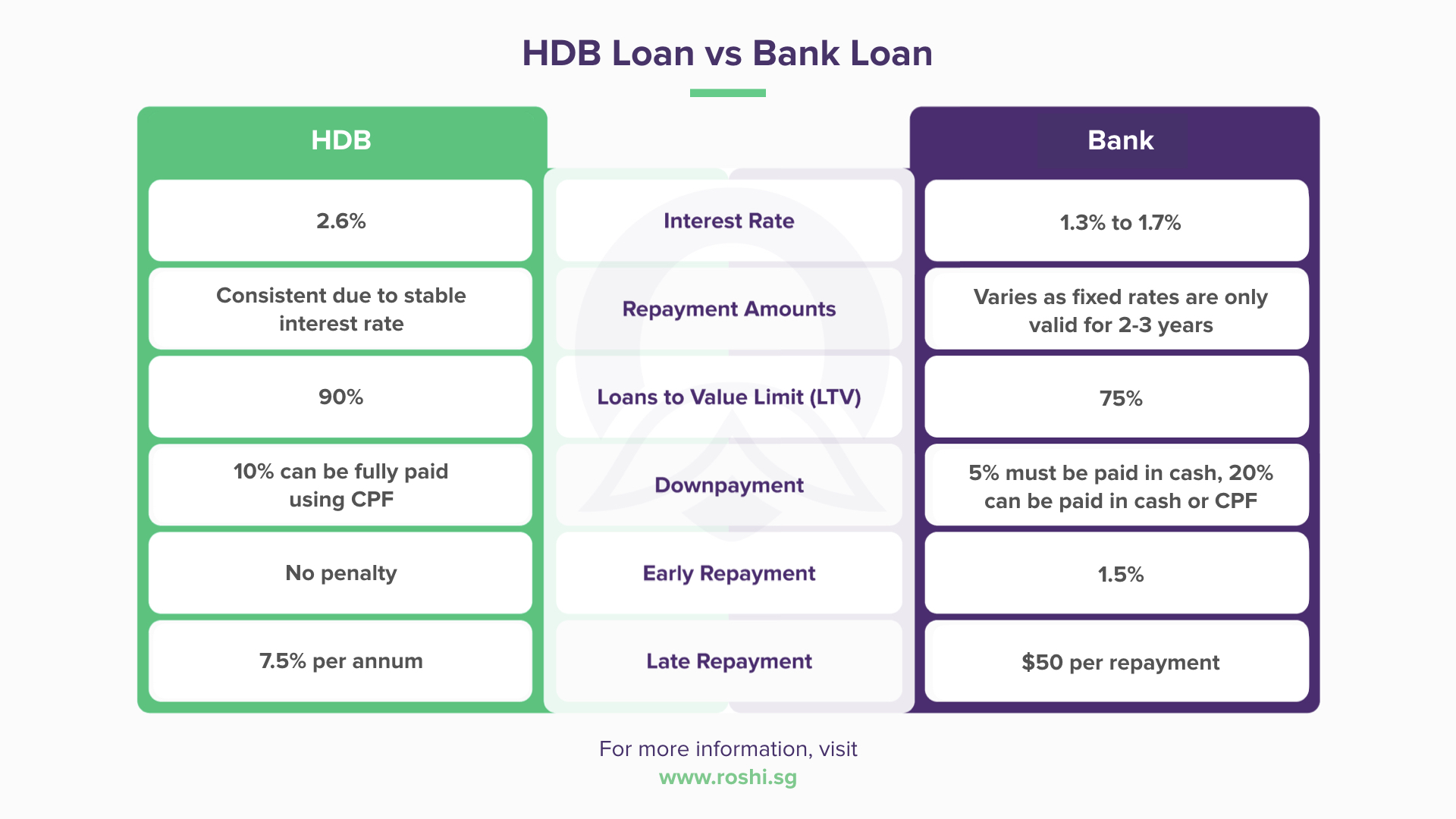

To summarise, these are the differences again between the two types of loans:

| HDB | Bank Loan | |

|---|---|---|

| Interest Rate | 2.6% | 1.3% to 1.7% |

| Repayment Amounts | Consistent due to stable interest rate | Varies as fixed rates are only valid 2-3 year |

| Loan to Value Limit(LTV) | 90% | 75% |

| Downpayment | 10% can be fully paid using CPF | 5%must be paid in cash, 20% can paid in cash or CPF |

| Early Repayment | No Penalty | 1.5% |

| Late Repayment | 7.5% per annum | $50 per repayment |

Now that you’re better acquainted with home loans from the HDB and banks, the choice is yours!

This is a crucial part of getting your dream home, and ROSHI will continue to help you throughout the process if you’ve taken the HDB loan, as our home loan comparison tool will always keep you up to date with the best home loans on the market for when you decide to switch out from the HDB loan.

Current Home Loan Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.

Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

*Today's Mortgage Rates - 21 May 2026

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 0 year | 1.60% |

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| RHB | 0 year | 1.70% |

| OCBC | 2 years | 1.70% |

| Bank of China | 0 year | 1.74% |

| DBS | 0 year | 1.79% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 21 May 2026