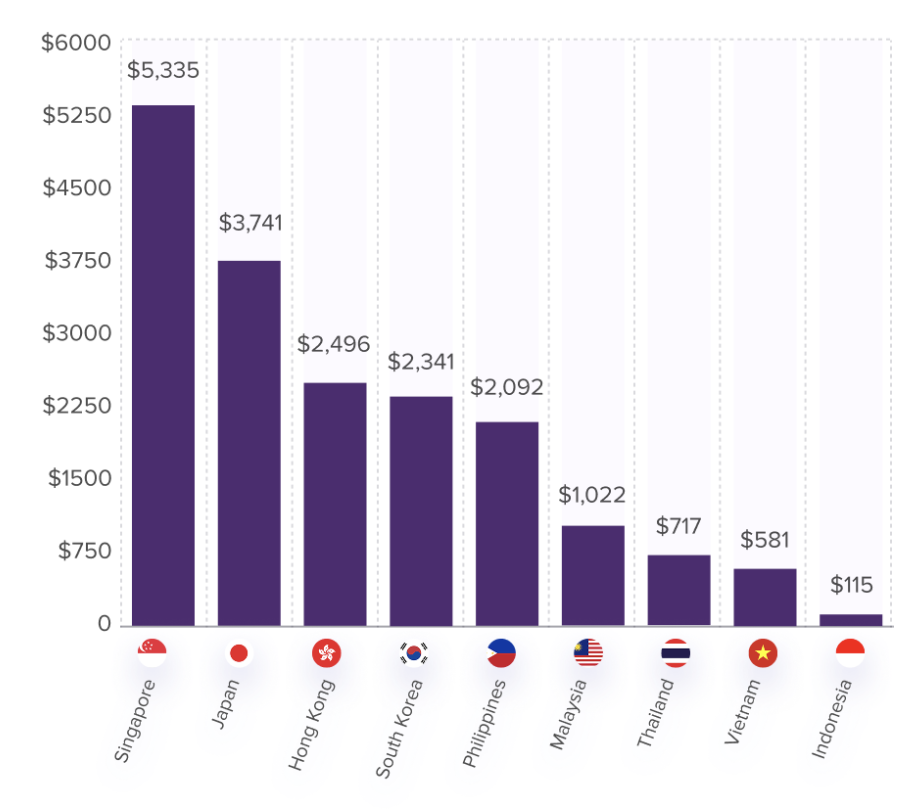

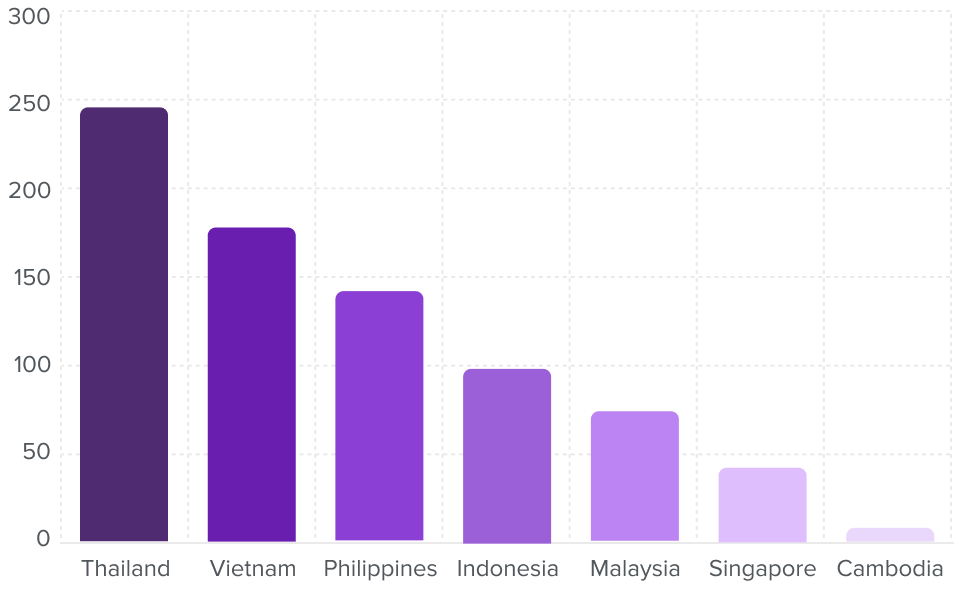

Thailand leads with 246,000 US residents and 14% year on year growth, supported by the Long Term Resident visa and world class private healthcare. Vietnam has surged to second place with 22% annual growth which is the highest in the region and is driven by ultra low living costs, improving urban infrastructure and a 90 day multi entry e-visa introduced in 2023. Both markets are pulling ahead of competitors and show no signs of slowing.

