Should I Get My Home Loan from a Mortgage Broker or a Bank?

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

Everyone knows you can go to the bank to get a home loan. If you approached a bank to inquire about home loans, you would be directed to speak with a mortgage staff who is obliged to promote the loans offered by that particular bank. For example, a DBS mortgage staff will only recommend packages offered by DBS.

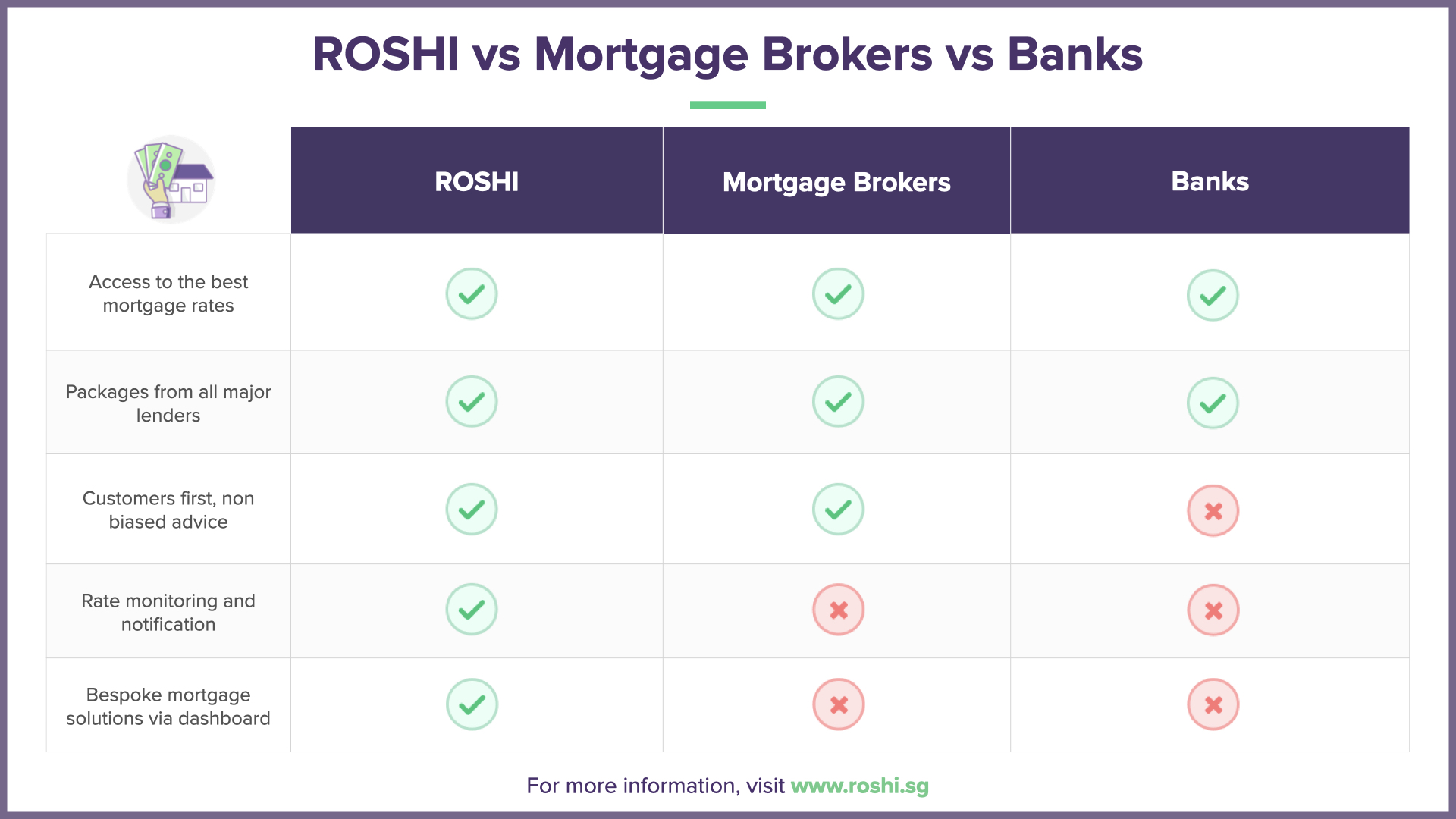

However, perhaps the lesser-known option is going to an independent mortgage broker instead.

