We’re likely to see a shift in payment preferences from credit cards to BNPL as consumers show greater satisfaction with many BNPL features. 42.1% of consumers chose BNPL because it provides the best terms, while only 17.5% chose credit card payments for the same reason. It seems that BNPL is also becoming more accessible as 32.7% paid BNPL because the merchant offered it as an option, significantly higher than the 9.5% of credit card users who stated the same reason.

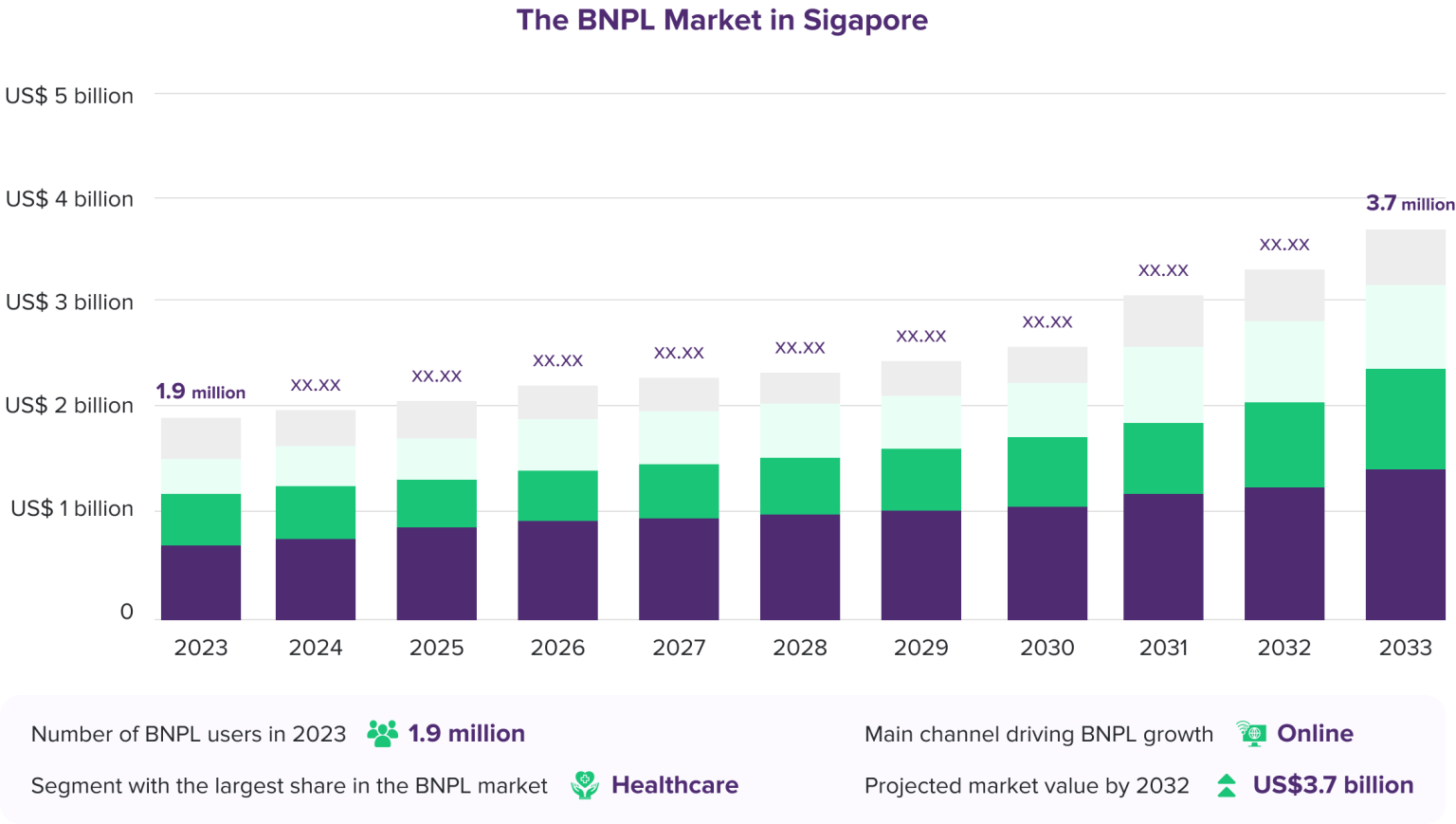

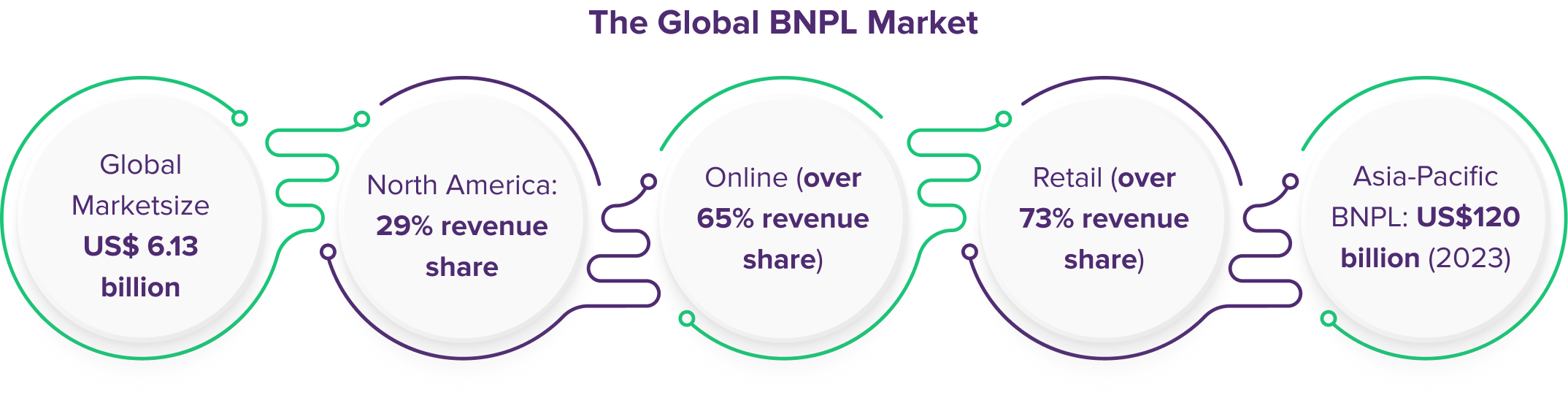

Both globally and within Singapore, the BNPL market is expected to grow at a steady rate. Globally, the market is forecasted to grow at 26.1% CAGR from 2023 to 2030. In the Asia-Pacific region, BNPL payments are outpacing payments by cash and debit cards, as BNPL captures 4% of e-commerce transactions in the region. Valued at US$1.2 billion in 2022, the Singapore BNPL market is projected to reach US$3.7 billion by 2032.

