Can’t Pay Back Your Credit Card Debt? Definitive Singapore Guide [Updated 2026]

![Can’t Pay Back Your Credit Card Debt? Definitive Singapore Guide [Updated 2026]](https://static.roshi.sg/roshi-wp-insights/2026/01/trinh_thanh.png)

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

In a time of financial challenge, it’s easy for credit card payments to get missed. This could be from dealing with an emergency expense, the loss of a job, or overwhelming debt. The hard truth is that when credit card payments cannot be met, things can quickly spiral downhill.

When a credit card balance is left unpaid for an extended period, it will continue accumulating interest and fees, putting you in a worse situation than you started with. Interest rates average about 25% per year, which can cause debt to become unmanageable.

This is a daunting reality, but below are outlined ways to save yourself from incurring more debt from high-interest rates and fees.

How do credit cards work?

Let’s begin by understanding how credit cards work. Credit cards allow you to purchase items and pay bills without using your cash. It’s similar to a short-term loan, which a credit card company gives to you in advance. Much like a loan, you are limited on how much money you can be provided in advance.

Transaction Processing with Credit Cards

You will be given a limit when you sign up for a credit card. Each time you purchase something or pay a bill using the card, your available balance will be reduced. When the billing cycle completes, the credit card company will send you a statement with all transactions from the past month. This statement shows you the entire balance that needs to be repaid and the amount you are required to pay during that billing cycle.

Considerations

If you keep a high balance on the card month after month, you may be subject to additional interest. Credit cards are charged an annual percentage rate, or APR, each month which will be calculated based on the average daily balance. There is also a penalty APR; a higher rate charged when you miss two or more monthly payments.

The Difference Between Credit and Debit Cards

Credit cards and debit cards are in two separate lanes. Credit cards are linked to the bank’s account, while a debit card is linked to your checking account. Debit cards have no impact on your credit score as you use your money to make purchases and payments. However, credit cards directly impact your credit score. Every action or inaction made on your card and account will be reported to the Credit Bureau Singapore (CBS) to formulate your score.

Repaying Monthly Bills In Full

Paying your credit card balance monthly to improve your credit score is essential. As we previously discussed, credit cards are not meant to mode for long-term loans due to the APR. If you need a long-term loan, consider other options than using your credit card.