Mortgage brokers compare home loan products across different banks and help their clients to get the lowest interest rates. As independent advisors, they do not work for any bank and are relatively free to recommend the best deals to be found anywhere.

This results in a lot more flexibility and a wider range of options, which is a big advantage that going to a mortgage broker has over approaching a bank. Most times, a mortgage broker will be able to help you secure the lowest mortgage rates.

Some Differences Between Looking for a Mortgage Broker and Approaching a Bank

Mortgage brokers and loan managers working for banks operate quite differently. Knowing some of their differences could help you make a more informed decision on which approach to take.

1. Level of experience and knowledge

To build up their customer base, many mortgage brokers have an online presence. This benefits potential clients as well, who can easily validate the broker’s knowledge and track record through customer reviews and social media features. This can provide some assurance of how experienced and reliable that individual broker is.

If you were to approach a bank directly, you would most likely have a random mortgage staff assigned to you. While that staff would have received training of a certain standard from the bank, you will not be able to verify his/her mortgage-related expertise or level of professionalism.

2. Incentive for earning

Since mortgage bankers are employed by a bank, they often earn a basic salary as well as commissions from deals secured. The amount earned through commissions mostly depends on the interest rates being offered and the features of the housing loan package. Hence, mortgage bankers could have an incentive not to help you find the absolute lowest rates or might be reluctant to inform you of the full suite of special features offered for your mortgage because a better choice for you results in lower commissions for them.

Meanwhile, mortgage brokers earn solely from fixed fees, which are dependent on the mortgage loan amount, and not the interest rates or features. This way, they can help you to look for the best deals without conflict of interest.

3. Relationship with clients

Unlike banks, which have a much larger pool of financial resources, independent mortgage firms have a much stronger need to maximise revenue from all the clients they can get. Thus, they are highly incentivised to ensure that all advisory they offer for home loans is trustworthy and insightful.

One way that they do this is by intentionally trying to get to know their clients better. This then opens the doorway for conversations about other financial products, such as insurance or investments, that the broker can also earn from if the client has such needs.

In contrast, loan managers are hired specifically to sell mortgage products for the bank. They could be more interested in simply closing the deal and moving on.

Advantages of Using a Mortgage Broker

1. Cheaper interest rates

Mortgage brokers have a more direct relationship with banks than members of the public. Some mortgage brokers may even have been former mortgage bankers with years of experience in the banking industry. Because of this direct relationship, brokers can usually obtain better home loan interest rates than are made known to the public.

Sometimes, mortgage brokers may even be able to request preferential rates from a particular bank due to the volume of business they may already have generated for the bank.

Mortgage brokers also have a sweeping view of the market and the most updated information on the changing interest rates. As banks often take turns offering the lowest rates to gain market share, mortgage brokers would be in the know of when these rates are offered and can recommend the best options at any point in time.

Since there could be over 50 different home loan packages offered across all the banks in Singapore at any point in time, it would be very time-consuming for you to approach banks one by one to compare their options. Mortgage brokers thus make selecting the right home loan a much quicker and more convenient process.

Considerations

The ROSHI loan marketplace enables borrowers to receive fully personalised mortgage solutions, updates and strategies in real-time directly on our platform, avoiding the hassle of calling, visiting or applying with multiple banks or traditional mortgage brokers.

2. Less biased advice

As mentioned earlier, mortgage brokers do not represent any single bank and can recommend packages across different banks. Mortgage bankers, on the other hand, can only recommend the best packages offered by the bank by which they are employed. Of course, they would try to sell it as the best in the market, but you would have to take this with a pinch of salt and do more research on your own.

3. Faster application process

For any loan (not just home loans), one common pain point is the vast amount of paperwork needed. Having gone through this process with many different clients, mortgage brokers are very familiar with the requirements.

A mortgage broker who is already acquainted with your financial situation could act as a consultant to quickly sieve out the most important details and the forms that are relevant for you to fill out. For example, salaried workers will not need to fill out some forms that self-employed borrowers will.