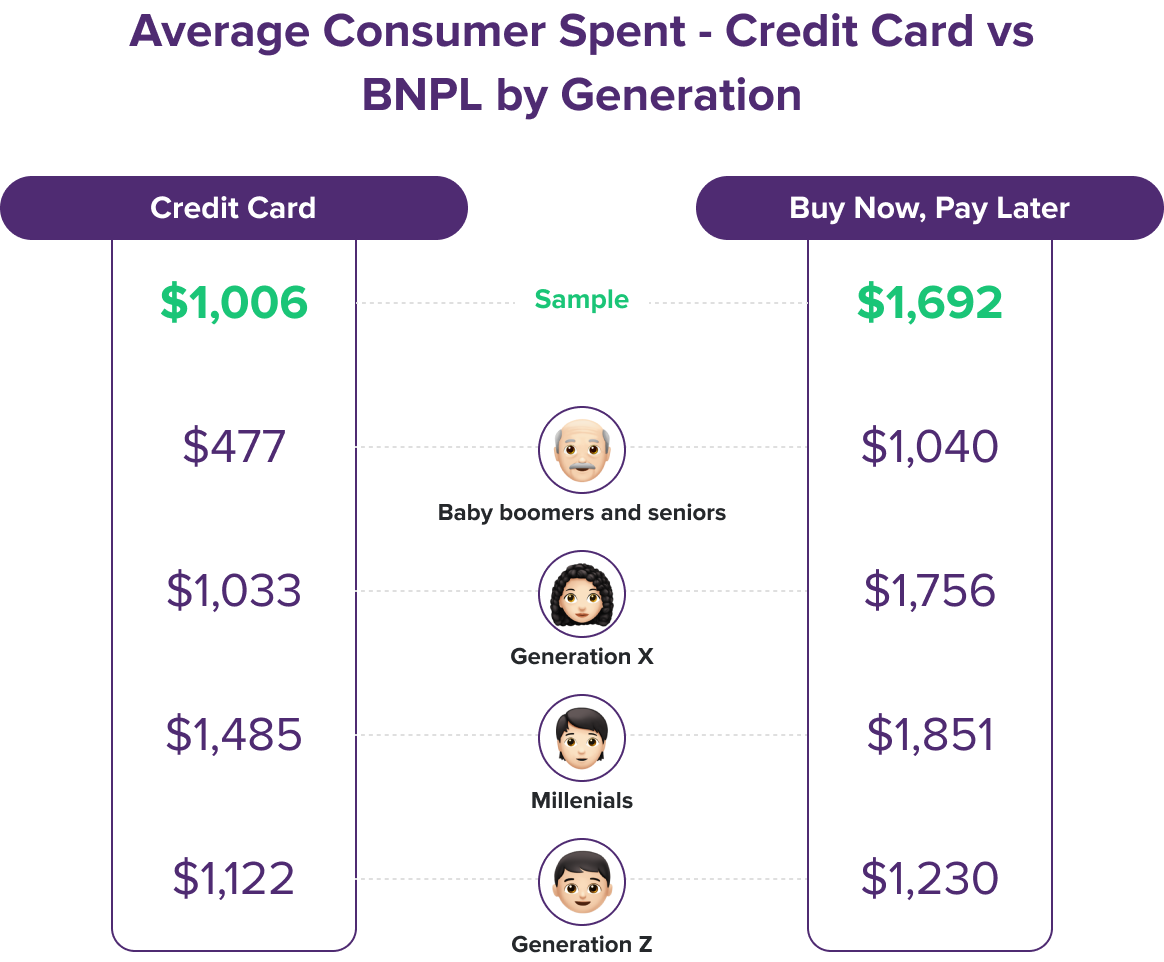

Although BNPL is making headwinds with younger consumers, it is unlikely to replace more established traditional lending systems. Still, it is worth noting that BNPL purchases are approximately 70% higher than that of credit card purchases. To meet the changing preferences and evolving financial needs of consumers, credit card issuers and traditional lending institutions must innovate their services.

As Singapore moves closer to being a cashless society, most consumers now prefer using digital payments for their purchases both online and in-store. Aside from these convenient payment options, many are also opting to use flexible financing terms such as buy now, pay later schemes. The question is, how safe and financially sound is BNPL?

Buy now, pay later (BNPL) is a short-term financing model that allows consumers to pay for their purchases in smaller, more manageable monthly instalments. It works pretty much the same way as some credit card instalment payments but with slight nuances.

