Buying an HDB Flat (BTO) as Students: What Should Be Considered?

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

If you are one who loves planning in advance, you may be thinking about getting a BTO flat with your partner while you are both still in school.

As BTOs can take up to 7 years to be built, applying early may seem like the ideal choice. If you are wondering if it is wise to apply for a BTO while still in school, here is what you need to look out for.

Can I apply for a BTO while still in school?

Yes, you can definitely apply for a BTO while still in school. The Singapore government has rolled out various concessions to accommodate young couples.

Whether it is a wise decision depends on you and your partner — buying a flat is a big commitment which needs to be discussed. Before applying for one, here are some details you may find useful about purchasing a BTO as a student.

Deferred Income Assessment

As mentioned above, the government provides a concession, the deferred income assessment, for younger couples. This concession is available for those who are:

- Full-time students,

- NS men,

- Those who have recently completed their studies

Couples that are first timers will need to be employed continuously for 12 months to be able to apply for the Central Provident Fund (CPF) grant. As a student, this means you will not get a grant at all, further making it difficult to get a housing loan to help with your flat purchase.

Thus, if you are a student and do not earn any income, the government has given you the opportunity to defer your income assessment till 3 months prior to your flat’s completion.

Important Information

To be eligible to apply for a deferent income assessment, both you and your partner must be at least 21 years old and below 30 years old.

Paying the Downpayment

Once you have successfully balloted and chosen a BTO unit, you will need to sign the lease agreement and pay the down payment within 4 months. For students, this down payment may not come cheap.

With a HDB loan, you will need to pay a 10% down payment of the HDB purchase price. Assuming you have a $300,000 flat, you will need to have a down payment of $30,000.

If you are younger than 30, you are also eligible for the Staggered Downpayment Scheme. This scheme allows you to pay your downpayment in two instalments — once when you sign the agreement for lease, the other during the key collection. This means only paying 5% of you lease upfront and the rest much later.

What If You Breakup?

If you and your partner breakup during the process of getting a BTO, the cost of your breakup will vary depending on which stage of the BTO application process you are at.

Breaking up before booking a flat will mean that there will not be any large financial penalty. However, this would be considered as having rejected a flat. Rejecting a flat more than once will result in your first-timer priority being suspended for a year.

While breaking up later on in the application process may have larger costs. If you have not signed the Agreement for Lease before breaking up, only the option fee would be forfeited. This option fee depends on which unit type you had opted for and can cost up to $2,000.

Breaking up after signing the Agreement of Lease will result in you forfeiting 5% of the purchase price of your flat. This is if you breakup after signing the Agreement of Lease and before key collection. This means that if your flat is purchased at $200,000, you will forfeit $10,000.

In addition, your downpayment, paid stamp duty and legal fees might not be refunded. You can request a reimbursement of stamp duty through getting a lawyer to write to the Inland Revenue Authority of Singapore (IRAS). However, there is no guarantee of reimbursement.

