Over 80% of applicants earned below Singapore’s median income of S$60,840, confirming heavy demand from middle and lower income groups facing inflationary pressures.

58% of applicants already had outstanding unsecured debts when applying, using new loans primarily for consolidation of higher interest credit obligations.

Over 40% sought loans specifically for debt consolidation purposes, but major personal expenses like housing, medical bills, education costs, and business funding needs also materialised as key reasons.

While mostly millennials, ROSHI applicants spanned age demographics - including nearly 15% youth and 20% aged 40+ cohorts. This points to inflation driving personal borrowing needs across employment stages - from digital native new hires to strained ageing households facing retirement cash crunches alike.

58% of applicants were men, with the higher borrowing demand suggesting men exhibit greater financial risk tolerance and remain viewed as household breadwinners in Singapore - pressuring them to secure needed loans during cash crunches. Cultural dynamics likely continue shaping expectations as well.

Over 80% of applicants were full-time employed, validating payroll and income stability key to qualifying for and repaying loans.

But 12% self-employed and marginal shares of students and unemployed point to demand transcending work categories - as those with variable incomes similarly rely on personal loans amid uneven cash flows in an uncertain climate.

Over one-third of applicants were newer employees (<12 months) potentially taking loans amid career transitions and rising costs. But nearly half had above 2-year tenures - confirming personal lending bridging temporary shortfalls even for generally stable households.

So while stretched paychecks of those newer to roles drive some demand, years into gainful employment still no guarantee of comfort during economic fluctuations.

Over 80% earned below Singapore's median salary, confirming heavy skews toward middle and lower income households. With the vast majority under national median, data spotlights personal loans increasingly bridge income-expense gaps and cash flow crunches facing average earners amid runaway living costs.

83% of applicants were Singaporean citizens, confirming the vital role of personal loans providing financial access for locals amid inflation outpacing incomes. Still, over 10% were residents or foreign talent on passes - showing breadth of demand across resident types needing assistance coping with domestic economic volatility.

Half of borrowers lived in public HDB flats, pointing to financial strains with mortgages or housing upkeep amid inflation - especially middle/lower-middle income segments.

Over a quarter resided with parents, reflecting loans meeting youth needs starting independent housing/lives. Though small shares alone, private property owners and renters combined underscore loans' flexibility bridging unstable income variability for some higher earning subsets too.

Over half of applicants already had unsecured debts like credit cards or informal loans when applying - suggesting attempts to consolidate higher interest burdens. But over 40% held no prior unofficial debt, validating the expanded role of personal loans for temporary cash flow smoothing amid inflation.

Over 75% owed at least $5k in prior debts, with 35% above $20k - indicating heavy consolidation demand from significantly pre-burdened households. Though small shares, extremes like 2.5% below $1k and 11% over $50k show loans cater across debt levels - be it light cash flow smoothing or heavy restructuring.

Over 40% sought loans for debt consolidation - namely credit cards, informal debts, and repaying family & friends. But sizable segments also tapped funds for pressing needs like housing, education, and business expenses amid cash flow shortfalls.

Over half requested small $1-5k sums - validating personal loans bridge short-term household budget gaps. Though 18% sought $10-20k for consolidation and over 10% above $20k for investments - conforming loan versatility suiting minor cash flow smoothing to major debt restructuring or asset funding demands alike.