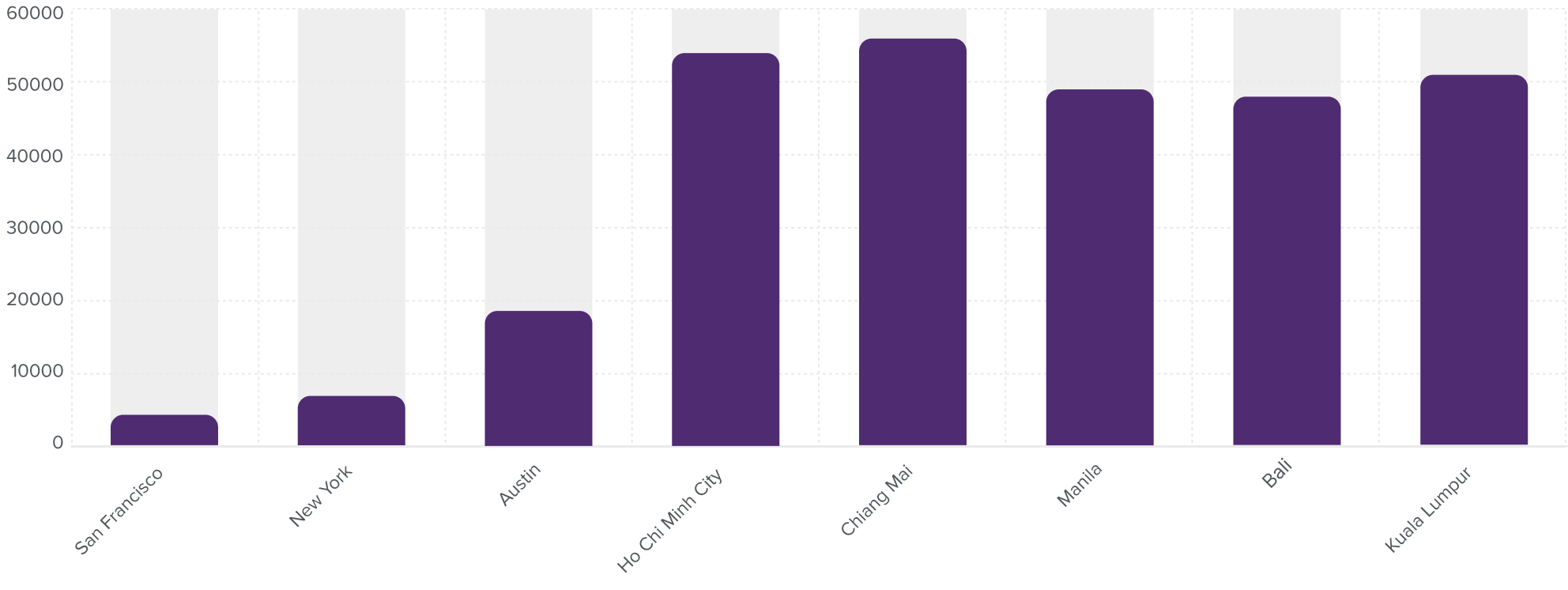

An American earning $85,000 per year retains as little as $4,200 in annual discretionary income in San Francisco after housing, food and transport. The same income in Chiang Mai or Ho Chi Minh City leaves $54,000 to $56,000 which translates into a 13x improvement in purchasing power. This arbitrage is cited by 82% of migrants as a significant or decisive factor in their decision, making it the single strongest pull force across all age groups and professional backgrounds.

The share of digital nomad arrivals converting to stays of one year or more has risen from 12% in 2019 to 34% in 2024. Thailand leads at 44% conversion closely followed by Vietnam at 42%. The normalisation of remote work, improved visa infrastructure and deepening community ties are making indefinite residence increasingly the default outcome not a conscious decision but a series of renewals that accumulate into a life.

Americans aged 50 to 70 remain the dominant migrant group, drawn primarily by healthcare quality to cost ratios that are transformative for those approaching or past retirement age. A procedure costing $40,000 in the US typically runs $6,000 to $8,000 at a top Bangkok or Manila private hospital. For Americans facing pre Medicare years with high private insurance premiums, Southeast Asia offers a financially viable alternative that preserves retirement savings significantly longer than staying in the US.

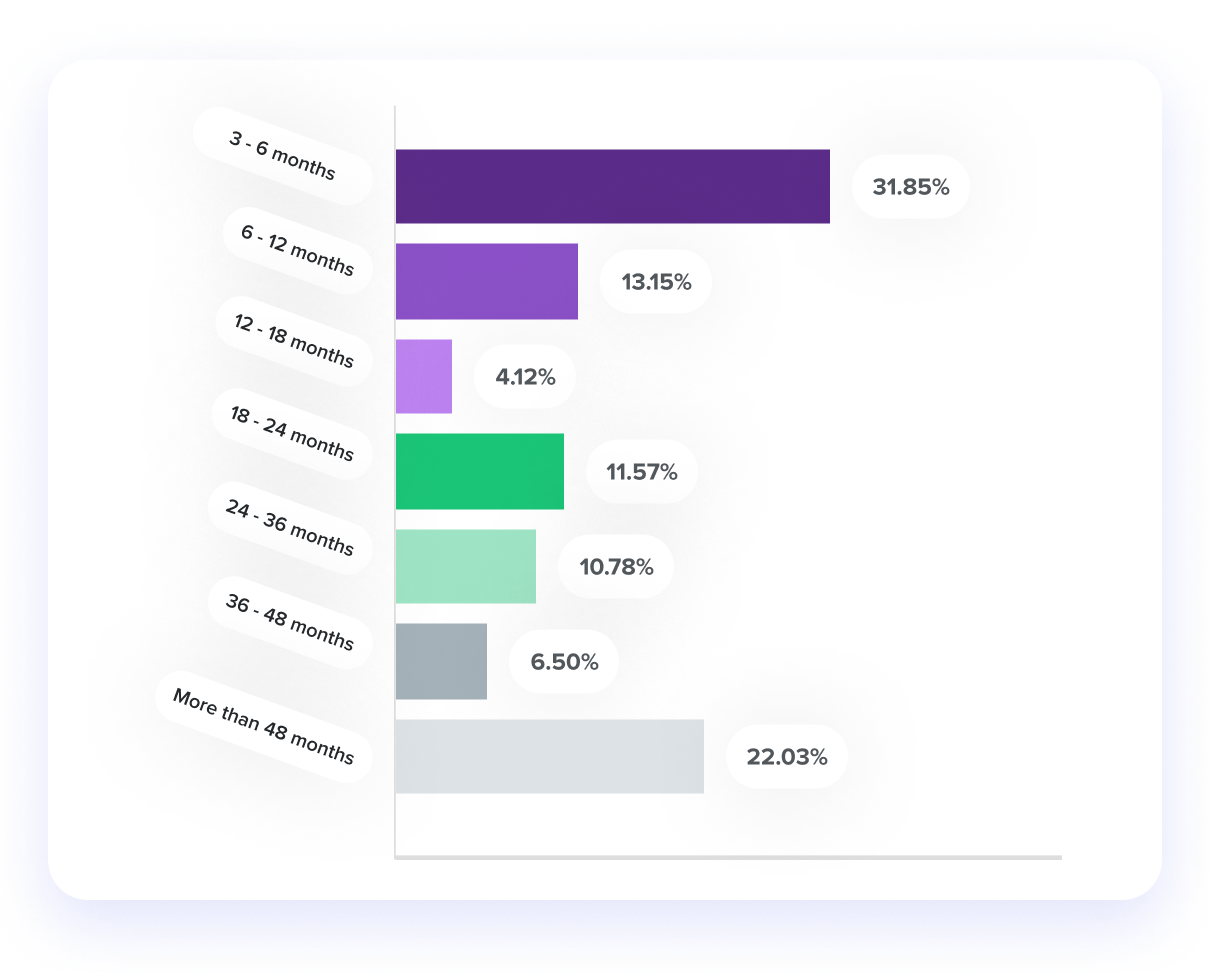

Among Americans who completed an initial SEA stay of 6 months or more and returned to the US, approximately 26% relocated back to the region within 24 months. The primary reasons for initial return were family obligations (44%), visa uncertainty (31%) and healthcare concerns (18%). The high reentry rate signals that the quality of life proposition is robust enough to overcome the frictions of departure and that many “returns” to the US are temporary rather than permanent.

