All banks on this page are licensed by the Monetary Authority of Singapore (MAS). Your property and data are protected under strict regulatory guidelines.

A home loan is likely the largest financial commitment most people will ever make and getting it right can save home buyers tens of thousands of dollars over the life of a mortgage.

This page covers everything there is to know about home loans in Singapore. How to choose between an HDB concessionary loan and a bank loan, understanding the critical TDSR & MSR limits that determine borrowing capacity, LTV rules for different property types and whether a fixed or floating rate makes more sense. It also explains SORA, the benchmark for floating rates, breaks down the true cost of buying a property and shares expert tips to improve approval chances. Whether you are a first time buyer or a property investor this page provides the information needed to make an informed decision before comparing rates.

A home loan or mortgage is a secured loan from a bank used to buy property. The property itself serves as collateral allowing banks to offer much lower interest rates than unsecured loans. In Singapore, home loans typically have tenures of 15 to 30 years with interest rates ranging from 1.50% to 3.50% p.a. depending on whether you choose a fixed or floating rate and the current SORA benchmark.

All banks on this page are licensed by the Monetary Authority of Singapore (MAS). Your property and data are protected under strict regulatory guidelines.

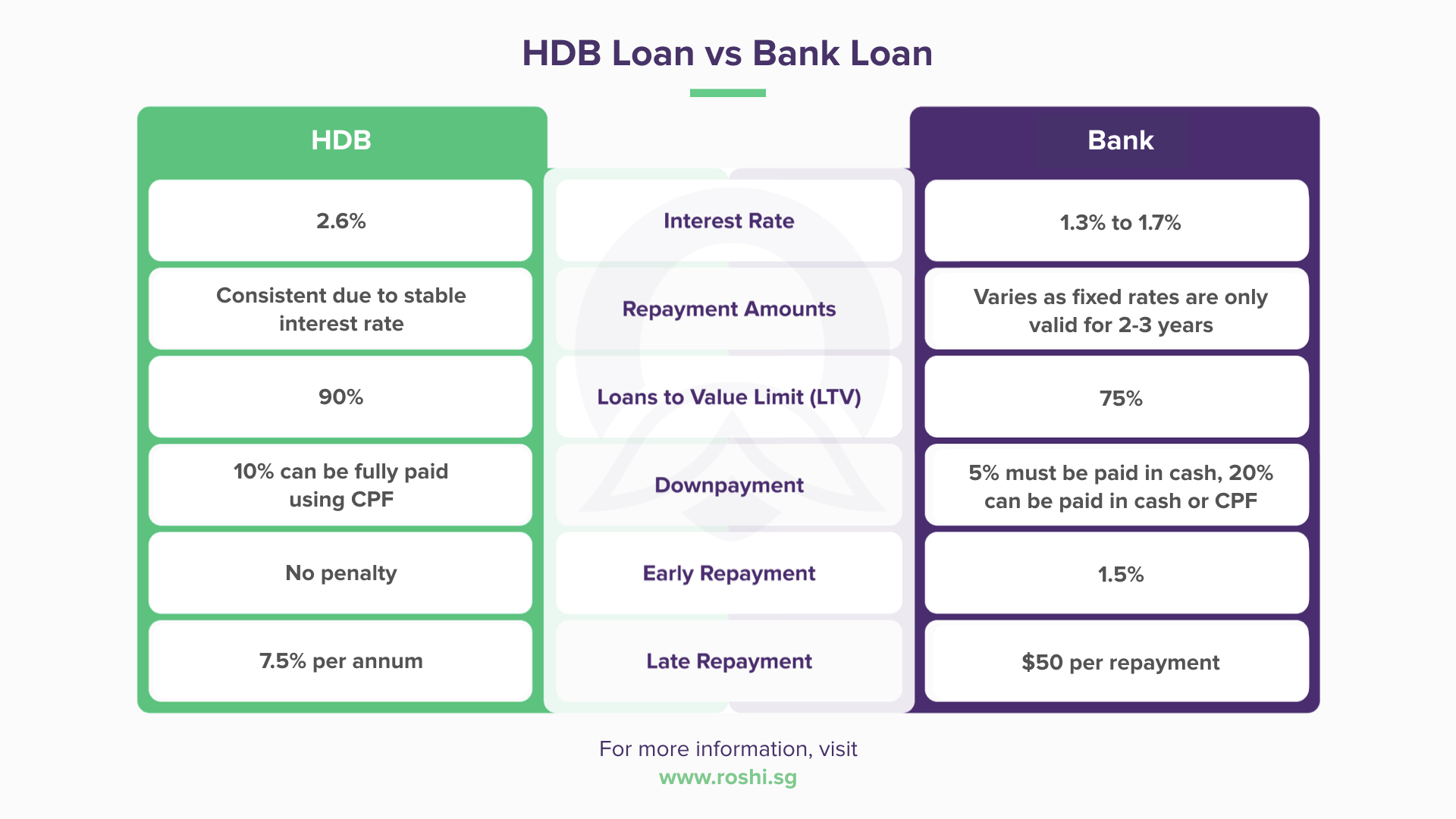

Bank loan rates range from 1.33% to 1.68% p.a. HDB concessionary loan remains fixed at 2.6% p.a. (pegged to CPF OA rate + 0.1%).