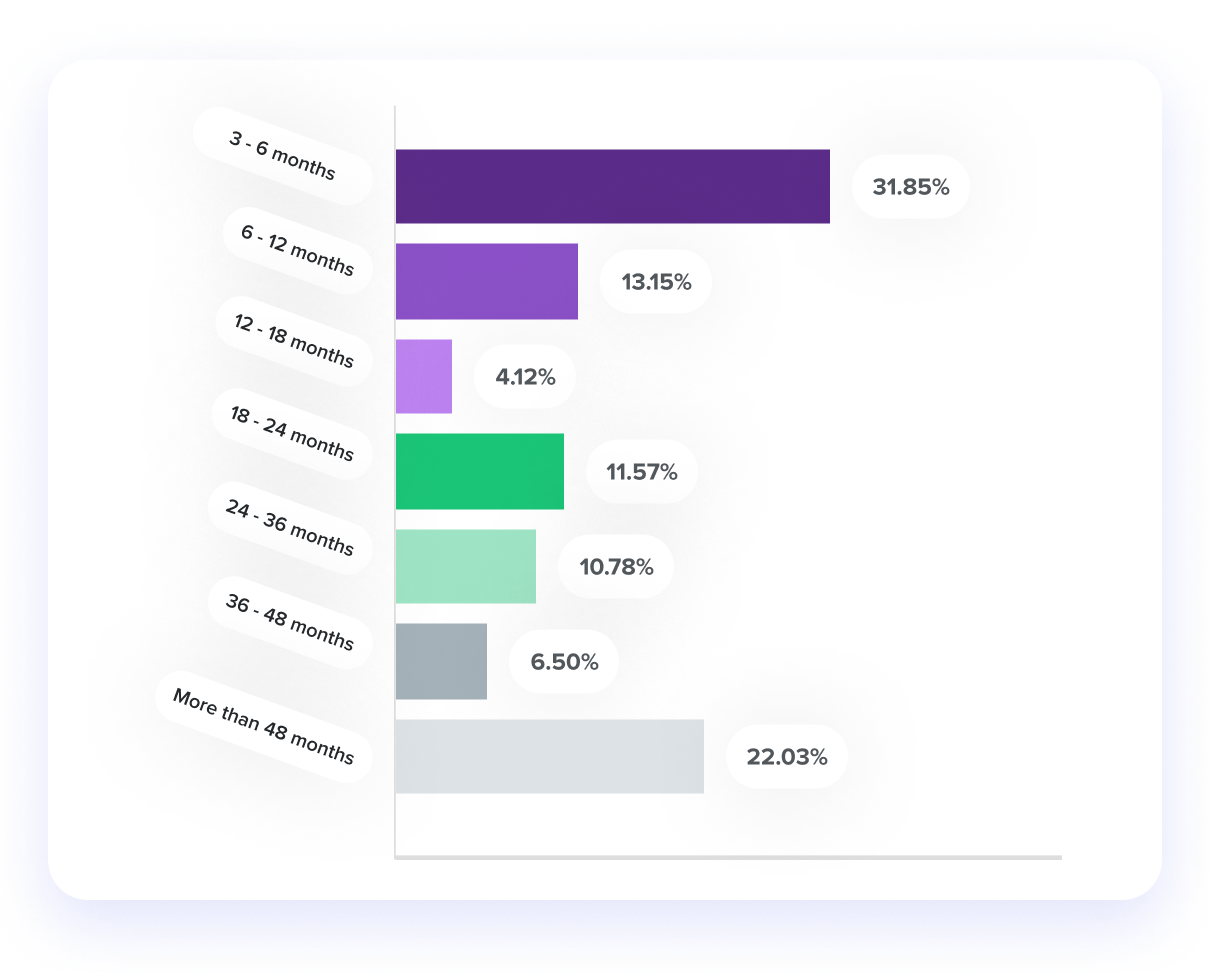

One third sought <6 month terms, confirming small personal loans predominantly fill temporary household budget gaps. Yet 20% requested 4+ year financing for major needs. In between, over 20% carry 1-3 year terms likely restructuring past-due debts into more manageable payment runways when rapidly paid down.

DISCLAIMER

This information herein is published by ROSHI Pte Ltd (UEN 202222480E) (“ROSHI”) and is for information only. This publication is intended for ROSHI and its clients to whom it has been delivered.

This report contains aggregated insights derived from personal loan applications submitted to ROSHI. Importantly, the insights shared are anonymized and contain no personally identifiable information, as protecting personal data is ROSHI’s utmost priority as per Singapore personal data protection laws.

The analysis aims to provide perspectives on borrowing behaviors but may be incomplete or condensed. ROSHI makes no warranty to accuracy or assumes any responsibility for decisions made based on this report. Figures used are for illustration and do not bind ROSHI.

ROSHI performs marketing and matchmaking services to connect clients with lending partners but does not directly offer any lending or financial advisory services under regulation by the Monetary Authority of Singapore. Users of this report should consult professional advisors before engaging in any transaction.

This report is meant solely for insight purposes following Singapore laws and regulations around data privacy. Please contact ROSHI for authorization before reproducing or relying on the analysis.