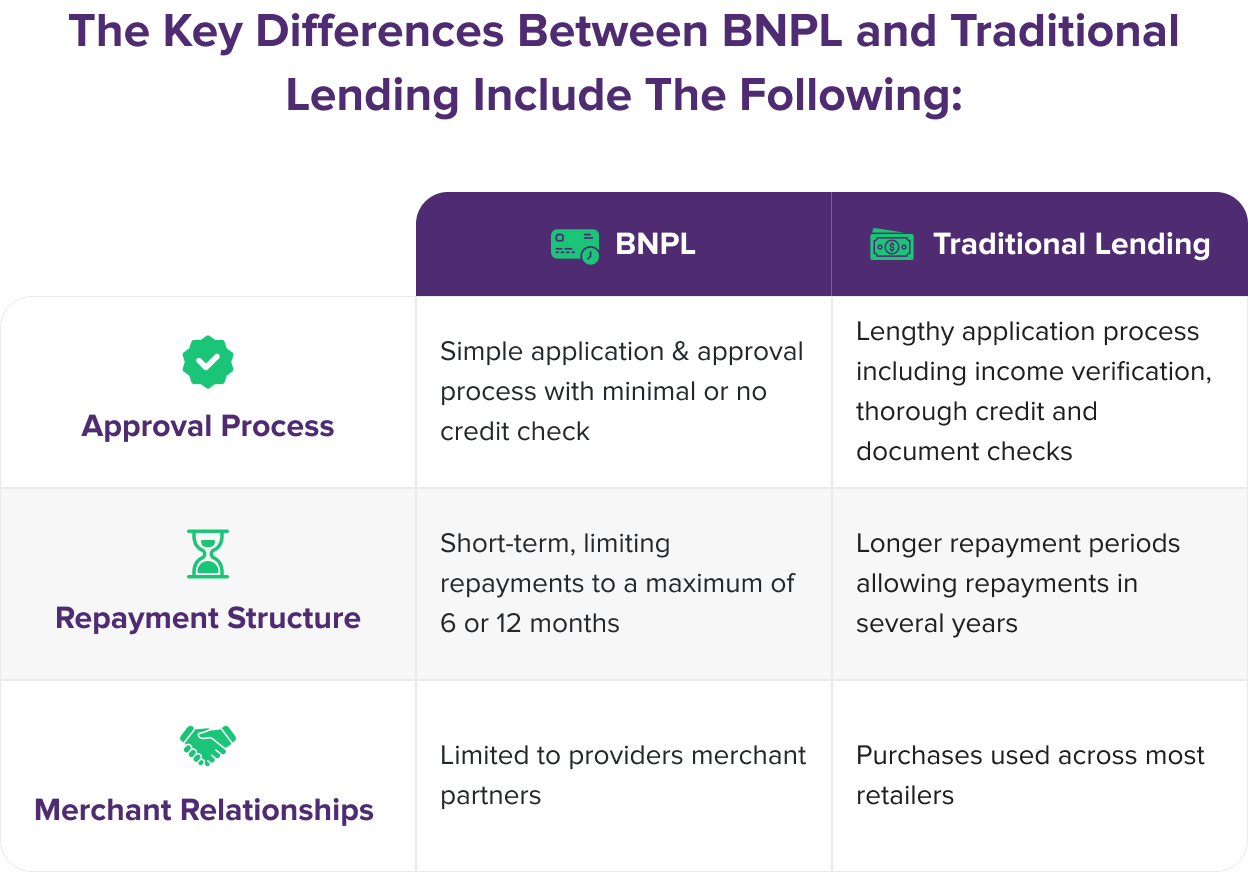

The key differences between BNPL and traditional lending include the following:

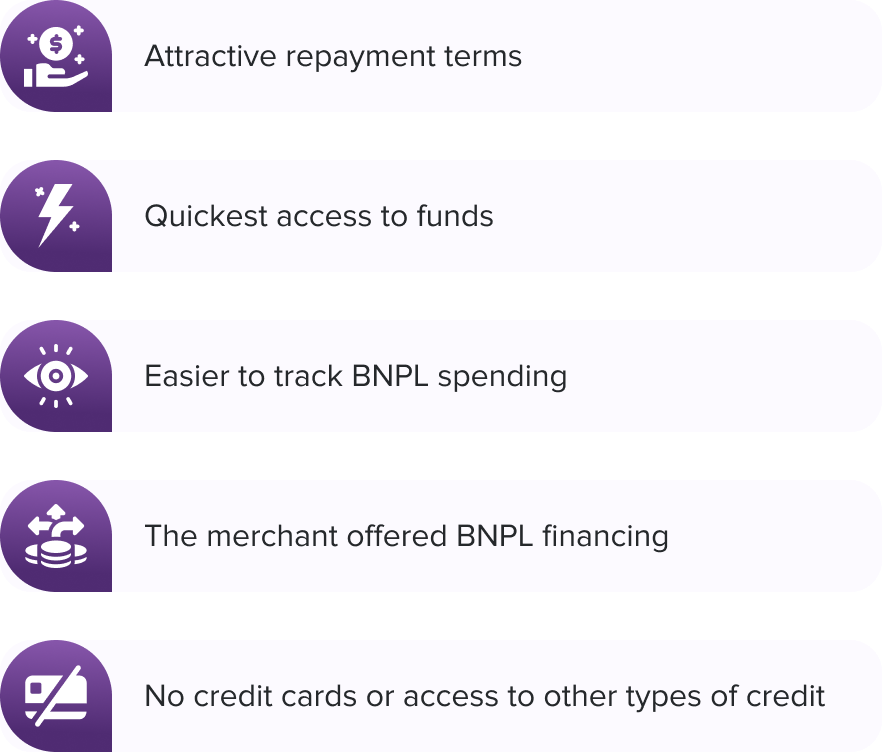

With easier access and more payment flexibility, BNPL is attracting more users, especially younger age groups. Lower interest rates, zero transaction fees, and fixed payments also appeal more to consumers who are averse to steep credit card charges and compounded interests.