Compare home loans from DBS, OCBC, Standard Chartered, HSBC, Maybank, Citibank, Bank of China and more.

Borrow up to 75% of property value with a bank loan or 80% with an HDB loan. Your down payment can be paid using CPF and/or cash

With bank rates now significantly lower than HDB's 2.6% we're seeing a 7x increase in HDB to bank loan switches. Here's my advice for different buyer profiles:

For first-time HDB buyers: Start with an HDB loan if you want flexibility. You can refinance to a bank later without penalty but if you're confident in your finances, a bank loan at 1.55% to 1.75% saves you $200 per month on a $400k loan.

For private property buyers: Bank loan is your only option. Consider a 2-year fixed rate at 1.55% to 1.65% if you want certainty. After lock-in, refinance or reprice to the best rate available.

For those refinancing: Start comparing 3 months before your lock-in ends. With rates at historic lows you could save thousands by switching. Most banks offer $2,000 to $2,800 in legal subsidies so switching costs you almost nothing.

One thing I always tell clients: Don't just look at Year 1 rates. Check the spread after lock-in (e.g., SORA+1.00% vs SORA+0.60%) that's when you'll need to refinance and a

lower spread gives you a buffer . ![]()

![]()

| HDB Concessionary Loan | Bank Loan | |

|---|---|---|

| Interest Rate | 2.6% p.a. (fixed, pegged to CPF OA + 0.1%) | From 1.50% p.a. (fixed) or SORA+0.25% (floating) |

| Rate Stability | Unchanged for 20+ years | Fixed rates are stable for 2 to 5 years. floating rates move with SORA monthly |

| Loan-to-Value (LTV) | Up to 80% | Up to 75% |

| Down Payment | 20% (can be 100% CPF, no cash required) | 25% (5% must be cash, 20% can be CPF) |

| Lock-In Period | None | 2 to 5 years |

| Early Repayment Penalty | None | 1.5% of amount redeemed (during lock-in) |

| Partial Prepayment | Allowed anytime, no penalty | Limited during lock-in (30% to 50% max for some packages) |

| Eligibility | Singapore Citizens only, must form family nucleus, income ceiling $14,000/month for new flats | Citizens, PRs, some foreigners; no income ceiling |

| Credit Check | Basic eligibility check by HDB | Full credit assessment by bank (CBS score matters) |

| MSR Applies? | Yes, ≤30% of gross income | Yes, ≤30% of gross income |

| TDSR Applies? | No (HDB loans are exempt from TDSR) | Yes, ≤55% of gross income |

| Refinancing | Can refinance to bank anytime | Can refinance to another bank after lock-in |

| Can Switch Back? | N/A | Cannot switch from bank loan to HDB loan |

| Maximum Tenure | 25 years or until age 65 | 30 years (HDB flat) or 35 years (private) |

| Legal Fees | Included in HDB process | $1,800 to $2,500 (often subsidised by bank) |

| Interest Rate | Monthly Repayment | Total Interest | Total Repayment | |

|---|---|---|---|---|

| HDB Loan | 2.6% p.a. | $2,275 | $182,500 | $682,500 |

| Bank Loan (Fixed) | 1.75% p.a. | $2,054 | $116,200 | $616,200 |

| Bank Loan (Floating) | 1.50% p.a. | $1,999 | $99,700 | $599,700 |

In 2026 and with SORA at around 1.1% to 1.2%, bank loans are significantly cheaper than HDB loans. A 1% rate difference on a $500,000 loan saves you about $220/month or $2,640/year, that's nearly $70,000 over 25 years.

However, rates can change and If you choose a floating rate, your payments could increase if SORA rises. My advice, if you're buying now and want certainty consider a 2-3 year fixed rate package to lock in low rates. You can always refinance when the lock-in ends.