US migrants in SEA fall through the cracks of two financial systems simultaneously: US banks restrict accounts and refuse local products while SEA banks cannot recognise foreign credit history. The result is a $4.2 billion annual unmet demand across personal lending, property finance, insurance and FX with no single provider covering more than two or three of the nine core product needs. 71% of migrants would pay $30 to $80 per month for an integrated cross border financial platform. No such product currently exists at scale.

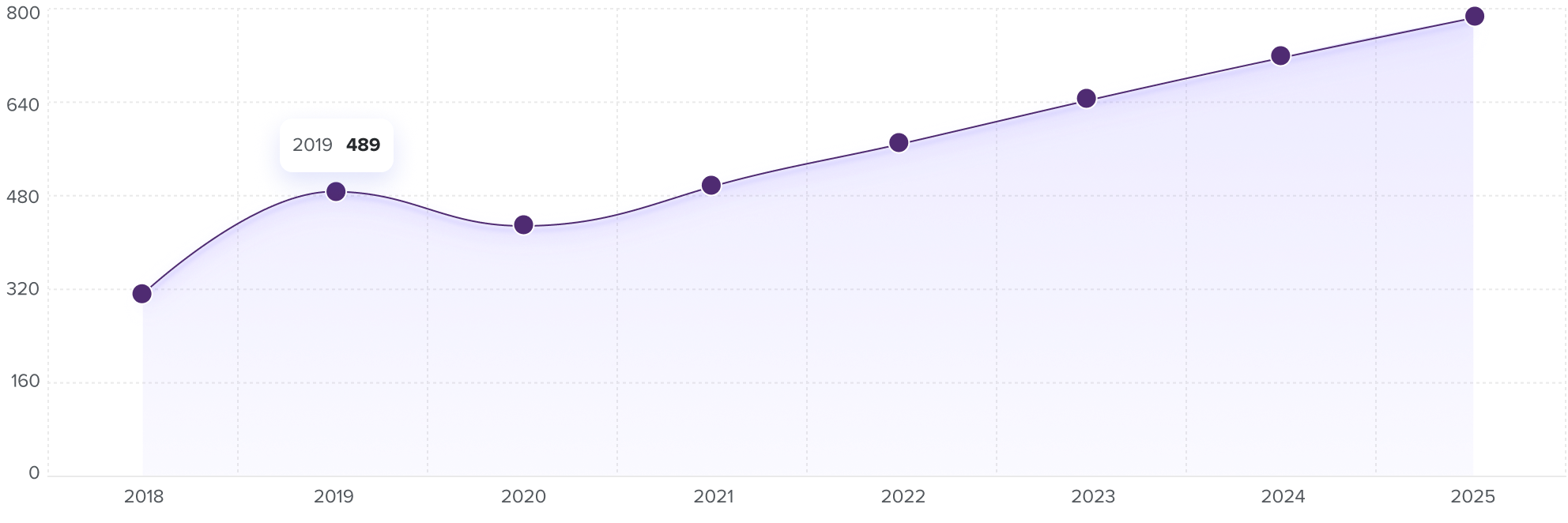

The United States has long maintained a significant overseas diaspora which the State Department estimates to be approximately 9 million American citizens which are currently living abroad. Southeast Asia has historically accounted for a small share of this population. What has changed dramatically over the past five years is the velocity of movement into the region particularly from Americans in the age bracket of 25 to 45 years and those approaching or in retirement.

The following structural forces explain the surge. First, the post COVID normalisation of remote work severed the geographic link between employment and location for roughly 22 million US workers, many of whom began exploring lower cost, higher quality of life alternatives abroad. Second, US inflation reached 40 year highs between 2022 to 2023, accelerating cost of living comparisons that made Southeast Asian cities look dramatically more affordable. Third, several SEA governments responded with long stay visa programmes. Thailand's Long Term Resident Visa (2022), Vietnam's enhanced e-visa (2023) and Indonesia's Second Home Visa (2022) directly targeting the affluent foreign resident market.

Thailand continues to dominate as the most popular destination for US citizens accounting for nearly a third of the total population. Vietnam has overtaken the Philippines to claim second place, driven by low costs, improving infrastructure and a rapidly expanding digital economy. Singapore, while home to a large American professional community, increasingly functions as a transit hub rather than a final destination due to prohibitive living costs.

| Est. US Residents (2025) | YoY Growth | Primary Visa Type | Key Driver | |

|---|---|---|---|---|

| 🇹🇭 Thailand | 246,000 | +14% | LTR Visa / METV | Cost, infrastructure, healthcare |

| 🇻🇳 Vietnam | 178,000 | +22% | E-Visa (90-day multi) | Low cost, culture, startup scene |

| 🇵🇭 Philippines | 142,000 | +8% | SRRV / 13A | English language, familiarity |

| 🇮🇩 Indonesia | 98,000 | +18% | Second Home Visa | Bali lifestyle, digital nomad hubs |

| 🇲🇾 Malaysia | 74,000 | +11% | MM2H Programme | English, regional hub access |

| 🇸🇬 Singapore | 42,000 | +3% | EP / PEP | Finance, professional roles |

| 🇰🇭 Cambodia | 8,000 | +6% | E-Class Business Visa | Ultra low-cost, ease of entry |

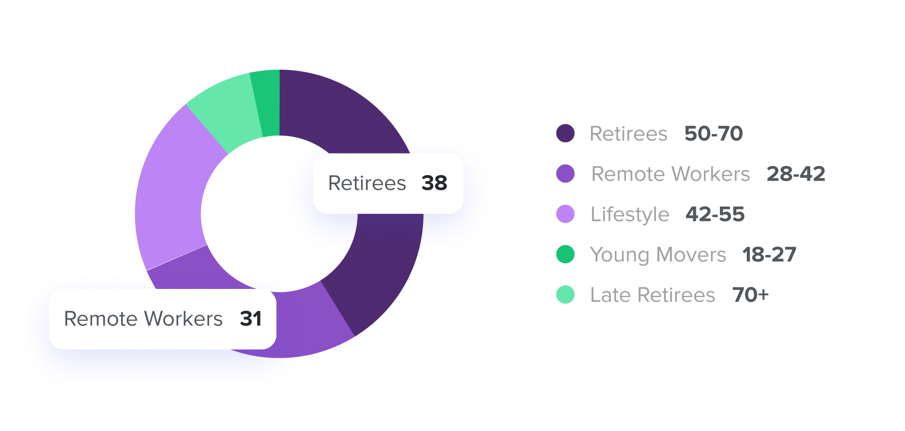

Contrary to the stereotype of the Southeast Asia expat as a young backpacker or retiree escaping cold weather, the 2025 remigrant is a more diverse and economically significant profile. Retirees remain the largest single cohort but the fastest growing segment is remote workers aged 28 to 42 years usually college educated, earning US salaries and seeking to dramatically extend their purchasing power.

