What Is The HDB Loan Eligibility (HLE) Letter? How Can You Apply For It?

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

Whether you are applying for a new HDB flat or buying one from the resale market, you very likely will need a valid HDB Loan Eligibility (HLE) letter.

Since an HLE letter is a necessity when applying for a flat in many situations, the following is a brief explanation of what it is, when you would need to apply for one, what you need to provide when applying, and how to apply for one

What is an HLE letter?

An HLE letter is basically the same as an in-principle approval for a bank loan, except this is for the HDB. It indicates that you qualify for a concessionary housing loan from the HDB, based on your provided information. The HLE will indicate the maximum loan amount that you can take, the monthly instalments, and repayment period.

Your HLE letter is valid for six months from the date of issue, provided that there is no material change in you or your family’s financial situation. You may apply for a new HLE letter one week before your existing HLE expires, if necessary.

When would you need to apply for an HLE letter?

You will need a valid HLE letter in the following instances:

- booking a new flat from the HDB (after successfully getting a queue number)

- obtaining an Option to Purchase from a resale flat seller

- applying for transfer of ownership of an HDB flat

The HLE letter is only required if you wish to take an HDB concessionary housing loan.

Insider tip

It is not necessary to take the loan once you have obtained the letter. You may obtain an HLE letter in advance if you wanted to just have the option of taking it if necessary.

Having an HLE letter would also help you understand the details of your HDB concessionary housing loan, as the letter includes the maximum loan amount that you can take, along with the projected monthly repayment plan. This can help you plan ahead and avoid overstretching yourself into buying a flat that you might struggle to pay for over the decades to come.

For a preliminary estimation of your home financing and budget before applying for an HLE letter, the HDB has a budget calculator.

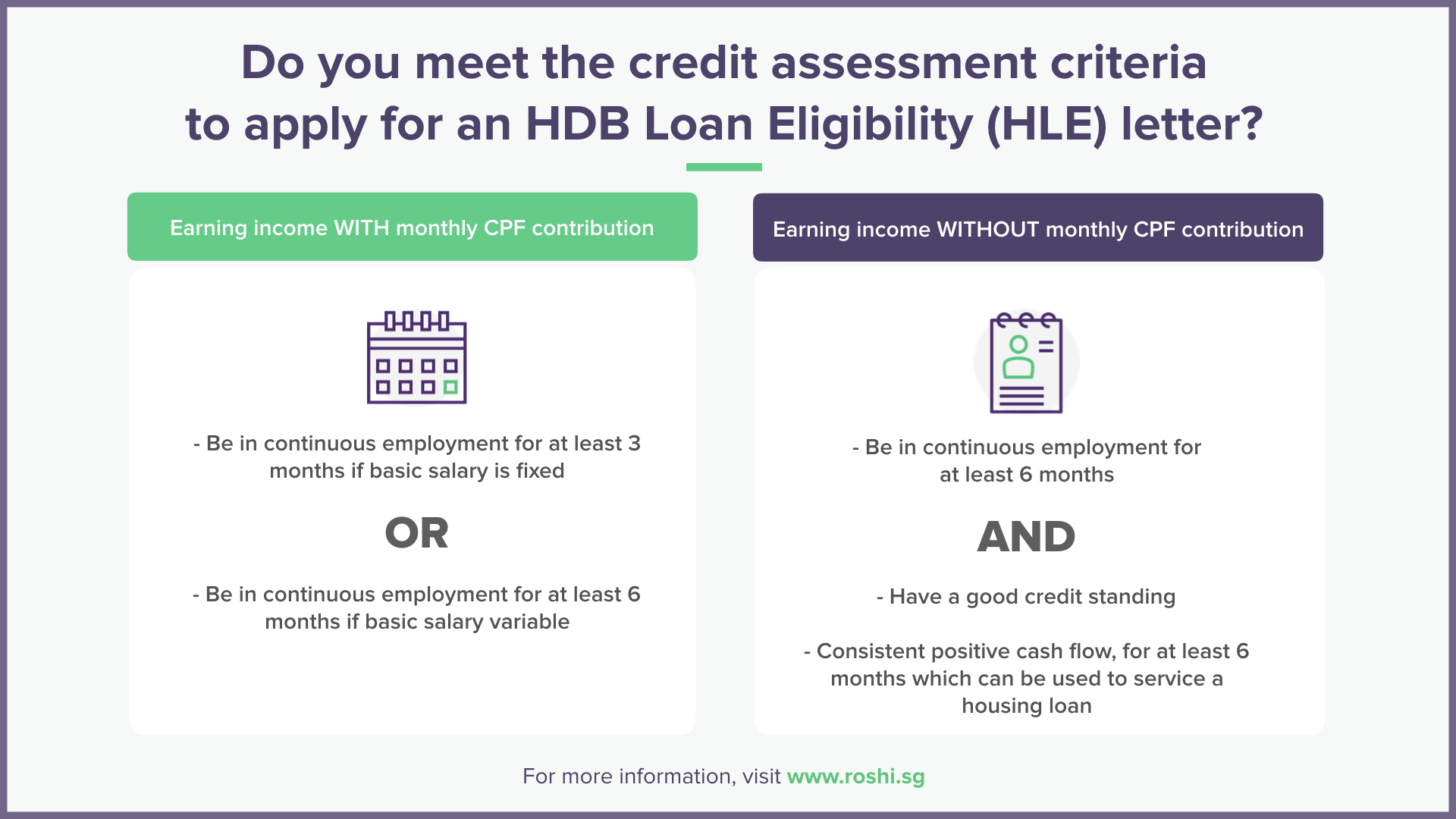

What do you need for an HLE letter?

The size and approval of your HDB loan primarily depends on your ability to sustainably service it. Therefore, your employment status is the key consideration for your application.

For those who are employed with CPF contributions, these are the main documents you need to submit:

-

- Three months of payslips preceding the month of application, or a recent letter from an employer stating job designation, commencement date, and salary for three months preceding the month of application.

- The last 15 months of CPF contribution history. This is downloadable from the CPF website using your SingPass.

If the above is not applicable to you (i.e. you are employed, but do not receive CPF contributions), you may refer to the HDB website for more information.

How do you apply for your HLE letter?

All applications for HLE letters require you to use the HDB’s e-service while logged in with your SingPass. This is also where you should upload any required supporting documents.

Your HLE letter submission will be processed within 14 days once you have submitted a complete application with all required documents. You can check the application status by logging into the HDB website.

If you have any general enquiries about the HLE applications, you can call the HDB Sales/Resale Customer Service at 1800 866 3066 on weekdays, between 8 am to 5 pm.

Latest Mortgage Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 13 June 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 13 June 2026