Loan Guarantor in Singapore: All Requirements & Responsibilities

Fact-checked

Fact-checked

At a glance

Being a loan guarantor in Singapore means that the person is responsible for fulfilling the loan contract if the borrower defaults on the loan. It is not an easy task, so potential guarantors must know the consequences of becoming a guarantor. Consequences include possible seizure of the guarantor’s assets, poor credit score and bankruptcy. Before deciding to be a guarantor, it’s best to ask many questions and clarify the borrower’s financial status. Hiring a lawyer to understand the terms of the contract is also advisable.

In Singapore, certain high-risk loans such as car, education, and business may require a guarantor instead of collateral. Understanding the responsibilities of being a guarantor is crucial before agreeing to support a friend or family member. As a guarantor, you promise to pay the borrower’s loan if they default. This could lead to significant financial burdens, like covering a substantial portion of a car loan while the car remains with the borrower. So, it’s important to know your obligations if you choose to be a guarantor for someone.

What is a Loan Guarantor in Singapore?

As a guarantor, you’re responsible for the debt and any associated fees, interest charges, and legal costs if the borrower defaults. Lenders may seek repayment from you without first taking action against the borrower. This could happen as soon as a payment is missed, potentially leading to the seizure of your personal assets, a negative impact on your credit report, and even bankruptcy.