The Retirement Cohort (50 to 70): Still the largest group at 38% of total migrants, retirees are drawn primarily by healthcare quality to cost ratios and the ability to live comfortably on Social Security and retirement savings that would be inadequate in most US cities. Thailand and the Philippines dominate this segment.

The Remote Worker Cohort (28 to 42): At 31% of migrants and growing at twice the overall rate, this group earns median US salaries between $85,000 to $110,000 which translates to a dramatically elevated standard of living in Vietnamese, Thai or Indonesian cities. Ho Chi Minh City, Chiang Mai and Canggu (Bali) have become established hubs.

The Lifestyle Transition Cohort (42 to 55): Representing 21% of migrants these are professionals who have partially or fully exited the US workforce and are trading urban American careers for entrepreneurship, consulting or semi retirement in the region.

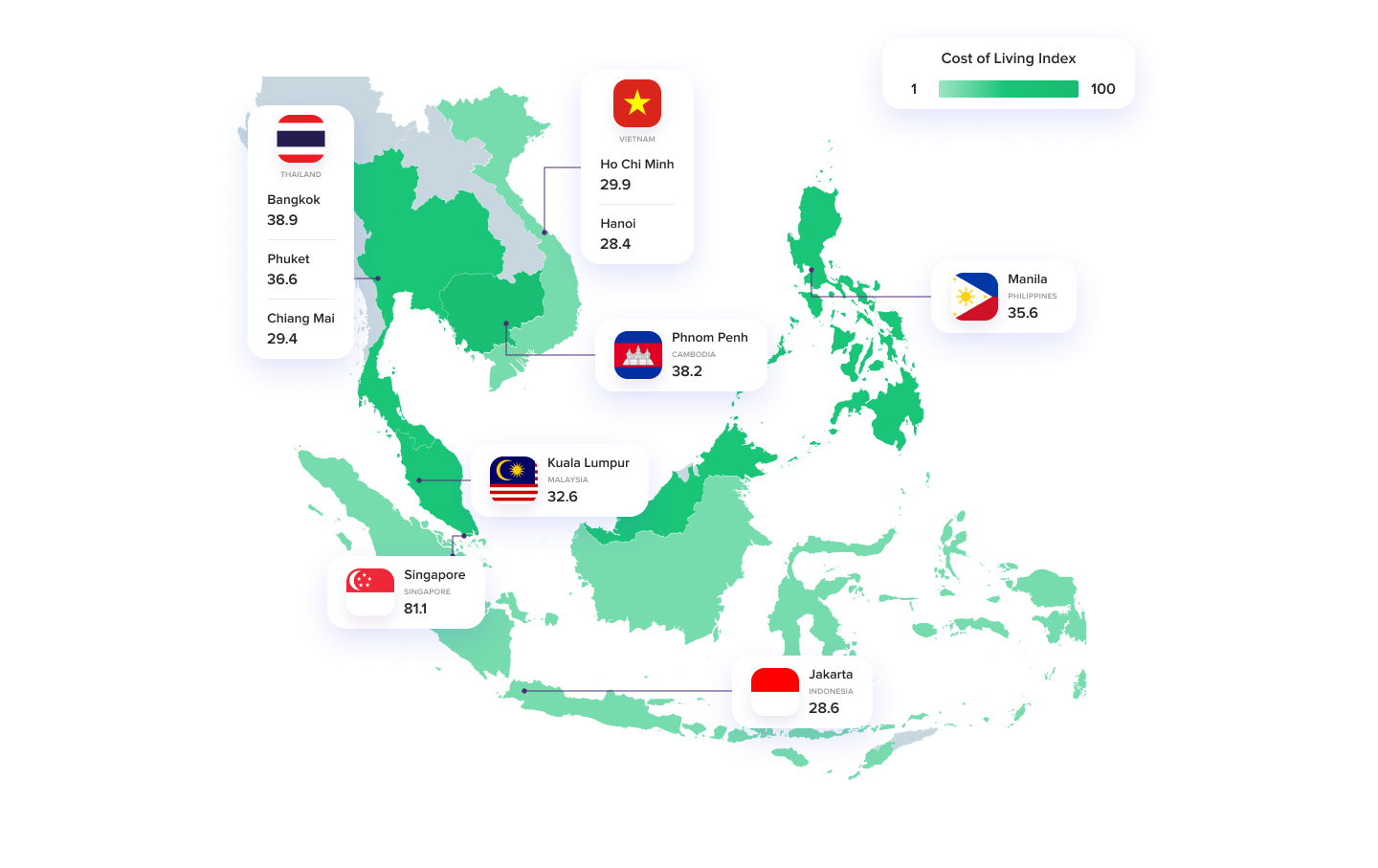

Thailand remains the undisputed leader for US remigrants combining world class private healthcare at 15 to 20% of US costs, an expat infrastructure built over four decades and the 2022 Long Term Resident (LTR) visa targeting higher income earners and retirees with a 10 year renewable permit. Chiang Mai consistently ranks in global top five lists for digital nomad liveability while Bangkok offers urban sophistication at a fraction of New York or San Francisco costs. The 94% adoption of PromptPay digital banking eases financial integration for new arrivals.

Vietnam's climb to second place is the defining story of the 2020s remigration wave. A combination of near zero crime in major cities, extraordinary food culture, a rapidly modernising urban landscape and some of the lowest living costs in the region has made Ho Chi Minh City and Hanoi magnets for younger American migrants. Vietnam's 2023 expansion of its e-visa to 90 day multi-entry has reduced administrative friction significantly. The country's dynamic startup ecosystem and young English speaking population add professional appeal for remote workers and entrepreneurs.

The Philippines benefits from a unique advantage no other SEA market can replicate. It is the only country in the region where English is a language, eliminating the language barrier that deters many older Americans from other markets. The Special Retiree's Resident Visa (SRRV) provides a clear pathway to long term residency. Growth is moderated by infrastructure challenges in secondary cities and concerns around weather events but Manila, Cebu and Davao continue attracting strong flows from the US West Coast where Filipino American community ties ease the cultural transition.

