Our Expert says

Is a Small Cash Loan Right for You?

If you only need a few hundred dollars, borrowing a smaller amount is almost always better than borrowing more.

A $500 loan at maximum interest costs about $70 in fees and interest over one month. A $2,000 loan? That's $280. If you only needed $500, you'd have paid $210 extra for nothing.

My advice, calculate exactly what you need, add a small buffer if necessary and borrow the exact amount. ![]()

![]()

Trinh Thanh

Head of Research

Tips for Borrowing Smaller Amounts

Calculate the exact amount you need

Don't round up to, If you need $480, borrow $500 and not $1,000.

Choose the shortest repayment timeline you can afford

1 month costs less than 3 months in total interest but only choose this if you can actually make the repayment.

Compare lenders as rates vary

Not all licensed moneylenders charge 4% monthly interest rate some offer half of that, especially for lower amounts.

Avoid repeat borrowing

One small loan can help but multiple small loans every month is a clear warning sign.

Have a repayment plan

Before you borrow, know exactly how you're gonna repay via what account and at what date.

Loan Amount Overview

Which Amount Do You Need?

Quick overview to choosing the right loan amount:

| If you need | Consider borrowing | Example use |

|---|---|---|

| Under $300 | $300-$500 | Utility bill, groceries |

| $300-$500 | $500 | Minor repair, small medical bill |

| $500-$700 | $600 | Larger utility bills, small emergency |

| $700-$900 | $800 | Minor car or appliance repair |

| $900+ | $1,000 or Personal Loan | Larger expenses |

Interest Rate Trends

Below is an overview of current interest rate trends in Singapore:

Today's moneylender interest rate trends in Singapore

Today's moneylender interest rate trends in Singapore - As of 9 March 2026, licensed moneylenders are charging an average interest rate of approximately

3.98% per month just under the legal cap of 4%.

Monthly Interest Rate Trends (March 2026)

Research updated by Trinh Thanh on 4 March 2026 - As March 2026 progresses, Singapore’s small cash loan segment continues to operate within a predictable and tightly regulated environment. No adjustments have been introduced to statutory interest caps or fee limits and lending activity remains steady across modest loan sizes.

Borrower demand continues to centre on relatively small sums intended to manage short-term liquidity gaps rather than major financial obligations. Requests for amounts such as S$500, S$600 and S$800 remain common, particularly among individuals seeking flexibility for day‑to‑day expenses, minor emergencies or temporary timing mismatches between income and bills. Overall pricing trends have remained broadly consistent with February levels.

Borrower demand continues to centre on relatively small sums intended to manage short-term liquidity gaps rather than major financial obligations. Requests for amounts such as S$500, S$600 and S$800 remain common, particularly among individuals seeking flexibility for day‑to‑day expenses, minor emergencies or temporary timing mismatches between income and bills. Overall pricing trends have remained broadly consistent with February levels.