One more thing once you switch from HDB loan to bank loan, you cannot switch back. So you

might

want to start with an HDB loan to keep your options open.![]()

![]()

Factor | Fixed Rate | Floating Rate (SORA) |

|---|---|---|

| Current rates | 1.50% to 1.80% p.a. | SORA + 0.25% to 0.50% |

| Rate stability | Locked for 2 to 5 years | Changes monthly with SORA |

| Best when | Rates expected to rise | Rates expected to stay low or fall |

| Risk level | Low | Higher |

| Monthly payment | Fixed during promo period | Variable |

| Lock-in period | Usually matches fixed period | 2 years typical |

| Who it suits | Risk averse and first-time buyers | Rate watchers and investors |

| Debt Type | Monthly Payment |

|---|---|

| New home loan (applying) | $3,000 |

| Car loan | $800 |

| Personal loan | $300 |

| Credit card (3.5% of $5,000 balance) | $175 |

| Total Monthly Debt | $4,275 |

| MSR | TDSR | |

|---|---|---|

| What it covers | Home loan payment only | All monthly debt payments |

| Limit | ≤30% of gross income | ≤55% of gross income |

| Applies to | HDB flats, ECs from developer | All property loans |

| Stress test rate | 4% p.a. minimum | 4% p.a. minimum |

Gross Monthly Income | Max Monthly Payment (MSR 30%) | Approx. Max Loan (25 yrs) |

|---|---|---|

| $5,000 | $1,500 | ~$285,000 |

| $6,000 | $1,800 | ~$340,000 |

| $8,000 | $2,400 | ~$455,000 |

| $10,000 | $3,000 | ~$570,000 |

| $12,000 | $3,600 | ~$680,000 |

| $15,000 | $4,500 | ~$855,000 |

| $15,000 | $4,500 | ~$855,000 |

Borrower Age + Loan Tenure | LTV Limit (1st Loan) |

|---|---|

| ≤65 years | 75% (bank) / 80% (HDB) |

| >65 years but ≤75 years | 55% |

| >75 years | Case-by-case |

1-Month Compounded SORA | 3-Month Compounded SORA | |

|---|---|---|

| Adjustment frequency | Monthly | Quarterly |

| Responsiveness | More responsive to rate changes | Smoother, less volatile |

| Best for | Those who want quick benefit from rate drops | Those who prefer stability |

With bank rates now significantly lower than HDB's 2.6% we're seeing a 7x increase in HDB to bank loan switches. Here's my advice for different buyer profiles:

For first-time HDB buyers: Start with an HDB loan if you want flexibility. You can refinance to a bank later without penalty but if you're confident in your finances, a bank loan at 1.55% to 1.75% saves you $200 per month on a $400k loan.

For private property buyers: Bank loan is your only option. Consider a 2-year fixed rate at 1.55% to 1.65% if you want certainty. After lock-in, refinance or reprice to the best rate available.

For those refinancing: Start comparing 3 months before your lock-in ends. With rates at historic lows you could save thousands by switching. Most banks offer $2,000 to $2,800 in legal subsidies so switching costs you almost nothing.

One thing I always tell clients: Don't just look at Year 1 rates. Check the spread after lock-in (e.g., SORA+1.00% vs SORA+0.60%) that's when you'll need to refinance and a

lower spread gives you a buffer . ![]()

![]()

| Property Value | BSD Rate |

|---|---|

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 | 3% |

| Next $500,000 | 4% |

| Next $1,500,000 | 5% |

| Above $3,000,000 | 6% |

| Buyer Profile | 1st Property | 2nd Property | 3rd+ Property |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Permanent Resident | 5% | 30% | 35% |

| Foreigner | 60% | 60% | 60% |

Good intermediary for understanding market trends and knowing many offerings laid out for clarity. Professional and timely sync + scheduling to ensure apt offers and appointments are arranged. Recommended

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I used Roshi , to be referred to a trusted lender and got my loan approved.. Would highly recommend anyone to use Roshi for their financial need s. 2 thumbs up.

I am truly grateful to Rosh for helping me find such a professional and reliable lending company. They don’t just provide financial support, but also take the time to understand and guide you with genuine care. Rosh’s assistance made the entire process smooth and reassuring, and I sincerely appreciate the professionalism and dedication.

After you’ve cleared the hurdle that is the down payment for your new home, don’t forget there are still the monthly mortgage instalments to go.

