HDB BTO Application Process: How Do You Buy Your Very First Home in 2023?

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

When Singaporeans become adults, a typical rite of adulthood is the application and purchase of an HDB BTO flat. Without further ado, here are the 6 steps to buying your very first BTO flat in 2021.

These 6 steps include:

- Checking for Eligibility

- Balloting

- Obtaining an HLE Letter or AIP

- Selecting a Flat

- Signing the Lease Agreement

- Collecting the Keys

Need a more detailed understanding of the 6 steps? Let’s break the 6 steps down to simplify matters.

Step 1: Checking for Eligibility

Different requirements for eligibility are a given for the different types of HDB flats. To ensure you qualify for a BTO flat, you will need to check for certain factors.

For HDB BTO flats, both of the applicants can be Singaporean citizens or one Singaporean citizen and one of PR status.

When applying for the BTO flat, you must do so as either a couple or apply as a family unit (including parents, siblings, and children). Widowed or divorced applicants fall under the family unit distinction.

If you are intending to apply as a couple, then you must ensure your marriage is registered before taking possession of the flat. This is so that you can apply for additional or special CPF housing grants within 3 months of taking possession of the flat.

However, if you are applying as a single citizen, then you must be aged 35 and older in order to be eligible for 2-room flats in non-mature estates.

Other eligible applicants for 2-room flats in non-mature estates include citizen and non-citizen spouse couples (with a visit pass or work pass for the non-citizen spouse), or single citizens aged 35 and above that are applying for a flat together with up to 3 other single citizens as co-applicants.

Besides the above criteria, applicants must also not own any other property regardless if it is an HDB or private property, either locally or overseas. If the applicant is a property owner and wishes to apply for an HDB BTO flat, then the applicant will be required to dispose of their ownership status within 30 months of their application.

Considerations

Including the eligibility factors mentioned above, applicants should also ensure that the income ceiling matches with the average household monthly income in order to qualify for the desired flat. This is because having too high of an income will disqualify applicants based on the income ceiling of the specific flat type.

A 2-room flexi flat would typically have a maximum 45 year lease with an income ceiling of $7,000 or $14,000 for short-lease flats.

A 3-room flat on the other hand, would have an income ceiling that depends on the specific flat applicants are balloting for, which will typically range from $7,000, or $14,000. To figure out the exact income ceiling, applicants can check the sales launch of the specific flat.

As for 4-room flats or a larger property, the income ceiling will typically range from $14,000 to $21,000 if applicants are purchasing the flat as an extended or multi-generation family unit.

Step 2: Balloting

The second step to obtaining an HDB BTO flat is balloting. This process involves applicants looking around for a flat they desire, and then balloting for the flat unit online. Applicants will then have to wait until about a month in order to be notified on the success status of the balloting process.

While it sounds like a simple process, balloting for an HDB flat is harder than it seems.

Firstly, applicants will have to check the HDB website regularly in order to get news of upcoming sales and launches. This is because HDB tends to announce upcoming HDB BTO projects 6 months before the launching date, which will give applicants enough time to plan for the desired flat location.

The next part of the balloting process requires applicants to pay $10 to ballot during the BTO application window of the desired flat. The amount of tries before applicants can get a flat in the desired area depends entirely on luck. The amount of tries can range from once or twice, to up to 10 times.

