A low credit score doesn't define your financial future!

If your score dropped because of a rough patch, licensed moneylenders can still help. They assess your MLCB record, your current monthly income, your existing debt situation and your ability to make repayments.

Borrow what you can repay and use the loan to stabilise your financial situation at the same time avoid getting into recurring unmanageable debt. ![]()

![]()

Get Approved with Bad Credit

How to Improve Your Approval Chances

- Show stable income with recent payslips or CPF statements

- Reduce existing debts before applying

- Borrow only an amount you can comfortably repay

- Bring complete documents to avoid approval delays

- Be honest about your financial situation, lenders check your MLCB report anyway

Rebuilding Your Credit Score

Rebuilding takes time but consistent effort pays off

- Pay all bills and loan on time, every month

- Keep credit card utilisation below 30% of your limit

- Avoid submitting multiple loan applications in a short period

- Check your CBS report regularly for errors

- Check your MLCB report to make sure your moneylender repayments are recorded correctly

- Set up auto payments wherever possible

- Close unused credit lines you no longer need

With consistent on-time payments most borrowers see improvement within 6 to 12 months.

Interest Rate Trends

Research updated by Trinh Thanh on 6 July 2026 - Entering July 2026, Singapore’s consumer lending market continues to remain stable with no major changes to statutory interest rate caps, administrative fee limits or licensed moneylending regulations. Overall lending conditions continue to follow the same regulated framework seen in previous months.

Borrowing demand from individuals with weaker or limited credit histories remains relatively consistent, particularly among borrowers facing temporary financial pressure or difficulties accessing traditional bank financing. Approval patterns continue to depend mainly on current income stability, repayment capacity and supporting documents rather than short term rate movements. Compared to June, there have been no major shifts in approval trends with lenders continuing to assess applications using broadly similar criteria.