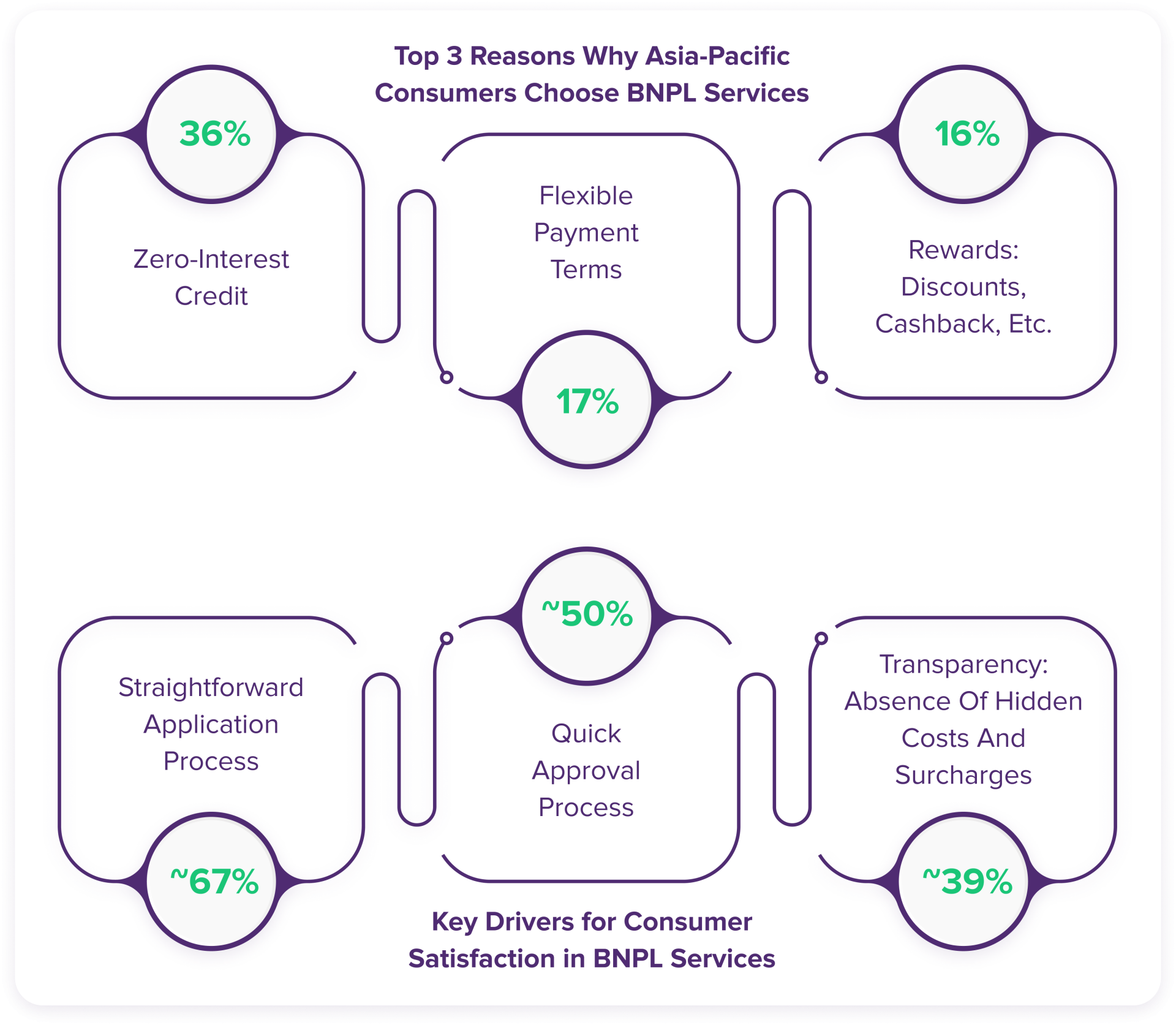

While there are significantly more credit card users than BNPL users, there is increased adoption of BNPL. A recent report on what impacts credit decisions also indicates that younger consumers prefer BNPL over credit cards and other payment options for the following reasons:

There is a positive outlook for the global BNPL market. It is forecasted to grow at 26.1% CAGR from 2023 to 2030. The growth would primarily be driven by consumer preference for more supple payment options and financial flexibility. BNPL integration with online checkout processes will also spur widespread adoption as consumers seek more seamless payment processes.

In terms of use, BNPL is more popular with younger consumers who have no credit histories or are averse to credit cards and debts. In the United States, the retail segment dominates the BNPL market, with more than 73% of BNPL revenue coming from retail purchases. Other market segments seeing growth in the BNPL market are healthcare, leisure and entertainment, and automotive.

In the Asia-Pacific region, we see increased use of BNPL payments from 1% of e-commerce transactions in 2020 to 4% in 2023. This increase puts BNPL transaction values at the same level as debit cards and twice as much as cash payments.