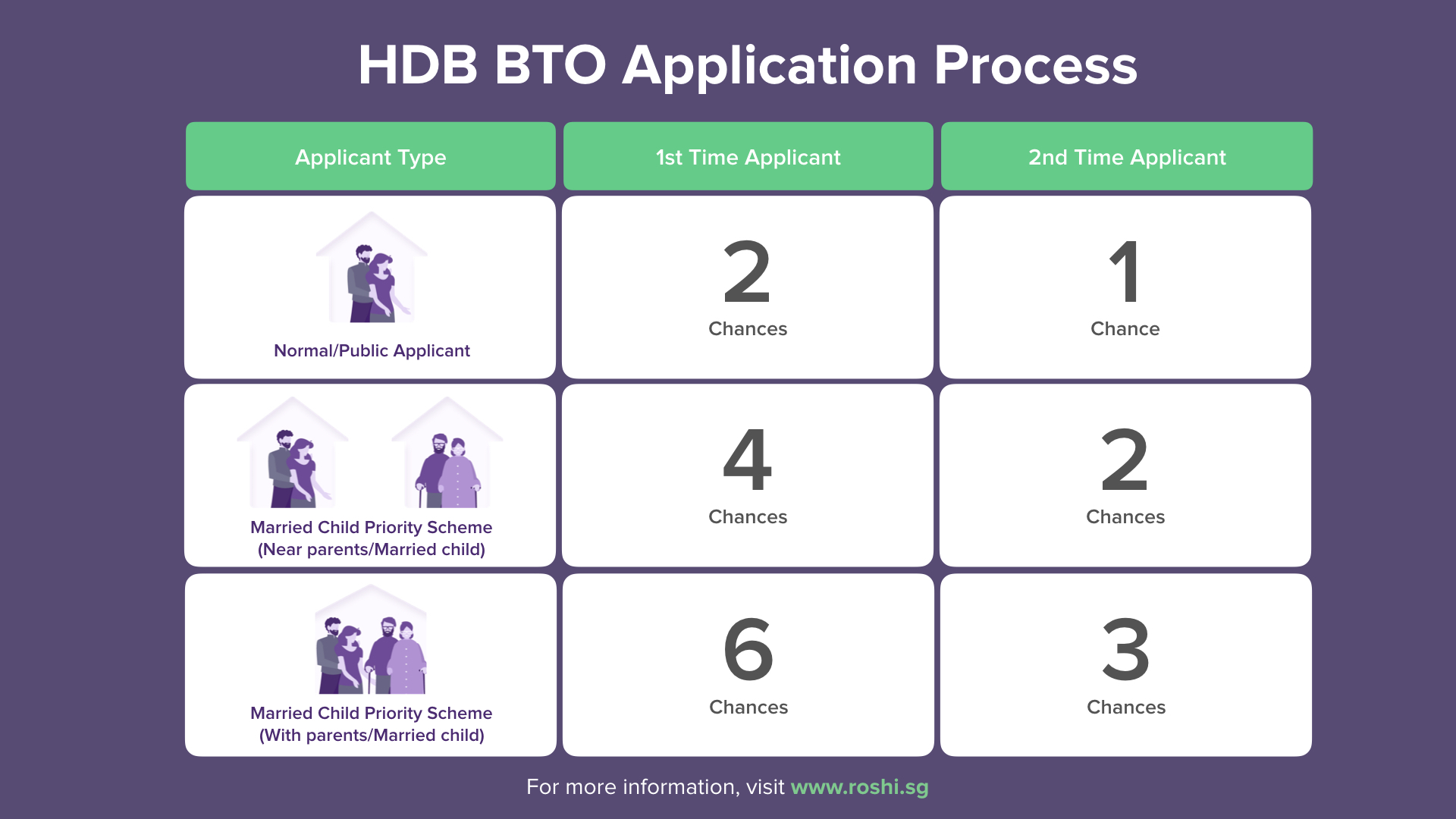

While you can check out the HDB website for more details on the HDB BTO application process, we have added a simplified graph (top of article – next to the heading) detailing of the differences in the application process for first-time and second-time buyers, depending on the eligible applicant types.

Step 3: Obtaining an HLE Letter or AIP

Deciding between taking out an HDB loan or a bank loan is crucial for first-timers, as there is a difference in what you will need to apply for.

The HDB Loan Eligibility (HLE) letter is a must for those that wish to get an HDB loan. For applicants that intend to get a bank loan, the Approval-in-Principle (AIP) can be applied for at the desired bank.

Before fully committing to the HDB BTO flat purchase, it’s a good idea to plan out your finances. This can be done with HDB’s estimated budget calculator on their website.

Typically, first-time HDB flat buyers will choose to get a HDB home loan instead of a bank loan. This is due to the no cash down payment that a HDB loan offers.

However, money savvy applicants with enough savings can choose to get a bank loan and enjoy lower interest rates compared to an HDB loan.

At the end of the day, all applicants must either an HDB Loan Eligibility (HLE) letter or Approval-in-Principle (AIP) before selecting a flat. Plus, all loan documents are required to be in order before a buyer can sign the lease agreement.

Note: If you are looking for the most suitable bank loan for you, you can compare the best home loan rates in Singapore with ROSHI’s New Home Loan page.

Step 4: Selecting a Flat

After your balloting is a success, you will be invited by HDB in order to choose the flat you desire. When you have selected the desired flat, you will then be required to pay the Option-to-Purchase (OTP) fee.

The queue number you have will determine the priority you are given when choosing a flat unit. As the number of people that are allotted queue numbers tend to exceed the number of available flat units, there is a chance that you will have to ballot all over again if you do not get a good queue number.

Important documents such as your IC, income documents, and HLE letter must not be forgotten when heading to the HDB Hub to book the desired flat if you intend to get a housing loan from the HDB. As you will most likely have applied for your CPF housing grants at this point, don’t forget to download and bring along the application forms for the Enhanced CPF Housing Grant to the booking appointment.

The Option-to-Purchase (OTP) fee can be paid on the spot after you’ve selected your desired unit, with variations in the fee for different flat types. 2-room flexi flats have a fee of $500, while 3-room flats have a $1,000 fee, and 4-room or larger flats have a fee of $2,000.

Step 5: Signing the Lease Agreement

After the Option-to-Purchase (OTP) fee is paid, you will be required to pay the down payment, stamp duties, and legal fees on the same day you are to sign the lease agreement.

The lease agreement must be signed within 4 months of booking a flat. As such, do be sure to have your loan arrangements settled by that time period.

Besides that, the down payment amount you will need to pay will depend on whether you chose an HDB loan or bank loan.

Buyers that have chosen an HDB loan will have to pay 10% of the purchase price in cash or with CPF. On the other hand, buyers that chose a bank loan will have to pay 25% down payment, with 5% in cash and the remaining can be paid with CPF savings within certain limits.

For legal fees and stamp duties, a mix of cash and CPF can be used to pay them off. The stamp duty rates for the first $180,000 is at 1%, while the next $180,000 is at 2%. As for the remainder and onwards, the stamp duty rate will be at 3%.

Insider tip

If you are applying for a BTO flat as a first-timer couple in your 20s, then you can apply for the staggered down payment scheme. This allows you to split the down payment into 2 parts; the first payment when signing the lease agreement, and the second payment when signing the Terms of Agreement and collecting the keys.

For example, if your bank loan has a loan ceiling of 75%, the first payment will be 5% in cash plus 5% using CPF OA savings or cash. The second payment will then be 15% using CPF OA savings or cash.

Step 6: Collecting the Keys

Upon completion of the flat, HDB will notify you that the keys to your flat unit can be collected. With the keys collected, you can now move in immediately.

Current Home Loan Rates

The following tables offer a comprehensive look at today’s mortgage landscape, featuring competitive rates from established banks. From fixed-rate mortgages to floating options, these figures represent current rates in the market.

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 08 June 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 08 June 2026