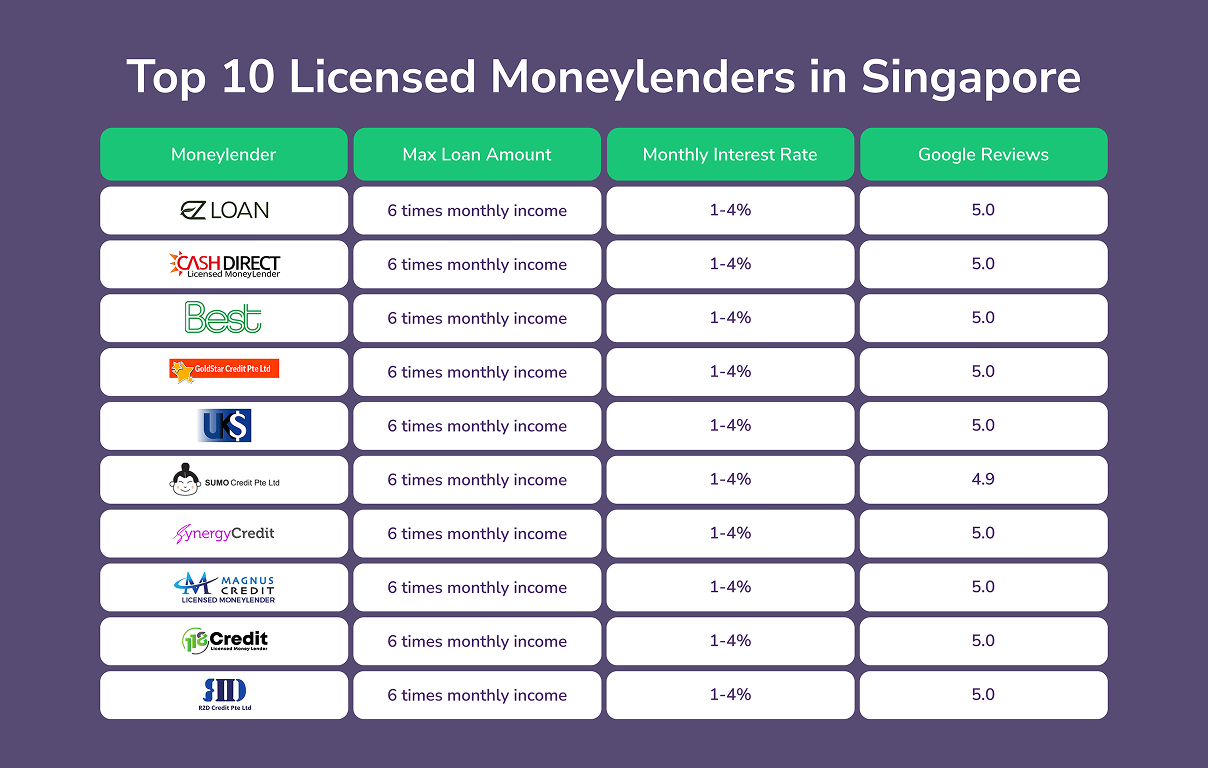

As of July 2026, licensed moneylenders regulated by Singapore’s Registry of Moneylenders continue to remain one of the main borrowing options for individuals with weaker or limited credit histories. Average monthly interest rates continue to stay around 3.8%, remaining slightly below the legal cap of 4% per month. These rates continue to apply within Singapore’s regulated lending structure, including for borrowers who may present a higher level of credit risk.

Although borrowers may still qualify for loan amounts of up to six times their monthly income, lenders continue to place strong focus on verified income, employment consistency, MLCB records and repayment capacity rather than relying only on past credit performance. Administrative fees remain capped at 10% of the principal amount while late payment charges generally continue to stay within the S$60 monthly regulatory limit.

Most applications can still be started online allowing borrowers to submit basic details and supporting documents digitally before visiting the lender’s office.

However, Singapore regulations continue to require borrowers to complete identity verification and sign loan agreements in person before funds can be released. Once this process has been completed many lenders are still able to finalise approvals and disburse funds within the same working day.

Banks in Singapore continue to maintain stricter credit assessment standards for unsecured lending, which continues to limit access for borrowers with adverse or weaker credit records. Personal loans and credit facilities from banks generally continue to offer lower effective interest rates but approvals still depend heavily on credit score, CBS statements, income stability and overall financial profile.

For borrowers with lower credit scores, approval rates remain more limited and additional requirements such as secured collateral or guarantor arrangements may still be necessary depending on the lender and loan type. Bank applications also continue to involve more detailed documentation and longer processing timelines compared to licensed moneylenders.

As a result, banks continue to play a smaller role for borrowers with weaker credit profiles, especially when the borrower requires short term financing or faster access to funds.

In July 2026, bad credit loans continue to highlight the importance of regulated borrowing access and responsible affordability assessment within Singapore’s consumer lending market. Licensed moneylenders remain open to reviewing applications from borrowers with past credit difficulties, provided there is sufficient current income and a reasonable repayment plan in place.

From ROSHI’s perspective, bad credit loans should be used as temporary financial support rather than ongoing borrowing solutions. A weaker credit history does not remove the need for repayment planning. Borrowers should continue reviewing loan terms, repayment obligations and total borrowing cost before committing to any short term financing.

Borrowing through licensed channels also continues to provide greater transparency around fees, repayment terms and legal protections, which remains especially important for borrowers with weaker credit profiles.

For borrowers in July 2026, Singapore’s consumer lending market continues to provide regulated borrowing options for individuals who may not fully meet traditional bank lending requirements. Licensed moneylenders still provide an important financing option for borrowers with weaker or limited credit histories while clear limits on interest rates and fees continue supporting transparency across the market.

Although borrowing costs remain higher compared to standard bank loans, Singapore’s regulatory structure helps reduce the risk of excessive charges and unclear lending practices. Borrowers who keep loan amounts aligned with realistic repayment capacity are generally in a stronger position to manage repayments without creating additional financial strain.

Within Singapore’s regulated consumer lending environment, borrowers who compare loan terms carefully and use short term financing responsibly continue to be better positioned to manage immediate financial needs while supporting longer term financial recovery.