Overall Thoughts

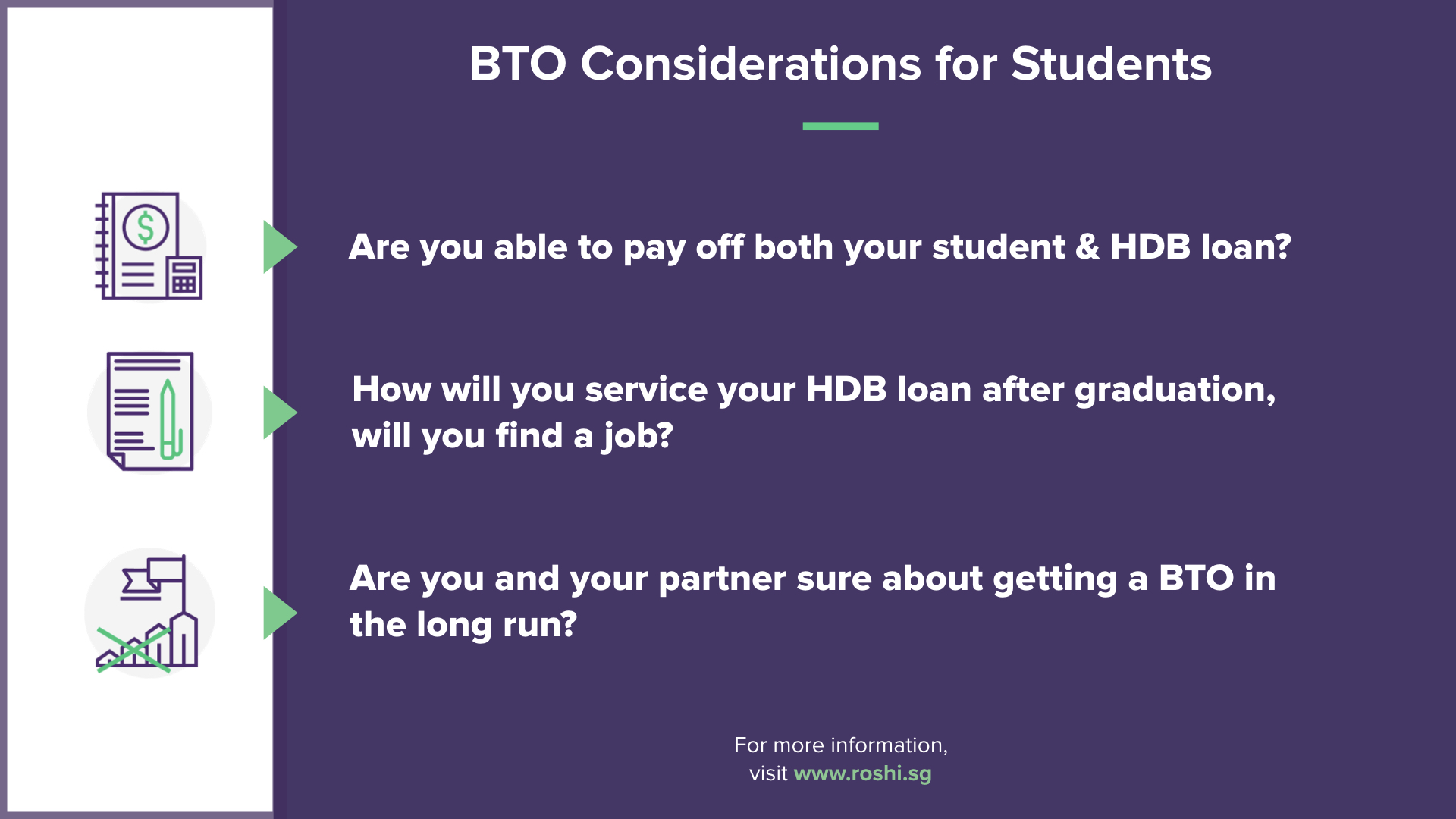

Applying for a BTO is a big step in your life, especially when you are still a student. It is important to consider some of these factors with your partner before deciding to apply for a BTO:

- Are you able to pay off both your student loans and HDB loans?

- How will you service this HDB loan after graduation?

- What if you are not able to find a job?

- Are you and your partner sure about getting a BTO in the long run?

Applying for a BTO is a milestone and may result in costs if you relationship fails, thus applying for a BTO should not be something that is decided lightly.

Today's Refinance Rates

The following tables offer a comprehensive look at today’s refinance landscape, featuring competitive rates from established banks. From fixed-rate refinance home loans to floating options, these figures represent current rates in the market.

Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

*Today's Mortgage Rates - 15 May 2026

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 15 May 2026

Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 0 year | 1.60% |

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| RHB | 0 year | 1.70% |

| OCBC | 2 years | 1.70% |

| Bank of China | 0 year | 1.74% |

| DBS | 0 year | 1.79% |

*Today's Mortgage Rates - 15 May 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 15 May 2026