Indonesia's remigrant story is almost entirely told through Bali which has evolved from a tourist destination into a globally recognised remote work and lifestyle hub. The 2022 Second Home Visa (5 or 10 years renewable) was explicitly designed to capture this market. Canggu, Seminyak and Ubud have developed dense ecosystems of co-working spaces, international schools and Western standard healthcare. Indonesia's challenge is the concentration effect as most US migrants cluster in southern Bali creating pockets of high demand and rising costs that undermine the affordability argument for newcomers.

Malaysia's My Second Home (MM2H) programme, despite periodic tightening of financial requirements, remains one of the most structured and credible long term residency options in the region. Kuala Lumpur offers genuine cosmopolitan living, strong English usage, excellent private healthcare, world class transport infrastructure and proximity to the rest of Southeast Asia at roughly 40% of equivalent Singapore costs. Malaysia's multicultural food and cultural environment is particularly attractive to American migrants with diverse backgrounds. Growth has been moderate partly due to periodic policy uncertainty around MM2H eligibility criteria.

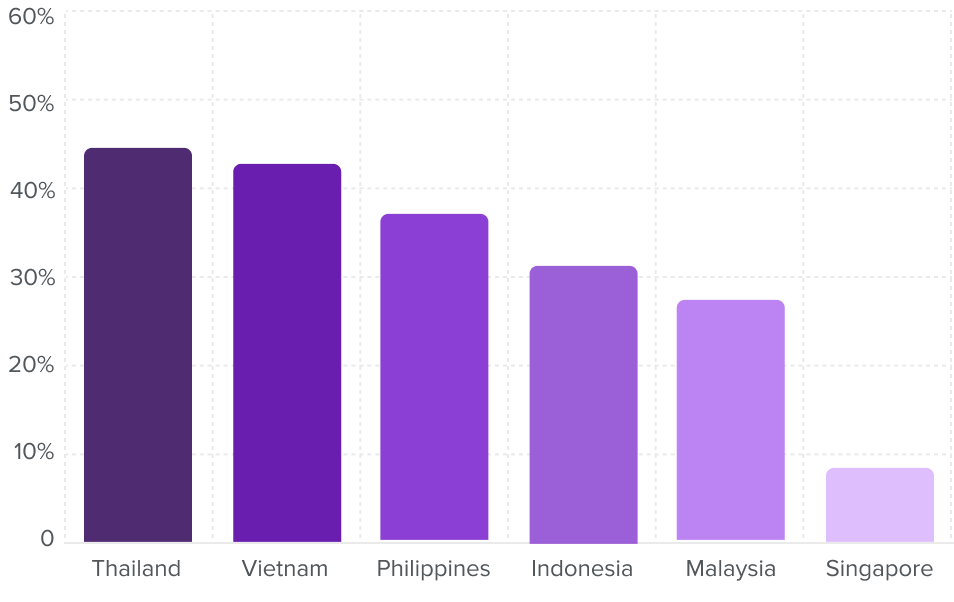

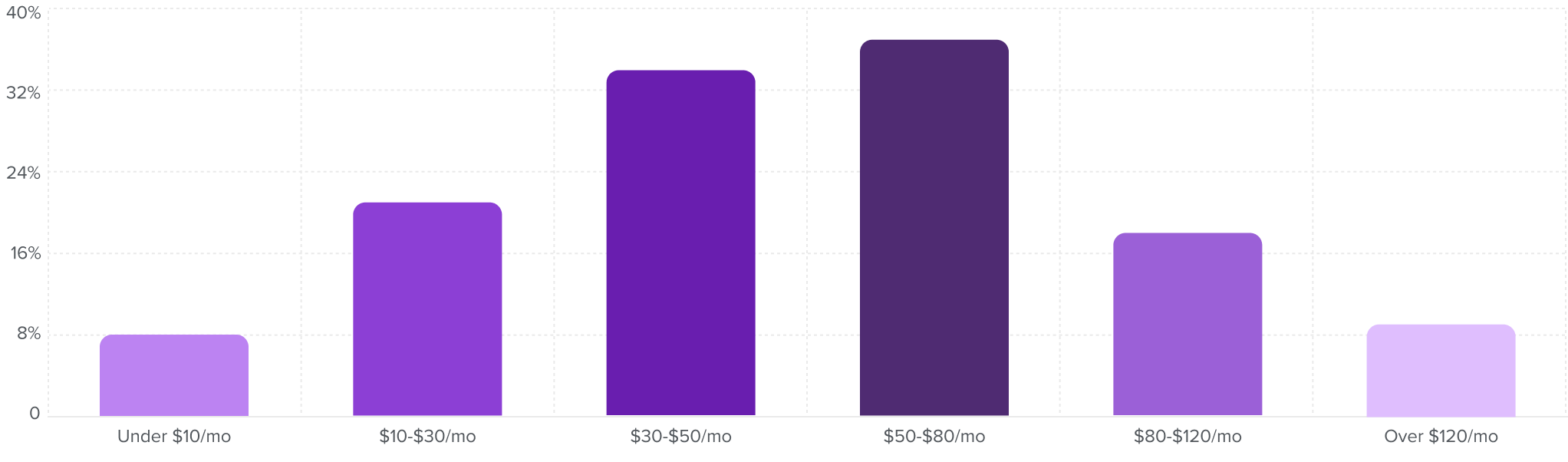

A defining structural shift in this migration wave is the conversion rate from temporary digital nomad stays to long term or permanent residence. In 2019, this conversion was estimated at 12%. By 2024, it had risen to 34% reflecting both improved visa infrastructure and a deepening of community ties that makes return to the US feel increasingly optional.

Thailand leads conversion rates at 44%, driven by the LTR visa's deliberately low friction and a mature support ecosystem, immigration attorneys, relocation agencies and expat communities that reduce the administrative burden of transitioning from visitor to resident. Vietnam's 42% conversion reflects the pull of its rapidly improving urban quality of life and the growing normalcy of building a long term life there. The Philippines lags on conversion partly due to ongoing infrastructure gaps outside Metro Manila though SRRV uptake among retirees keeps absolute numbers significant.

