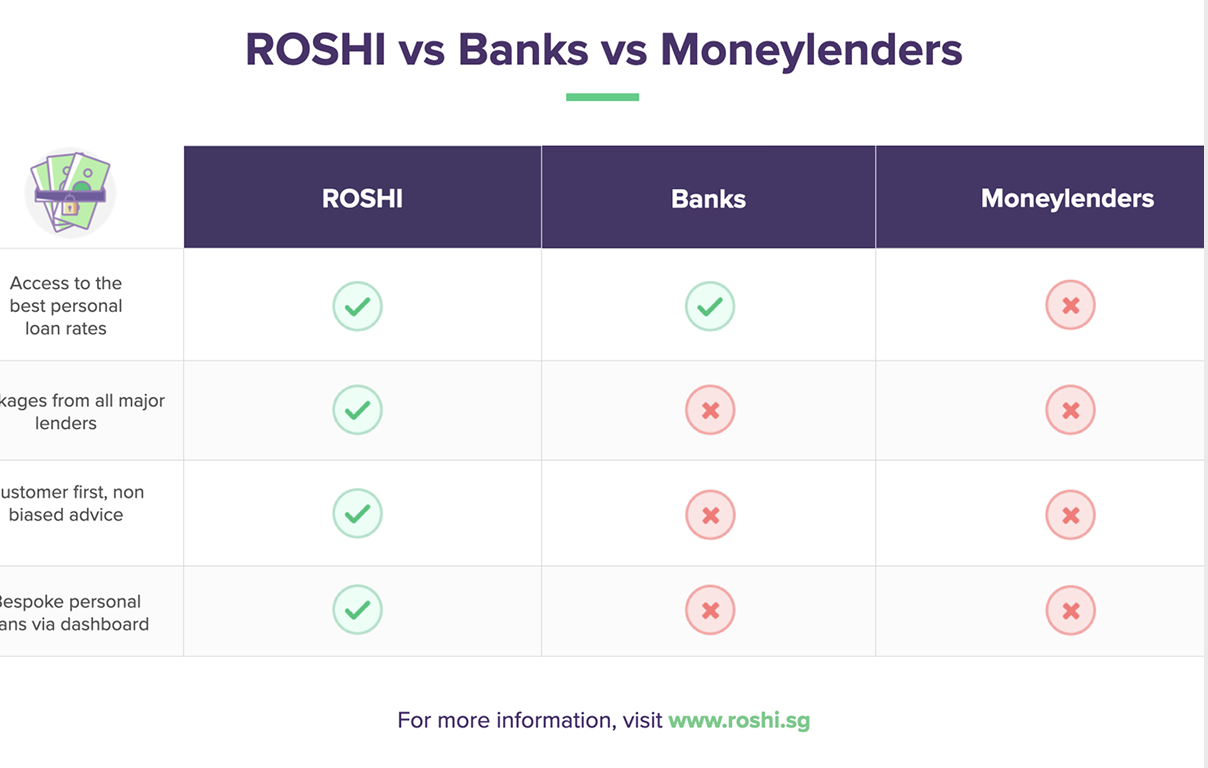

Draw funds up to your limit, repay and reborrow without reapplying. Credit resets as you repay so no need for new applications each time.

A personal line of credit also known as a credit line or revolving credit facility provides flexible access to funds up to a pre approved limit. Unlike personal loans that disburse a lump sum upfront, credit lines allow borrowers to draw funds as needed, repay and reborrow without reapplying. Interest is charged only on the amount used and not the full credit limit which makes crest lines cost efficient for short term or unpredictable financing requirements.

Credit lines in Singapore are offered by most major banks and on this page you’ll find how credit lines work, compare available options and determine whether a credit line or personal loan better suits specific borrowing needs.

A credit line is a pre approved borrowing limit that allows flexible access to funds. Unlike a personal loan where you receive a lump sum and repay in fixed instalments, a credit line lets you withdraw any amount up to your limit, repay it and borrow again similar to how a credit card works. Interest is charged daily on the outstanding balance, not the full credit limit.

Credit line interest rates typically range from 18% to 23% p.a. which is higher than personal loan rates of 5% to 14% EIR but lower than credit card rates of 26% to 28%. Interest is calculated daily on the outstanding balance and compounds if unpaid. Rates are variable and may change based on market conditions.

Draw funds up to your limit, repay and reborrow without reapplying. Credit resets as you repay so no need for new applications each time.

Pay interest only on what you use not your full credit limit. Daily interest calculation means quick repayment minimises costs.

Borrow up to 4 times monthly income (below $120k) or 6 to 10 times (above $120k). Maximum typically capped at $200,000.