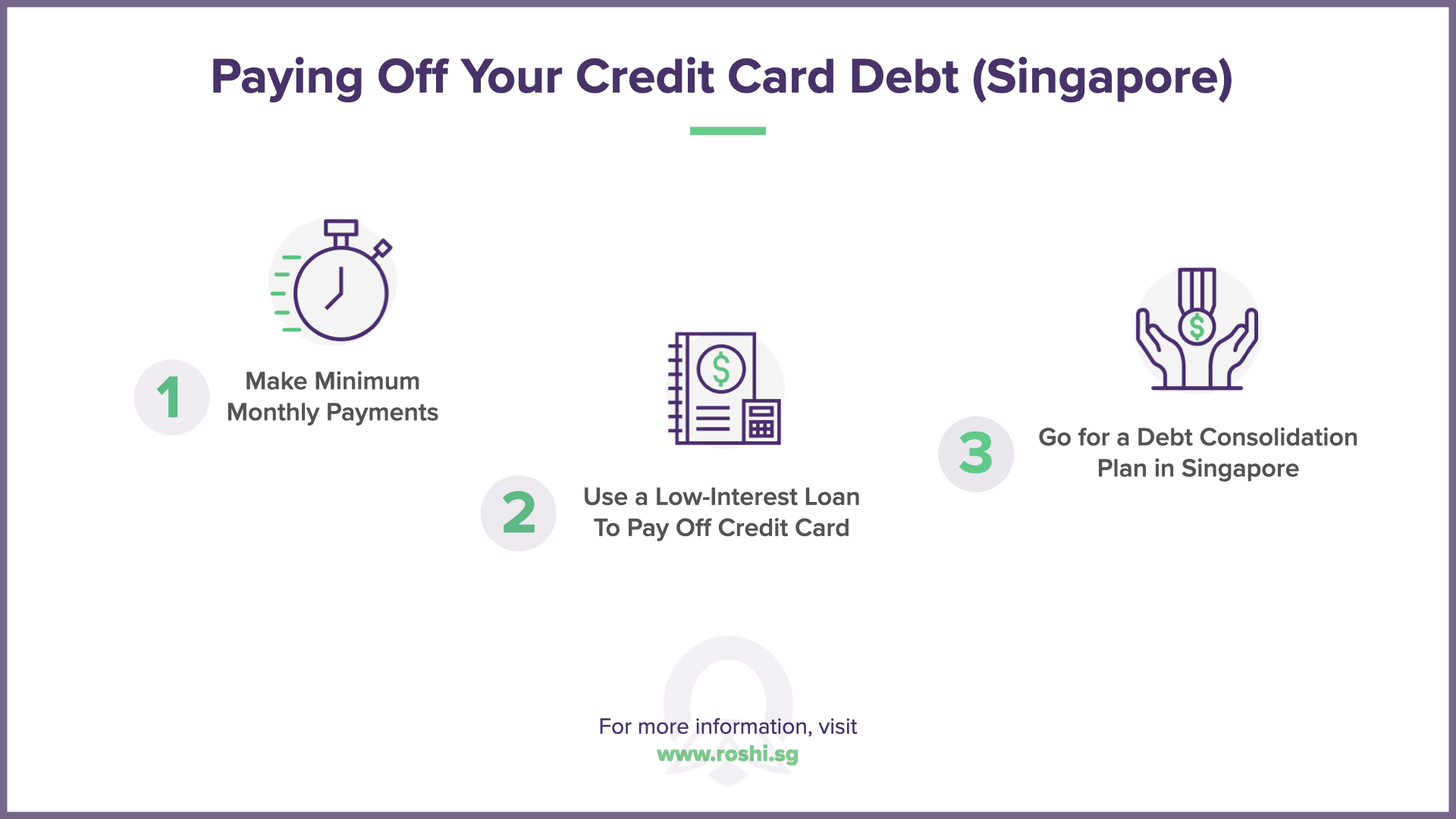

How to Pay Off Your Debt?

You can consider several options if you are struggling to pay off your debt. Look at the list below to determine the best repayment method for you.

Making Minimum Monthly Payments

If paying your monthly bill in full is impossible, you must at least pay the minimum balance due. A minimum balance owed is established by credit card companies and is a percentage of the total balance. If you cannot meet the minimum, you can quickly damage your credit score, affecting your ability to get loans. Not completing the minimum payment can also result in $100/month for late payments.

In Singapore, most credit card companies set the minimum monthly payment to 3% of the total balance or $50, whichever is higher.

Use A Low-Interest Loan To Pay Off Credit Card

One of the best options you can do to pay off a credit card debt is to take out a personal loan with low-interest to settle the debt. Then you can build credit by paying off the loan instead of trying to pay down your credit card. In Singapore, most personal loans carry an interest rate of 7% per year, a drastic decrease from 25% for most credit card companies. Another benefit of choosing a personal loan is extending your payment over a long period to keep your required monthly payments to a minimum. One thing to keep in mind when taking out a loan is early repayment may result in a prepayment fee.

Go for Debt Consolidation Plan in Singapore

If your debt is 12 times or more than your monthly income, getting a debt consolidation plan may be your best option. When debt is extraneous, it is crucial to get it paid off as fast as possible, as debt will continue accumulating in the form of interest. In this case, you could be declared bankrupt, which is a massive red flag on your credit score.

Debt consolidation is a way to wrap your debt into a single loan. Here is an example of how this process works. Let’s say you have a monthly salary of $3,000, and you owe $8,500 on one credit card, $10,000 on another credit card, and $15,000 on a personal loan. For personal loans, most lenders will only approve a loan amount that is six times your monthly income. This may not be enough to clear the debt. In that case, you would need to get on a debt consolidation plan, which allows you to move from three separate monthly payments that acquire interest to one low-interest payment plan.

Considerations

If you are already behind payments, you might want to consolidate your debt via a lower interest personal loan. ROSHI’s loan marketplace (which is one of the leading lending platforms in Singapore) allows borrowers to see loan offers from various financial institutions and moneylenders without directly applying or negatively affecting their credit score.

Today's Personal Loan Rates

| Lender | Annual Interest Rate | Effective Interest Rate | Processing Fee |

|---|---|---|---|

| Trust Bank | 1.08% | 2.43% | $0 |

| CIMB Bank | 1.28% | 2.46% | $0 |

| DBS | 1.48% | 3.22% | $100 |

| POSB | 1.48% | 3.22% | $100 |

| Standard Chartered | 1.60% | 3.07% | $0 |

| Maybank | 1.79% | 3.29% | $200 |

| HSBC | 1.80% | 3.50% | $0 |

| OCBC Bank | 1.98% | 4.19% | 1.0% of approved loan |

| GXS | 2.99% | 5.65% | 1.35% of approved loan |

| Citibank | 3.45% | 6.50% | $0 |

| OCBC Bank | 5.54% | 10.96% | $200 |