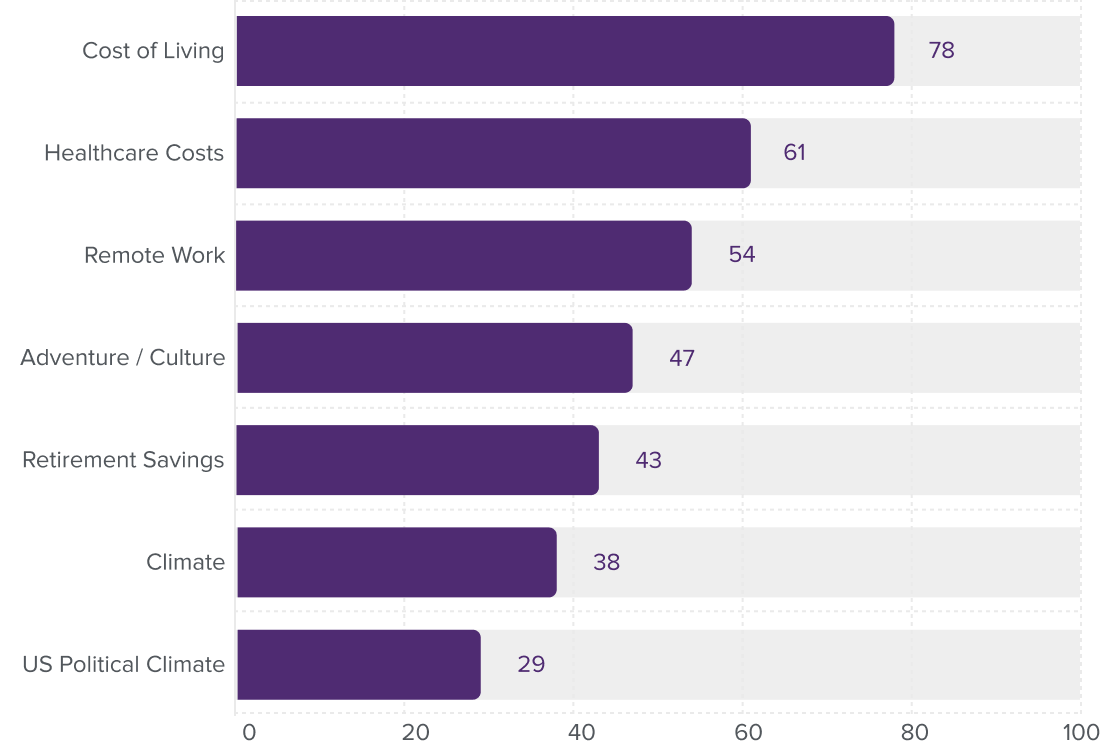

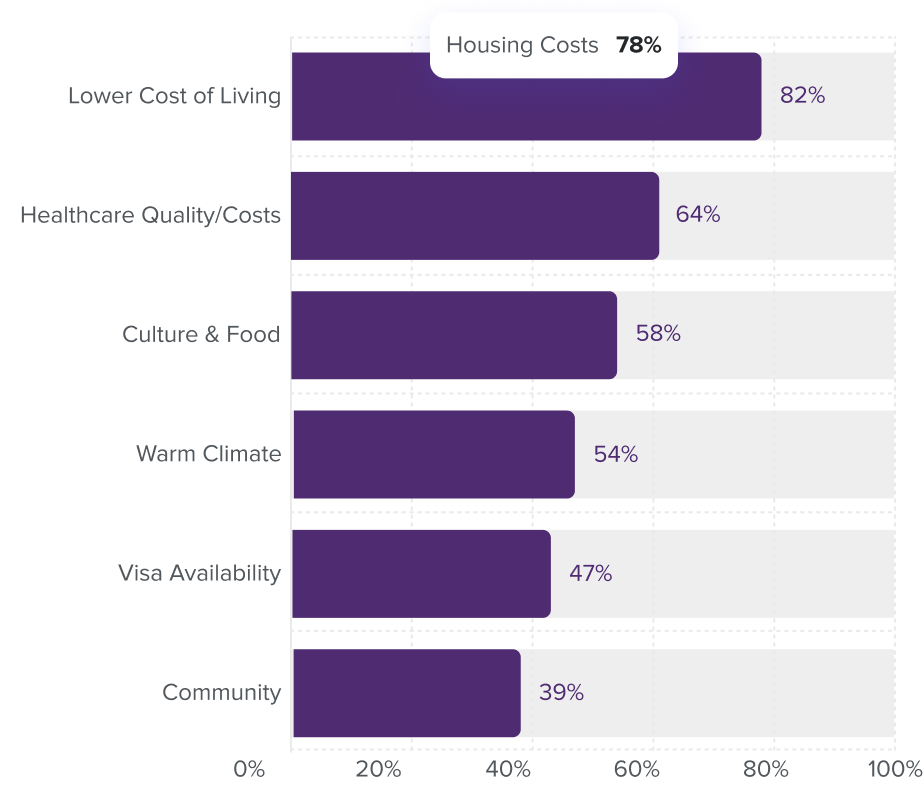

Understanding the Great Remigration requires understanding what is pushing Americans out as much as what is pulling them toward Southeast Asia. Our survey data identifies a consistent cluster of US structural factors that appear repeatedly across all demographic segments and destination markets.

Housing unaffordability is cited by 78% of respondents as a significant or decisive factor which is the highest of any push variable. The US median home price surpassed $420,000 in 2024 while rental costs in major metros have increased 40 to 60% since 2019. For Americans without existing property wealth, home ownership has become effectively unattainable in coastal cities.

Healthcare costs rank second particularly among migrants over 45 who face the prospect of pre Medicare years with high private insurance premiums. Thailand's world class private hospitals where a comparable procedure costs 20 to 30% of US prices are a decisive factor.

One of the more striking data points from our research is the rate of return migration. Americans who tried Southeast Asia returned to the US and then moved back to the region within two years. This figure stands at approximately 26% among those who completed an initial stay of 6 months or more. The primary reasons cited for initial return were family obligations (44%), uncertainty about long-term visa status (31%) and healthcare concerns (18%). Among those who return, Vietnam and Thailand see the highest reentry rates suggesting that the quality of life benefits are strong enough to overcome the frictions of the first departure.