No fixed repayment period maintain the facility indefinitely with minimum monthly payments. Repay in full anytime without penalty.

A credit line is a powerful financial tool but only for disciplined borrowers. The flexibility that makes it attractive can also make it dangerous. Because there's no fixed repayment schedule forcing you to clear the debt, it's easy to fall into a pattern of paying only the minimum while the balance grows.

At 20%+ interest, a $10,000 balance with minimum payments can take years to clear and cost thousands in interest. Use a credit line for short term cash flow gaps you can repay quickly not for long-term borrowing. If you need funds for a specific purpose over 12 months, a personal loan at 5% to 12% EIR is almost always cheaper. ![]()

![]()

All lenders verified against Ministry of Law registry. Last updated: July 28 2026.

Three ways to manage debt but each works differently.

| Credit Line | Personal Loan | |

|---|---|---|

| Amount | Revolving limit | Lump sum disbursed upfront |

| How funds are provided | Revolving limit | Lump sum disbursed upfront |

| Interest calculation | Daily on amount used only | On full loan amount from day one |

| Interest rates | 18% to 23% p.a. | 5% to 14% EIR |

| Repayment structure | Flexible minimum payments | Fixed monthly instalments |

| Tenure | No fixed tenure | Fixed 1 to 7 years |

| Reborrowing | Yes, as you repay | No, need new application |

| Early repayment penalty | None | May apply (0-3%) |

| Annual fee | $60 to $150 | None |

| Best for | Short term for unpredictable needs | Specific purpose, longer-term |

| Scenario | Credit Line (20% p.a.) | Personal Loan (8% EIR) |

|---|---|---|

| Borrow $5,000 Repay in 2 months | $165 interest | $65 interest + fees = $150 to 200 total |

| Borrow $20,000 Repay in 3 years | $12,000+ interest (if minimum payments) | $2,500 interest |

| Bank | SC/PR Min Income | Foreigner Min Income |

|---|---|---|

DBS Cashline | $20,000 | $45,000 |

OCBC EasiCredit | $30,000 | $42,000 |

Citibank Ready Credit | $30,000 | $60,000 |

Standard Chartered CashOne | $30,000 | $60,000 |

| Balance | Minimum Payment ($50 + 2.5%) | Time to Clear | Total Interest Paid |

|---|---|---|---|

| $5,000 | $175 per month | 32 months | $2,275 |

| $10,000 | $175 per month | 40 months | $2,000 |

| $20,000 | $175 per month | 48 months | $6,400 |

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

In the past, the thought of borrowing money was associated with stress

![How to Improving Your Credit Score in Singapore? [Updated Information 2026]](https://www.roshi.sg/wp-content/themes/roshi/images/new-home-page/expert/e9.png)

Your credit score plays an essential role in your financial health

This guide offers an in-depth look at securing personal loans in Singapore for those with poor credit.

Unanticipated emergencies can push individuals towards loan sharks

![Can’t Pay Back Your Credit Card Debt? Definitive Singapore Guide [Updated 2026]](https://www.roshi.sg/wp-content/themes/roshi/images/insights/paying-off-your-credit-card-debt-guide.png)

In a time of financial challenge, it’s easy for credit card payments to get missed

Need cash urgently? Consider a personal loan from a bank to relieve your situation.

A credit line provides flexible revolving access to funds but depending on your situation other loan types may be more cost effective. For specific purposes requiring 6+ months to repay, personal loans offer significantly lower interest rates of somewhere between 5% to 14% EIR versus 18% to 23% for credit lines with structured monthly repayments. Those managing multiple high-interest debts may benefit from a debt consolidation plan which combines debts into one lower interest repayment.

Borrowers needing quick access to smaller amounts can also explore fast cash loans or emergency loans from licensed moneylenders for urgent situations.

To estimate monthly repayments and compare options before applying our personal loan calculator helps model different loan amounts, interest rates and tenures. Our credit card repayment calculator helps plan a payoff strategy for existing card balances.

Mastering your loan moves starts with understanding the real cost of borrowing. We believe in empowering you with the right knowledge to make smart financial choices, not quick fixes that lead to debt traps. Our commitment is helping you borrow wisely and stay in control of your money.

Read Our Borrowing Guide

.Don't be a fool! #roshi #singapore #lending #borrowing

Trust the original! #roshi #singapore #lending #borrowing

.Don't be a fool! #roshi #singapore #lending #borrowing

Trust the original! #roshi #singapore #lending #borrowing

.Don't be a fool! #roshi #singapore #lending #borrowing