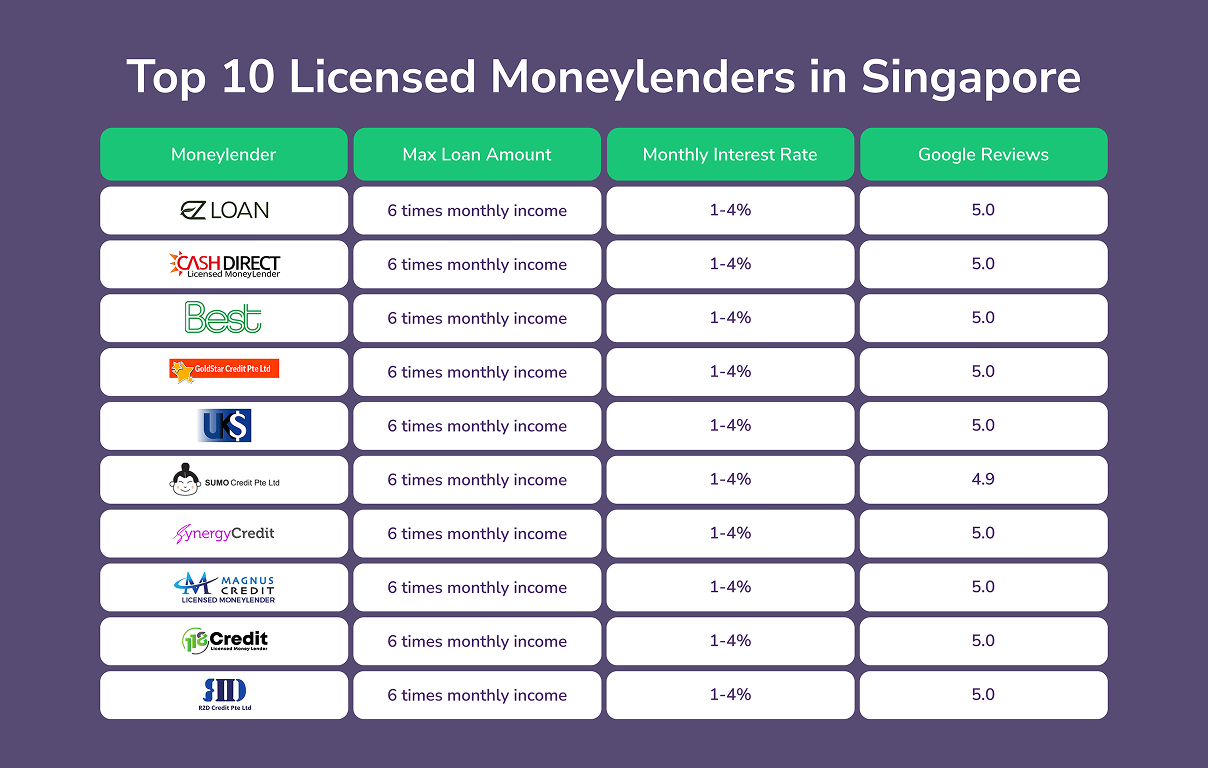

Licensed Moneylenders

As of March 2026, licensed moneylenders overseen by the Registry of Moneylenders under Singapore’s Ministry of Law continue to charge average monthly interest rates of approximately 3.8%, staying just below the legal cap of 4% per month. This rate structure generally applies to small cash loan amounts including S$500, S$600 and S$800, depending on the borrower’s income and risk assessment.

While regulations allow borrowing of up to six times monthly income, small cash loans typically represent only a fraction of this limit. Administrative fees remain capped at 10% of the principal and late fees generally do not exceed S$60 per month. Applications can often be initiated online for convenience with preliminary document submission completed digitally. However, in accordance with Ministry of Law requirements, borrowers must finalise identity verification in person at a licensed outlet before funds are released. Once verification is completed and documentation is in order, approvals for smaller amounts are frequently processed within the same day, preserving accessibility despite the physical verification step.

While regulations allow borrowing of up to six times monthly income, small cash loans typically represent only a fraction of this limit. Administrative fees remain capped at 10% of the principal and late fees generally do not exceed S$60 per month. Applications can often be initiated online for convenience with preliminary document submission completed digitally. However, in accordance with Ministry of Law requirements, borrowers must finalise identity verification in person at a licensed outlet before funds are released. Once verification is completed and documentation is in order, approvals for smaller amounts are frequently processed within the same day, preserving accessibility despite the physical verification step.

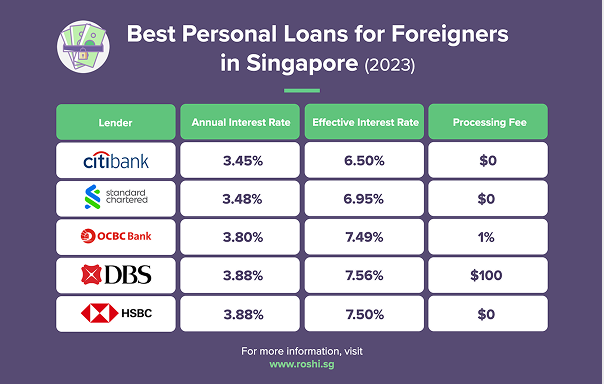

Banks

Mainstream banks in Singapore generally structure their unsecured lending products around higher minimum loan amounts, which makes them less aligned with borrowing needs in the S$500 to S$800 range. Although bank personal loans and credit lines typically offer lower Effective Interest Rates when calculated over longer tenures, they are not specifically designed for low-value, short-duration borrowing.

In practice, the administrative requirements and processing timelines associated with bank loans can outweigh the cost advantage when the amount required is relatively small. As a result, borrowers seeking modest sums for immediate use tend to find licensed moneylenders more responsive to their needs, while banks remain better suited for planned financing of larger amounts.

In practice, the administrative requirements and processing timelines associated with bank loans can outweigh the cost advantage when the amount required is relatively small. As a result, borrowers seeking modest sums for immediate use tend to find licensed moneylenders more responsive to their needs, while banks remain better suited for planned financing of larger amounts.

ROSHI Expert Insight

In March 2026, the small cash loan space continues to reflect a balance between convenience and cost transparency. Licensed moneylenders maintain the ability to release S$500, S$600 or S$800 within compressed timeframes once regulatory checks are completed. Monthly interest rates remain near 3.8%, consistent with the established cap environment rather than market-driven repricing.

From ROSHI’s perspective, small cash loans function best as short bridging tools rather than recurring credit solutions. When repayment is aligned with the borrower’s next salary cycle or near-term income, overall costs remain proportionate to the modest principal involved. Clear disclosure of fees and regulated interest limits further support responsible usage within this segment.

From ROSHI’s perspective, small cash loans function best as short bridging tools rather than recurring credit solutions. When repayment is aligned with the borrower’s next salary cycle or near-term income, overall costs remain proportionate to the modest principal involved. Clear disclosure of fees and regulated interest limits further support responsible usage within this segment.

What This Means for Borrowers

For March 2026, borrowers considering small cash loans will encounter a market characterised by stability and regulatory clarity. Licensed moneylenders continue to provide timely access to S$500, S$600 and S$800 loans, subject to defined interest caps and fee limits. The requirement for in‑person verification remains part of the process but it has not significantly reduced turnaround speed for most applicants.

Given the short-term nature of these loans, maintaining repayment discipline remains essential. When used to address temporary cash flow gaps rather than ongoing financial strain, small cash loans can serve as a practical and contained solution. Singapore’s regulatory safeguards, together with platforms like ROSHI that connect borrowers to licensed providers, help ensure that decisions are made with transparency and awareness of total borrowing costs

Given the short-term nature of these loans, maintaining repayment discipline remains essential. When used to address temporary cash flow gaps rather than ongoing financial strain, small cash loans can serve as a practical and contained solution. Singapore’s regulatory safeguards, together with platforms like ROSHI that connect borrowers to licensed providers, help ensure that decisions are made with transparency and awareness of total borrowing costs