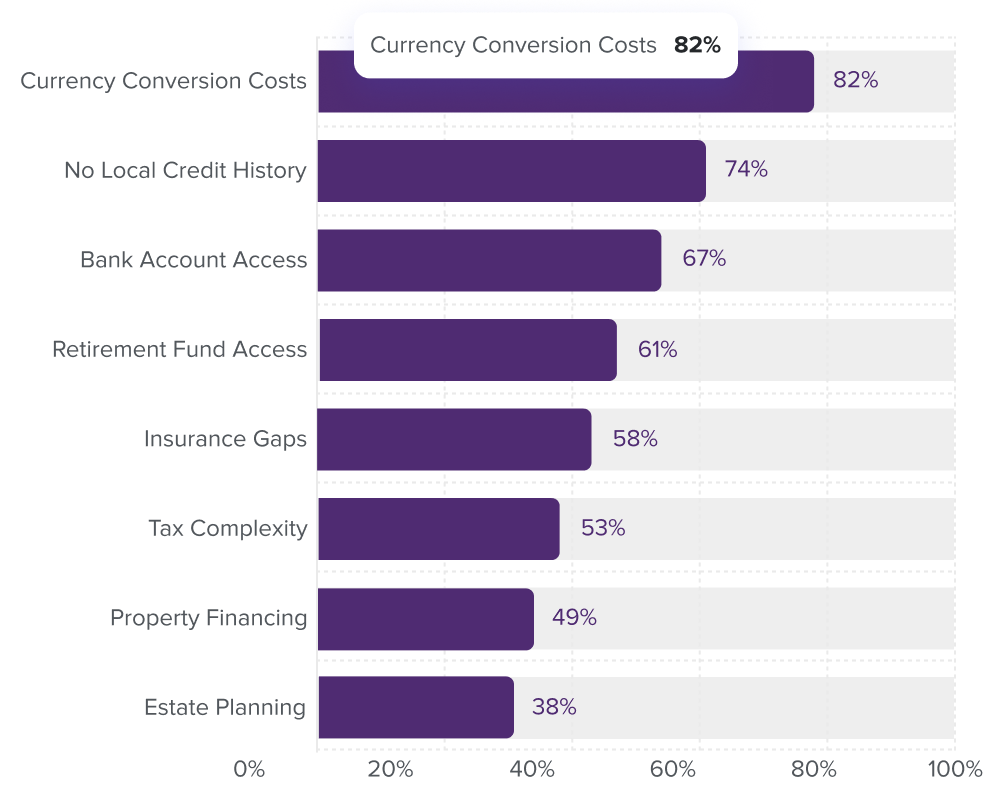

American lifestyle migrants represent one of the most financially significant and least well-served consumer segments in Southeast Asia. They arrive with US denominated income and assets, face complex cross-border financial needs and discover that neither US based financial institutions nor local SEA banks are designed to serve them well. The result is a structural gap estimated at $4.2 billion in unmet annual financial services demand.

Currency conversion costs top the list with migrants typically running 100% of their living expenses through USD to local currency conversions. Those relying on bank wire transfers or ATM withdrawals pay estimated annual fees of $1,800 to $3,200 on a $4,000 per month budget which can be translated into a silent tax of 4 to 7% on their entire expenditure. Fintech solutions like Wise and Revolut have captured significant share here but remain incomplete solutions particularly for larger transactions like property deposits or vehicle purchases.

Credit invisibility is the defining structural barrier. Americans who spent decades building strong US credit profiles arrive in SEA as credit nonentities. Local banks have no mechanism to import, recognise or proxy US FICO scores. The result: no local credit cards, no mortgages, no car loans, no personal credit lines regardless of income level or financial history. A retired American with a $1.2M investment portfolio and 800 FICO score cannot get a $5,000 credit card from a Thai bank.

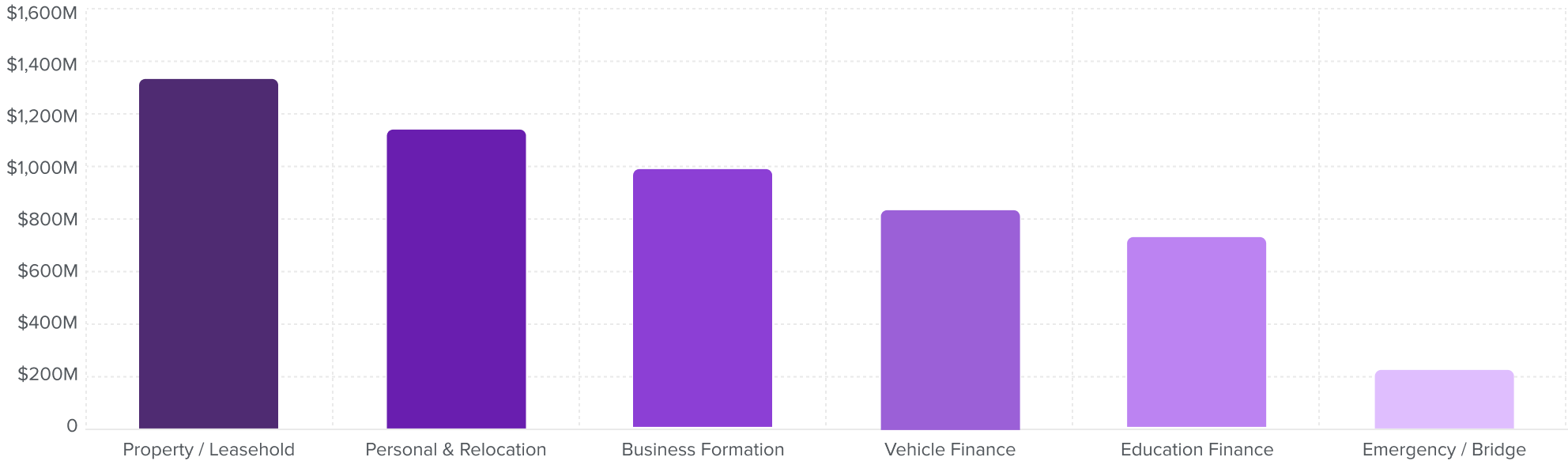

Property financing represents the largest single lending opportunity at an estimated $1.4 billion annually. Despite legal restrictions on foreign freehold ownership in Thailand and Vietnam, long term leasehold structures, condo purchases and developer financing arrangements create substantial demand for mortgage equivalent products. Most migrants currently finance property through U -based home equity lines or cash both suboptimal.

Personal loans and relocation financing constitute the highest frequency product need. Migrants face large upfront costs such as visa deposits, apartment deposits (often 3 months in advance), furniture, vehicle purchases and school fees which arrive before local income streams are established. This is a natural short to medium term lending window that local banks are structurally unable to serve and US banks will not touch.

Business formation loans are the fastest growing category, driven by the lifestyle entrepreneur cohort. Americans starting cafés, co-working spaces, online businesses or consulting practices in SEA require startup capital of $20,000 to $150,000 which is usually too small for institutional lenders, too large for personal savings and structurally excluded from local SME lending programmes that require local ownership or tax history.

