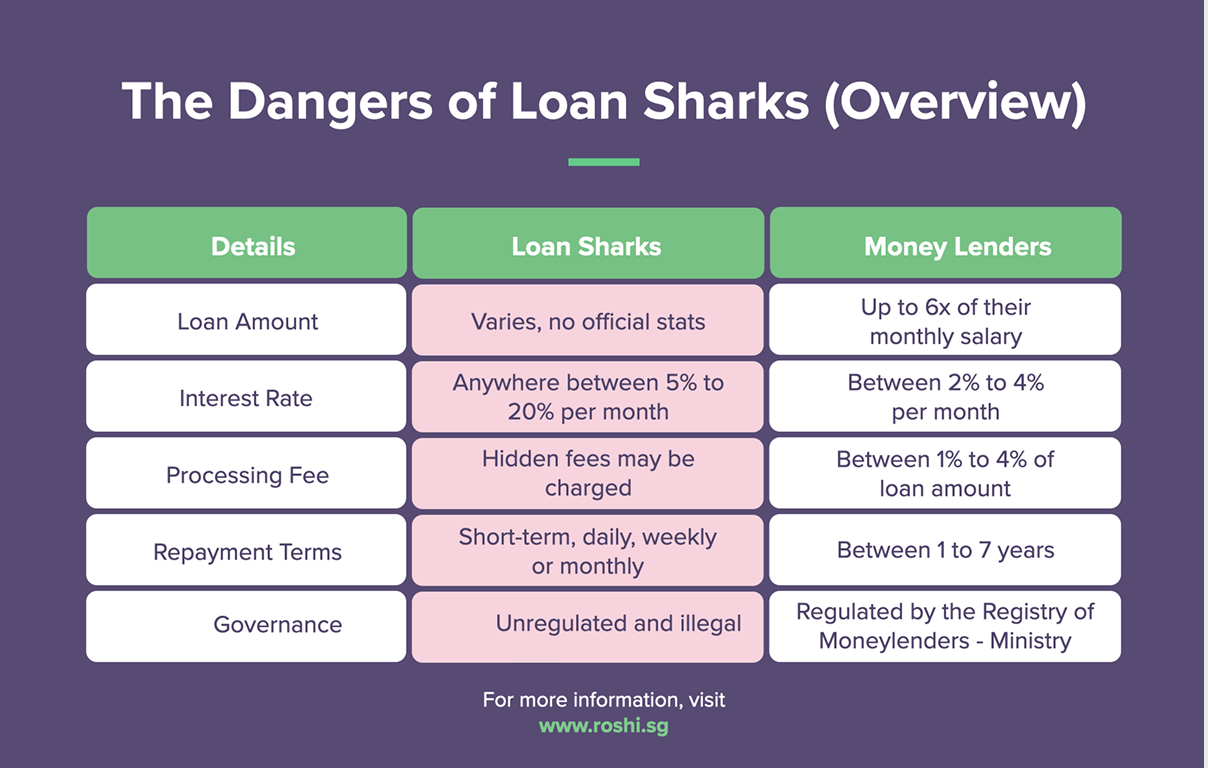

When Should You Get an Emergency Loan?

An emergency loan can be a lifeline when you're facing an unexpected crisis but it's important to pause and assess your situation first.

Ask yourself if this is a one-time emergency or a sign of a bigger problem? If it's the latter, consider speaking with a credit counsellor.

For real emergencies where you need money within hours, licensed moneylenders offer a faster alternative to banks. Just make sure you borrow only what you need and have a clear plan to repay. ![]()

![]()

Borrowing Checklist

Answer these questions before applying:

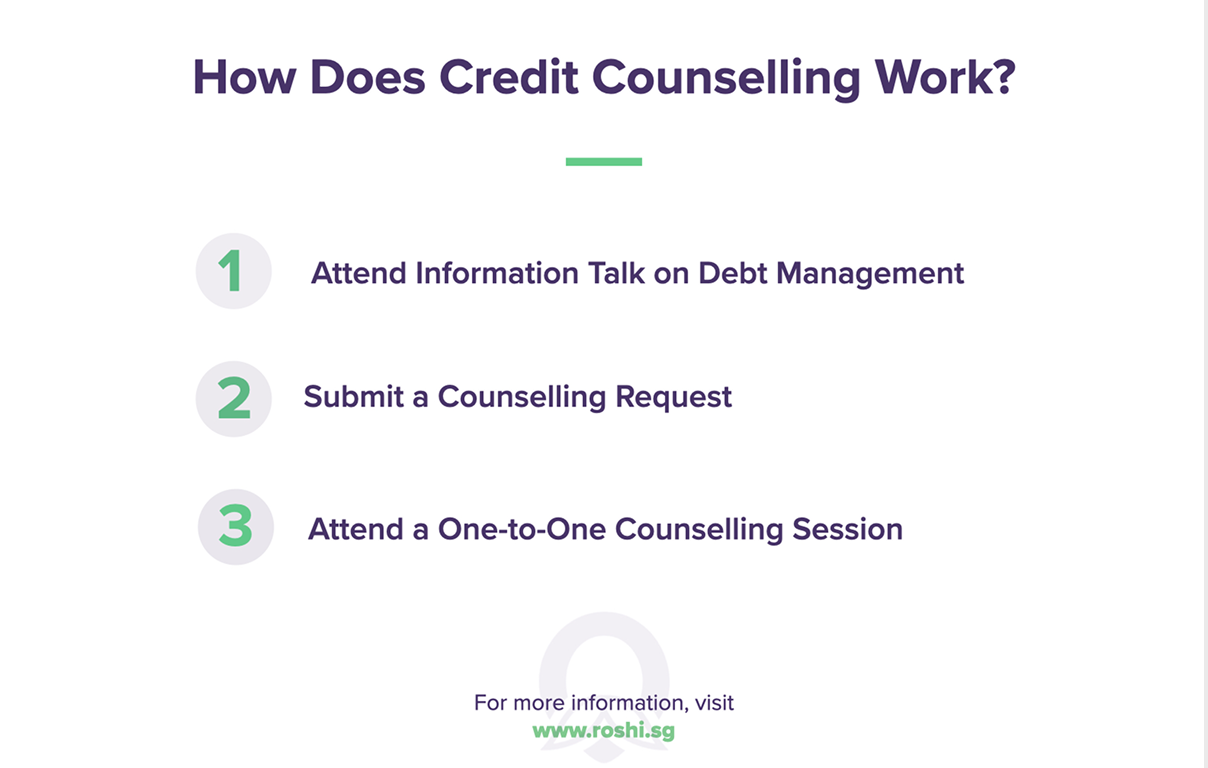

Where to Get Help

Before taking a loan, consider seeking help:

Interest Rate Trends

Research updated by Trinh Thanh on 6 July 2026 - Entering July 2026, Singapore’s consumer lending market continues to remain stable with no major changes to statutory interest rate caps, administrative fee limits or licensed moneylending regulations. Licensed moneylenders continue operating within the same regulated framework helping maintain consistent conditions for short term borrowing needs.

Demand for emergency loans remains relatively steady, especially among borrowers managing urgent situations such as unexpected medical expenses, household repairs or temporary income disruptions. Loan amounts around S$2,000 continue to be commonly requested as they are usually large enough to address immediate financial needs while still being manageable for short term repayment. Compared to June, rate trends and approval conditions have remained largely unchanged across the regulated lending environment.

As of July 2026, licensed moneylenders regulated by Singapore’s Registry of Moneylenders continue to provide emergency financing at average monthly interest rates of around 3.8%, remaining slightly below the legal cap of 4% per month. These rates are commonly applied to emergency loan amounts such as S$2,000 depending on the borrower’s income level, MLCB records, repayment capacity and current financial commitments.

Although borrowers may qualify for higher loan limits of up to six times their monthly income, emergency loans are generally structured around more moderate amounts intended to address immediate financial situations. Administrative fees continue to remain capped at 10% of the principal loan amount while late payment charges generally stay within the S$60 monthly regulatory limit.

Most emergency loan applications can still be started online allowing borrowers to submit basic details and supporting documents digitally before visiting the lender’s office.

However, Singapore regulations continue to require borrowers to complete identity verification and sign loan agreements in person before funds can be released. Once documents have been reviewed and verification has been completed many licensed moneylenders are still able to finalise approvals and disburse funds within the same working day.

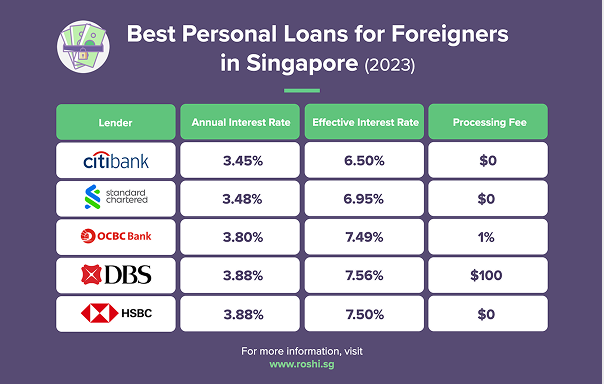

Banks in Singapore continue to offer unsecured personal loans and credit facilities that may be used for emergency funding, although these products are not usually designed for urgent short term borrowing. Compared to licensed moneylenders, banks generally continue to provide lower effective interest rates particularly for borrowers with a stronger credit score, stable income and longer repayment periods.

For emergency loan amounts such as S$2,000, banks may still provide a lower overall borrowing cost for individuals who are not facing immediate time pressure. However, approval procedures remain more detailed and structured. CBS statements, income verification and supporting documentation continue to form part of the application process with approval timelines often extending across several business days depending on the level of verification required.

Because approvals may still take longer, bank financing may not always match the urgency associated with emergency expenses. As a result, licensed moneylenders continue to remain the more practical option for borrowers who require faster access to funds within a regulated lending environment.

In July 2026, emergency loans continue to reflect the balance between fast access to funds and responsible repayment planning within Singapore’s consumer lending market. Licensed moneylenders remain able to disburse loan amounts such as S$2,000 within relatively short timeframes once verification requirements are completed. Monthly interest rates have also remained stable at around 3.8%, consistent with Singapore’s regulated lending structure.

From ROSHI’s perspective, emergency loans continue to work best when they are used for genuine short term financial situations with a clear repayment plan in place. These loans are generally intended to help borrowers manage unexpected expenses rather than ongoing financial difficulties or long term borrowing needs.

Through ROSHI’s platform, borrowers are also able to compare licensed lenders more easily, review loan terms clearly and make decisions based on urgency, affordability and repayment readiness.

For borrowers in July 2026, Singapore’s consumer lending market continues to provide regulated options for emergency financing. Licensed moneylenders still provide quick access to loan amounts such as S$2,000 supported by clear regulations on monthly interest rates, administrative fees and late payment charges. Although in-person verification remains mandatory, approvals are generally still completed within a short timeframe when all required documents are available.

Bank alternatives continue to offer lower long term borrowing costs but they remain more suitable for borrowers who are able to wait longer for approval and disbursement. For situations where timing is more urgent, licensed moneylenders continue to provide a faster and more accessible option.

Within Singapore’s regulated consumer lending environment, borrowers who compare loan terms carefully and align emergency loan amounts with realistic repayment capacity continue to be better positioned to manage urgent financial needs without creating unnecessary financial pressure.