Brokers can also spot common red flags early and pre-empt you, such as if you fail to meet the total debt servicing ratio requirement of 60%. They could then offer tips on the best workaround procedure.

This speeds up the application process for both you and the bank you’re getting the loan from.

4. Advice on different home loan features and types

Home loans have different features which could be beneficial for you.

For example, a lock-in feature (i.e. a penalty for refinancing your home loan) might sound like a bad idea, but could also mean lower rates, especially if you aren’t planning to refinance for many years anyway.

Considerations

Refinancing your home loan means switching your home loan from one bank to another. Borrowers might opt for this if a better rate is offered elsewhere that wasn’t available at the time when the loan was taken.

However, refinancing comes at a cost – minimally $2,500 for legal fees. It also risks switching to a worse package, which could end up costing more overall.

Some other home loan packages might include free repricing features, meaning that you can switch to another package within the same bank at no additional fee.

Banks offer new types of features all the time. Mortgage brokers can explain which features might work best for your specific needs.

5. Advice on home loan refinancing

A mortgage broker can be useful even if you had taken your home loan many years ago. You might feel that there might be cheaper loans on the market currently.

In these cases, brokers can help to manage the switch to another bank’s loan, which could help to lower your monthly payments. They can help you to work out the costs of refinancing, negotiate for a full offset of your costs and plan for the best time to refinance. They can also help with the required paperwork.

6. Finding a reliable conveyancing law firm

In any property transaction, a law firm will be engaged. The lawyers will review the deeds and documents, such as the Sale & Purchase Agreement and the seller’s background (e.g. if the seller is facing bankruptcy, which could affect the property transaction).

Mortgage brokers would have a network of connections due to their first-hand experience in interacting with law firms. They can thus help you to find a trustworthy conveyancing law firm at a reasonable fee, which can range from $2,500 to over $4,000. Finding a reliable conveyancing law firm is important because any errors on your mortgage documents could result in financially significant delays.

7. Advice on property valuation

Considerations

The Loan to Value (LTV) ratio determines how much a bank can loan you for your house. It is a complex calculation based on many factors, such as age, loan tenure, credit history and number of outstanding property loans.

Things to Watch Out for When Using a Mortgage Broker

Mortgage brokers only earn fees when you take a new home loan from a bank. So in a case where you already have a mortgage and would like to stick to the same bank but change your package (a.k.a. repricing), the broker does not stand to gain from assisting you. There is a chance that the broker might instead advise you to refinance with a different bank, even if this is not the best choice for you.

Instead, if you are looking to bring down the interest rate on your existing mortgage, a better approach would be to first request a repricing offer from your bank before approaching a mortgage broker to consider refinancing.

How Much Does It Cost to Use a Mortgage Broker in Singapore?

Using a mortgage broker is free! Your mortgage broker will be paid by the bank that issues the loan, so you will not incur any cost by engaging the broker.

You may also rest assured with the knowledge that all banks pay fixed commissions to mortgage brokers, so your broker is unlikely to favour any banks.

Some home loan brokers are even able to offer you exclusive rewards, simply because they don’t face the same high operating costs that banks do.

Given the many advantages of engaging a home loan broker, the service being free of charge is the icing atop the cake. We would highly recommend looking for one.

Latest Mortgage Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.

Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

*Today's Mortgage Rates - 21 May 2026

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 0 year | 1.60% |

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| RHB | 0 year | 1.70% |

| OCBC | 2 years | 1.70% |

| Bank of China | 0 year | 1.74% |

| DBS | 0 year | 1.79% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 21 May 2026

Refinancing Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.85% |

*Today's Mortgage Rates - 21 May 2026

Refinancing Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| SBI | 2 years | 1.88% |

*Today's Mortgage Rates - 21 May 2026

Refinancing Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| Standard Chartered | 2 years | 1.65% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 2 years | 1.80% |

| Bank of China | 2 years | 1.84% |

| OCBC | 2 years | 1.84% |

*Today's Mortgage Rates - 21 May 2026

Refinancing Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 2 years | 1.80% |

| OCBC | 2 years | 1.84% |

| Promotion | 2 years | 1.99% |

*Today's Mortgage Rates - 21 May 2026

Latest Mortgage Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.