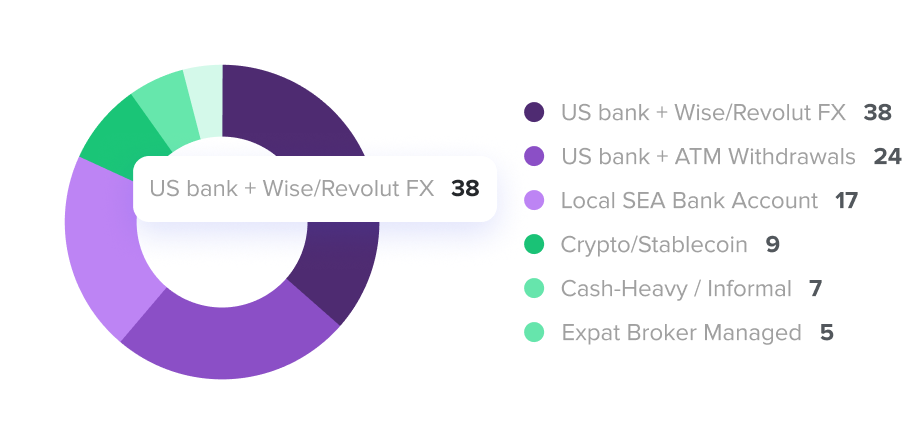

The current landscape is characterised by improvisation rather than design. The most common arrangement which is maintaining a US bank account and withdrawing cash or transferring via Wise works well for day to day spending but breaks down entirely for any financial product requiring local identity, local credit history or local income verification. Three specific failure points stand out:

Retirement account access. Americans drawing from 401(k) or IRA accounts face a cascade of problems: mandatory 20 to 30% US tax withholding on distributions, unclear tax treaty treatment in most SEA countries and no local financial institution able to act as an intermediary or provide advice. Many end up significantly over taxed or adopt aggressive structures to minimise withholding.

Insurance gaps. US health insurance is largely non-functional outside the country. International health insurance products exist but are expensive, poorly understood and often purchased through brokers with misaligned incentives. Life insurance, income protection and property insurance all have equivalent gaps. This is a $340 million+ annual premium opportunity that is currently served by a fragmented, low trust market of international brokers.

Estate and succession planning. Americans who purchase assets in SEA whether property, business stakes or investment accounts face genuinely complex cross border estate planning needs. US wills do not automatically govern SEA situated assets. Local inheritance law may conflict with US intentions. Very few financial or legal advisors are qualified to operate across both systems and the ones who do charge premium rates put them out of reach for most migrants.

The competitive landscape for US migrant financial services in SEA is fragmented, immature and ripe for consolidation. No single player currently offers a comprehensive cross border financial product stack. The market is served by four overlapping categories of providers each with significant limitations.

| Examples | What They Do Well | Critical Gaps | Market Share Est. | |

|---|---|---|---|---|

| US Challenger Banks | Charles Schwab, Citibank Global | Fee-free ATM withdrawals, USD holding | No local credit, no SEA products, account restrictions | 34% |

| FX / Transfer Fintechs | Wise, Revolut, OFX | Low-cost FX, multi-currency wallets | No lending, no insurance, limited local integration | 28% |

| Local SEA Banks | Bangkok Bank, BDO, CIMB | Local accounts, some foreigner-friendly branches | No credit history recognition, limited English service | 21% |

| Expat Brokers / Advisors | deVere Group, Henley & Partners | Wealth management, international insurance | High fees, commission conflicts, limited mass market reach | 11% |

| Local Loan Marketplaces | ROSHI (SG), various | Loan matching, local lender access | Early stage for US migrant segment specifically | 6% |

| US Banks | FX Fintechs | Local Banks | Expat Brokers | Loan Marketplaces | |

|---|---|---|---|---|---|

| Day-to-day spending / FX | |||||

| Local bank account | |||||

| Personal loans (local) | |||||

| Property / leasehold financing | |||||

| Credit history building | |||||

| International health insurance | |||||

| Retirement account access | |||||

| Business formation lending | |||||

| Tax / estate planning |

The coverage map reveals a consistent pattern: every provider category has meaningful strengths in one or two areas and critical absences everywhere else. No player currently offers what migrants actually need, a unified financial relationship that spans USD asset management, local-currency spending, credit building, lending, insurance and cross border tax guidance. This white space is the defining commercial opportunity in the segment.

Based on migrant survey data and competitive gap analysis, we identify five product pillars that together constitute a comprehensive financial solution for US lifestyle migrants in SEA. The first player to offer all five in an integrated, low friction package will capture disproportionate market share in a segment growing at 15% annually.

Willingness to pay data is encouraging for product developers. 71% of surveyed migrants indicate they would pay $30 to $80 per month for a genuinely integrated cross border financial platform, a figure that compares favourably with the $150 to $300 per month they currently spend on fragmented, suboptimal alternatives. At 788,000 residents and growing, even 10% platform capture at $50 per month represents a $47 million annual recurring revenue base before any lending margin is included.

The Great Remigration is not a marginal lifestyle phenomenon it represents a structural reallocation of American human and financial capital toward Southeast Asia, driven by compounding cost of living pressures in the US and dramatically improved access, infrastructure and policy frameworks across the region. The trend has self-reinforcing characteristics: as communities grow, the barriers for subsequent migrants fall, accelerating flows further.

DISCLAIMER & METHODOLOGY

This information herein is published by ROSHI Pte Ltd (UEN 202222480E) (“ROSHI”) and is produced for informational purposes only. Population estimates are derived from a combination of US State Department Overseas Citizens Services registration data (acknowledged to capture 30% of actual overseas residents), visa issuance data from SEA government sources, expat community platform surveys (n≈2,400 across six markets, 2024) and cross referenced secondary sources including the Association of Americans Resident Overseas (AARO) and InterNations Global Expat Index.

Where no primary data source exists, figures represent modelled estimates using stated extrapolation methodologies. All estimates should be treated as indicative orders of magnitude rather than census-grade figures. This report does not constitute financial, legal or immigration advice.

ROSHI performs marketing and matchmaking services to connect clients with lending partners but does not directly offer any lending or financial advisory services under regulation by the Monetary Authority of Singapore. Users of this report should consult professional advisors before engaging in any transaction.

This report is meant solely for insight purposes following Singapore laws and regulations around data privacy. Please contact ROSHI for authorization before reproducing or relying on the analysis.