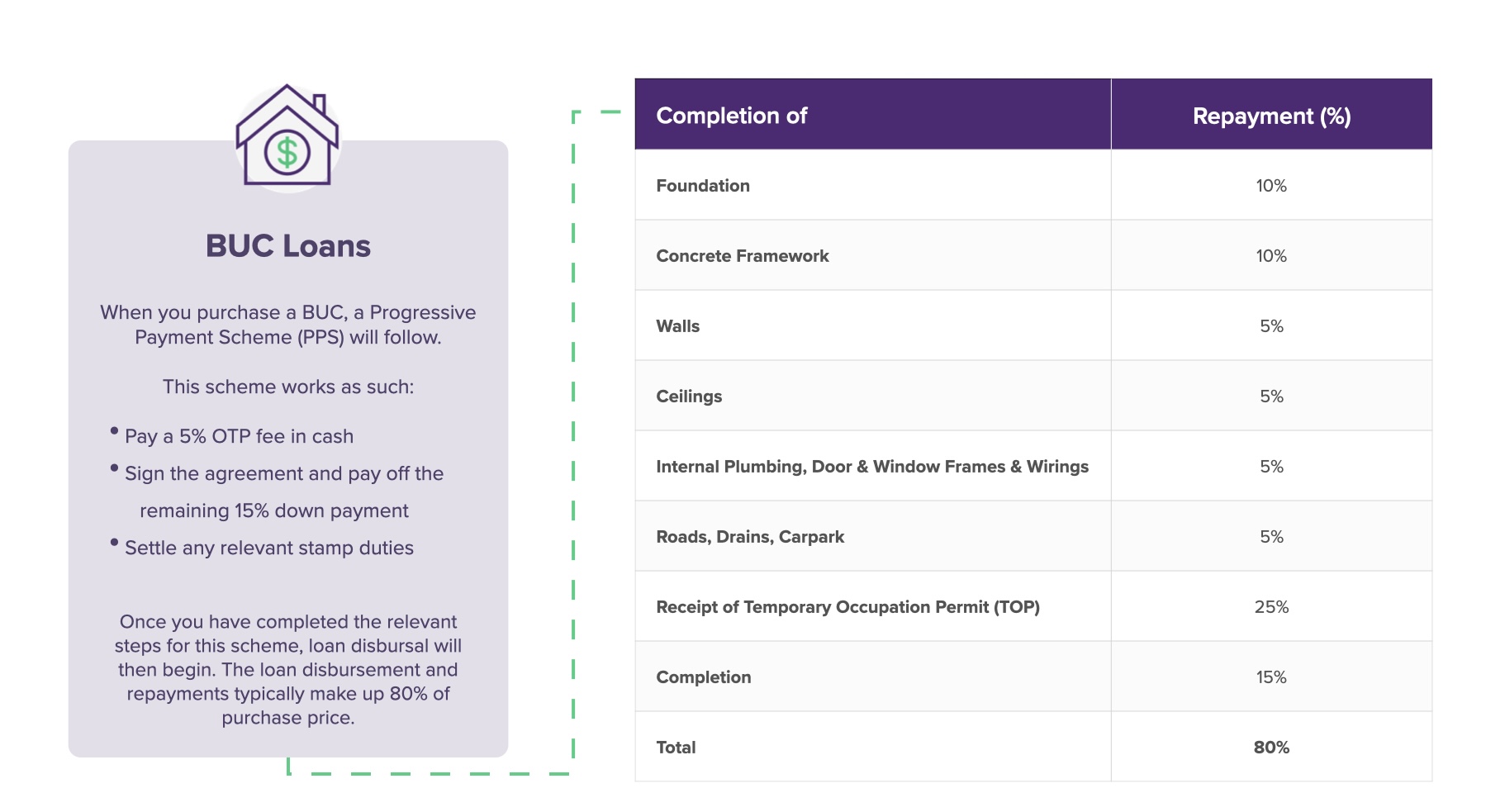

Buildings under construction (BUC) are projects that have not been completed yet. If you are considering purchasing a BUC property,

For many, taking a housing or mortgage loan would be one of the largest loans we would need to take in our lives.

Your home is going to be one of the biggest purchases you will ever make in your life.

![All Critical Factors When Deciding Between SORA and SIBOR [Definitive Guide]](https://www.roshi.sg/wp-content/themes/roshi/images/insights/sora-vs-sibor-home-loans-guide.png)

Have you considered switching from Singapore Interbank Offered Rate (SIBOR) to Singapore Overnight Rate Average (SORA) for your

Have you considered switching from Singapore Interbank Offered Rate (SIBOR) to Singapore Overnight Rate Average (SORA) for your

A home loan is just the starting point of property ownership. For home owners whose lock-in period is ending, refinancing to a lower rate could save thousands over the remaining loan tenure. Those looking to access cash from their property's value without selling can explore home equity loans, which unlock funds for personal or business investment needs.

For quick estimates on affordability, our HDB loan calculator compares HDB concessionary loan repayments against bank loan options while our refinance calculator helps existing home owners estimate potential savings when switching to a new rate.

For bank specific home loan packages and features reviews are available for local banks including DBS, OCBC, Maybank, UOB and Hong Leong as well as foreign banks such as HSBC, Citibank, Standard Chartered Bank, SBI and Bank of China.