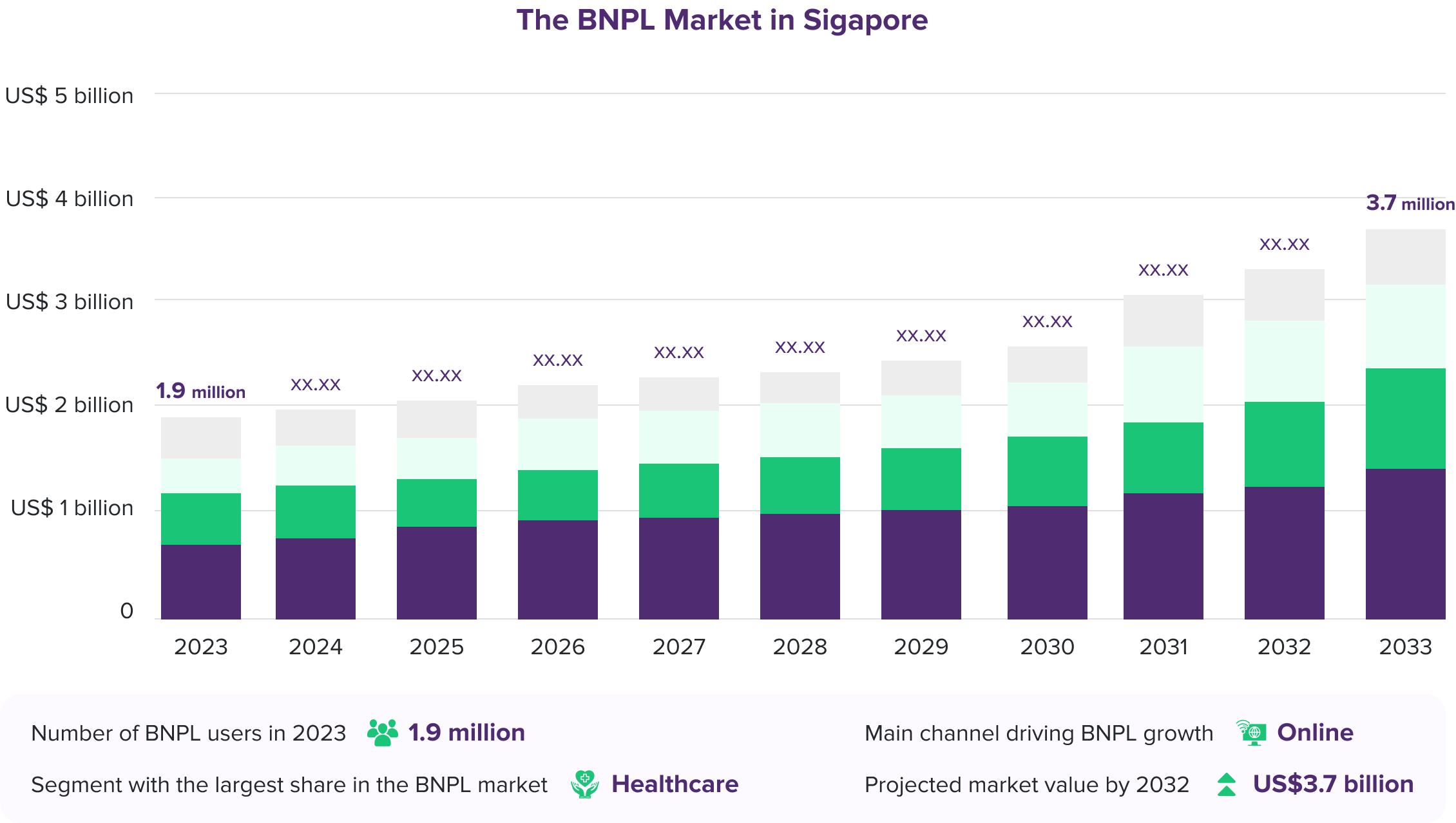

In Southeast Asia, Singapore was the first country in the region to offer BNPL payment options in 2017. By 2022, it already had 1.9 million BNPL users. Forecasted to be the only new digital payment to see a marked increase in e-commerce share, the BNPL market share in Singapore is expected to grow by 3% from 2022 to 2027.

Singapore has the most advanced payment systems in the world. On its path to a cashless society, the majority of consumers and merchants prefer using innovative payment systems , including digital wallets and BNPL. In fact, BNPL use in Singapore has seen steady growth in the past couple of years.

