Our Expert says

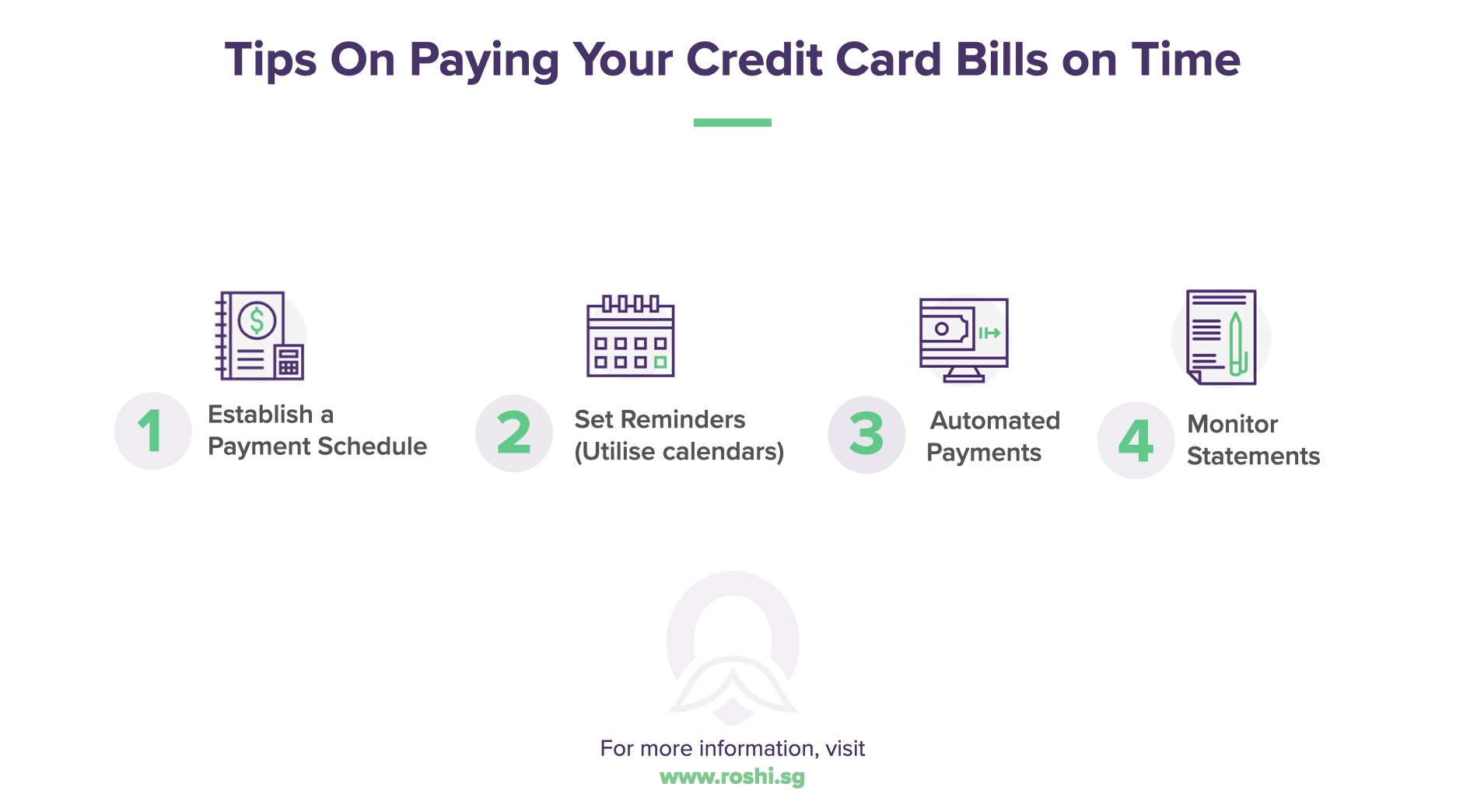

The Minimum Payment Is Not Your Friend

Credit card minimum payments are calculated to maximise interest revenue for the bank not to help you pay off debt. A $10,000 balance with minimum payments only can take over 15 years to clear, costing more than $15,000 in interest which means you'd pay more than double the original amount borrowed.

When using our calculator compare minimum only payments against fixed higher amounts. Even increasing from $200 to $400 monthly can cut payoff time by 70% and save thousands in interest. ![]()

![]()

The True Cost of Minimum Payments

How Minimum Payments Cost You More

Same debt vastly different outcomes based on payment amount.

| Minimum Only ($200) | $400 per month | $600 per month | $1,000 per month | |

|---|---|---|---|---|

| $5,000 | 32 months = $1,400 interest | 14 months = $580 interest | 9 months = $370 interest | 5 months = $210 interest |

| $10,000 | 94 months = $8,800 interest | 31 months = $2,400 interest | 19 months = $1,400 interest | 11 months = $780 interest |

| $20,000 | 180+ months = $26,000+ interest | 76 months = $10,400 interest | 43 months = $5,800 interest | 23 months = $3,000 interest |

Alternatives to High Credit Card Interest

Lower Cost Options to Clear Credit Card Debt

| Option | Interest Rate | Best For |

|---|---|---|

| Balance Transfer | 0% for 6 to 12 months (promotional) | Debt that can be cleared within promo period |

| Personal Loan | 5% to 12% EIR | Debt requiring 1 to 5 years to clear |

| Debt Consolidation Plan | 6% to 11% EIR | Debt exceeding 12x monthly income; MAS-regulated |

![Can’t Pay Back Your Credit Card Debt? Definitive Singapore Guide [Updated 2026]](https://www.roshi.sg/wp-content/themes/roshi/images/insights/paying-off-your-credit-card-debt-guide.png)