Loan Guarantor Requirements & Responsibilities

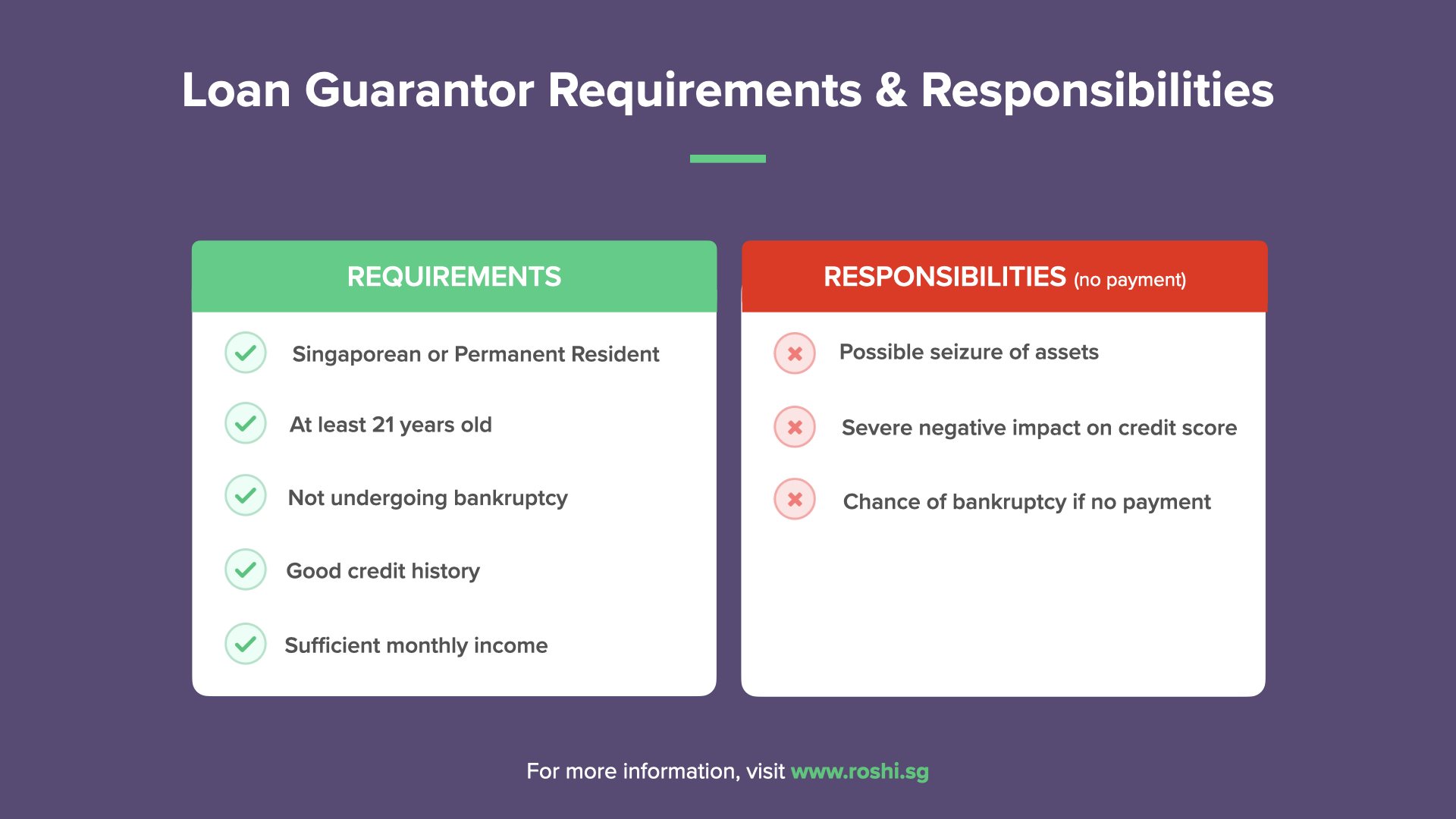

To qualify as a guarantor in Singapore, you must be a Singaporean citizen or Permanent Resident, at least 21 years old, and not undergoing bankruptcy procedures. A good credit history and sufficient income might also be necessary.

Should the lender be unable to pay their loan, the guarantor might face certain consequences. These include:

- Possible seizure of the guarantor’s assets

- A severe impact on the guarantor’s credit reports makes taking up future loans for a car, education, or buying a house more challenging.

- It’s possible to go bankrupt, which might adversely impact the guarantor’s employment opportunities.

Considerations

Before becoming a guarantor, it’s important to consider your ability and willingness to repay the loan, the borrower’s repayment capacity, readiness for potential consequences, and any legal recourse available. Understanding the loan agreement thoroughly is also vital. It’s advisable to consult a lawyer to protect your interests and to thoroughly evaluate your financial situation and the borrower’s ability to repay your debt before agreeing to be a guarantor. If you cannot afford the risk, declining the request is better.

Considerations Before Signing Up

So, you’ve been approached to be a loan guarantor. Here’s what you need to think about before signing the contract.

- Are you able and willing to pay the loan should the lender default on the loan?

- Can the borrower fulfill their loan obligations? Check on their existing loans, credit score and income. It’s best to document these before deciding to be a guarantor rather than depend on goodwill. Even if it is a family member or close friend, it is not wise to be a guarantor to a financially irresponsible borrower.

- Are you able to accept the consequences in the case that you cannot fulfill the loan contract, should the borrower default?

- It may be possible to get repayment from the borrower if the loan contract protects the guarantor. However, the financial institute will still demand money from the guarantor if they cannot receive payment from the borrower.

- Do you understand what’s in the loan contract? Ensure you know the terms and conditions, interest rates and repayment timeline.

Important Information

Most importantly, read carefully and ask questions about the borrower’s ability to repay the loan. Details such as their credit history, financial commitments and income levels will help you decide. You may even want a lawyer to look at the contract so you understand the responsibility of becoming a guarantor.

Also, review your financial commitments before you sign the contract. It is better to be honest and let down a loved one if you cannot bear the responsibility of a defaulted loan.

Overview Of Licensed Moneylenders

| Moneylender | Max. Loan Amount (Singaporeans) | Max. Loan Amount (Foreigners) | Monthly Interest Rate |

|---|---|---|---|

| Best Licensed Moneylender | 6 times monthly income | 6 times monthly income | 1.88% |

| MoneyPlus Capital | 6 times monthly income | 6 times monthly income | 2.89% |

| Advance Cash Credit | 6 times monthly income | 6 times monthly income | 3.00% |

| EZ Loan | 6 times monthly income | 6 times monthly income | 1.99% |

| Abm Creditz Singapore | 6 times monthly income | 6 times monthly income | 3.90% |

| Cash Direct | 6 times monthly income | 6 times monthly income | 3.92% |

| UK Credit | 6 times monthly income | 6 times monthly income | 3.92% |

| Sumo Credit | 6 times monthly income | 6 times monthly income | 3.92% |

| Synergy Credit | 6 times monthly income | 6 times monthly income | 3.92% |

| Raffles Credit | 6 times monthly income | 6 times monthly income | 3.92% |