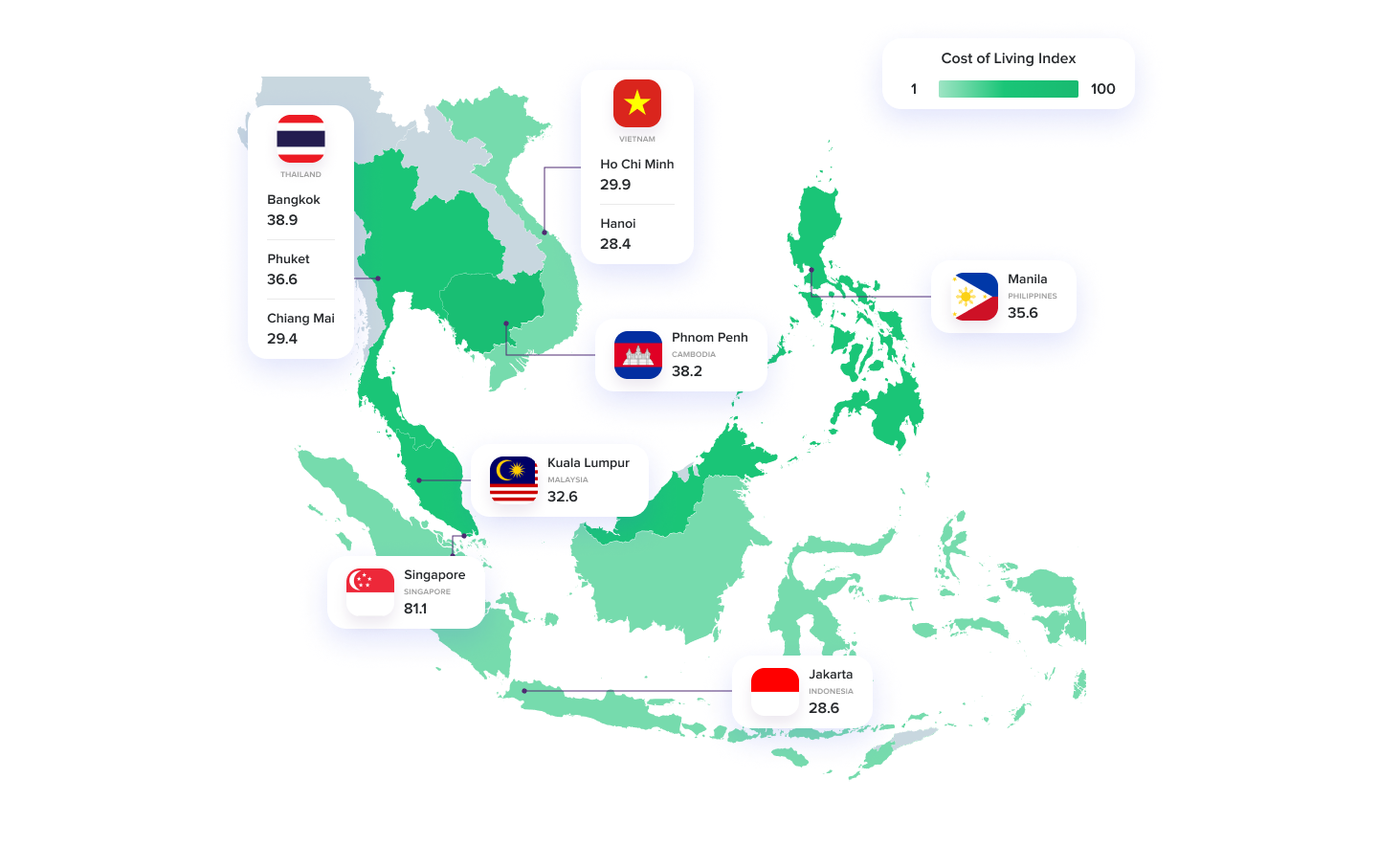

A report on the payment preferences of consumers in Singapore also reveals that 48% of purchases worth S$100 or less use BNPL. This indicates the popularity of such payment methods for smaller transactions.

Other factors that are driving growth in the Singapore BNPL market are:

The BNPL sector in Singapore has seen several mergers and acquisitions, liquidations, and dissolutions in the past couple of years. Pace filed for voluntary liquidation due to liabilities in 2023, just a year after it acquired Singapore BNPL frontrunner Rely. Early this year, ShopBack also discontinued its BNPL services in March 2024.

