Our Expert says

The Rate You See Is Rarely the Rate You Get

Advertised rates like "from 1.08% p.a." are best case scenarios for top tier applicants with excellent credit scores, high income and existing relationships with the bank.

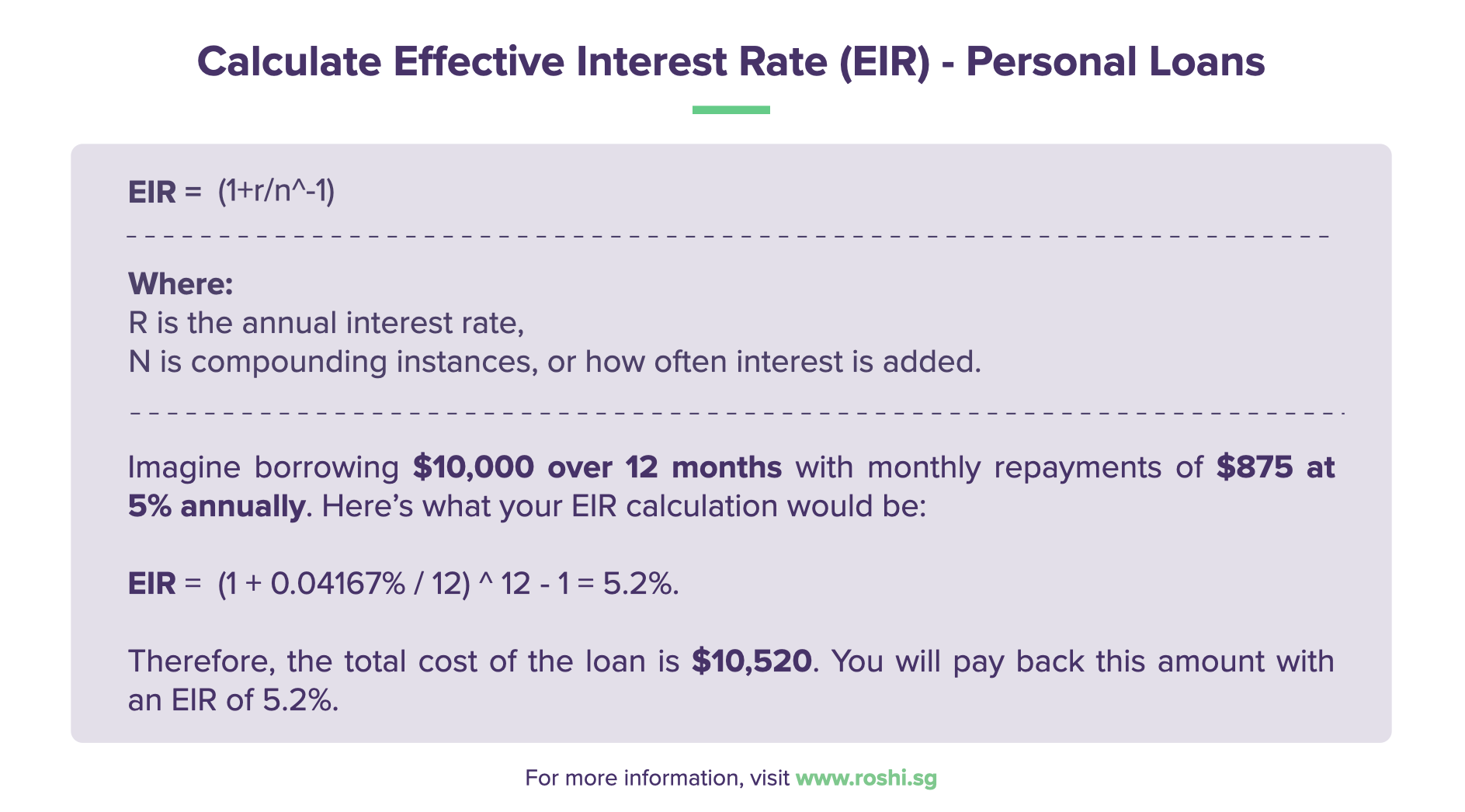

Most borrowers receive rates of 5% to 12% EIR depending on their credit profile. When using this calculator, run scenarios at multiple rates, the advertised rate, a mid-range estimate 7% to 8% EIR) and a conservative estimate 10% to 12% EIR) to understand the realistic range of monthly repayments before applying. ![]()

![]()

How Tenure Affects Total Cost

The same loan can cost vastly different amounts depending on repayment period.

| Loan Amount | 2 Years (EIR 8%) | 3 Years (EIR 8%) | 5 Years (EIR 8%) |

|---|---|---|---|

| $10,000 | $453 per month = $872 interest | $313 per month = $1,268 interest | $203 per month = $2,180 interest |

| $20,000 | $905 per month = $1,720 interest | $626 per month = $2,536 interest | $406 per month = $4,360 interest |

| $30,000 | $1,358 per month = $2,592 interest | $939 per month = $3,804 interest | $608 per month = $6,480 interest |

| $50,000 | $2,263 per month = $4,312 interest | $1,565 per month = $6,340 interest | $1,014 per month = $10,840 interest |

When to Use This Calculator

What This Calculator Helps With

Compare loan amounts

See how borrowing $20,000 vs $30,000 affects monthly payments

Compare tenures

Understand the trade-off between lower monthly payments and total interest cost

Budget planning

Check if the monthly repayment fits within your budget before applying

Rate scenarios

Test different interest rates to prepare for actual loan offers

What This Calculator Does NOT Do

Guarantee approval or actual rates offered

Factor in processing fees or insurance (if any)

Account for early repayment or lump sum payments

Replace official loan quotes from banks