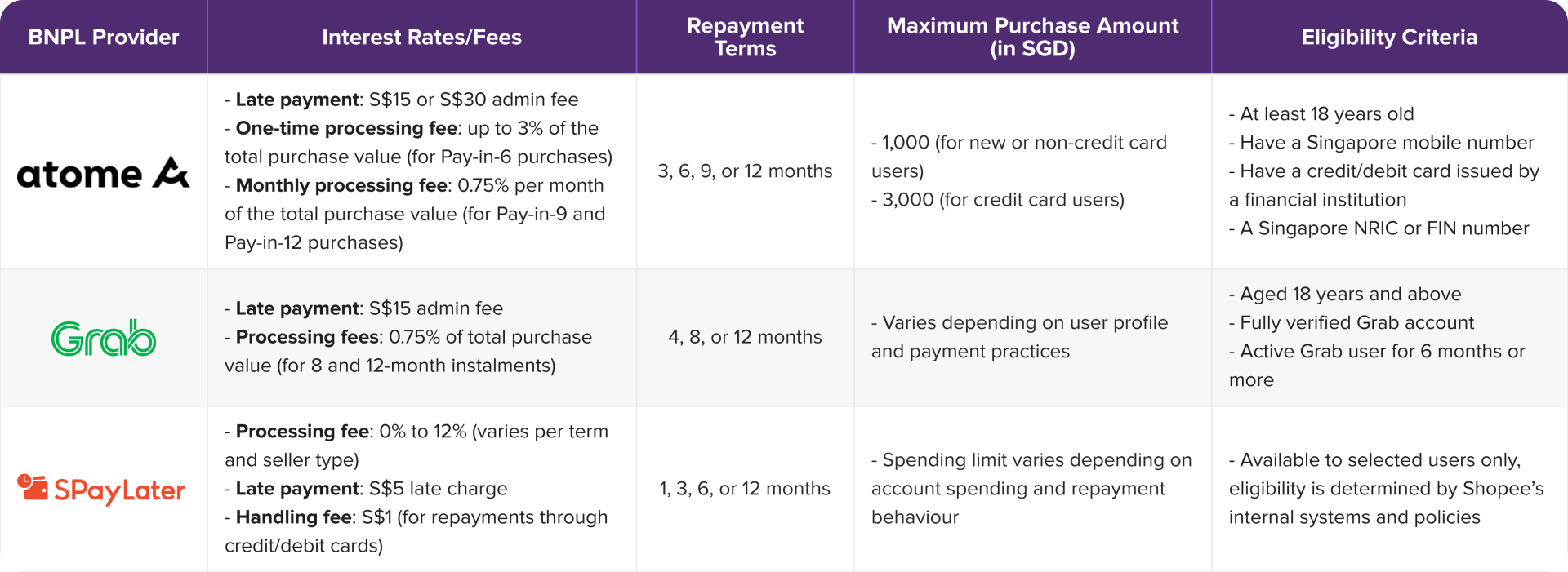

Still, a handful of BNPL providers remain strong and continue to attract new users. Leading the BNPL race in Singapore are Atome, GrabPay (Grab PayLater), and SeaMoney (SPayLater).

The majority of BNPL users today are under the age of 35. These young consumers often have no credit history and stable incomes as they are at a point in their lives when they are still building their careers. However, if ignored by traditional lending institutions, they can potentially reduce demand for traditional lending products in the future.

Today, BNPL usage is relatively lower than that of credit cards, but the average BNPL purchase is nearly 70% higher than that of the average credit card purchase.

Across all age groups, only 34% of consumers somewhat or completely trust BNPL services. To accelerate growth in the market, BNPL providers must implement strategies to earn consumer trust. This includes ensuring compliance with the BNPL Code of Conduct set by the Monetary Authority of Singapore.

For consumers, BNPL provides access to funds that can be used to meet immediate financial needs or to enhance cash flow management. However, they must exercise responsible spending and keep track of their purchases to avoid incurring huge debts across multiple providers.

Traditional lending institutions can continue to provide diverse options for consumers by expanding their service offerings to include those that are consumer-centric, financially inclusive, and transparent. By adopting these strategies, lenders can better meet the evolving needs of consumers and foster greater financial health and stability.

DISCLAIMER

This information herein is published by ROSHI Pte Ltd (UEN 202222480E) (“ROSHI”) and is for information only. This publication is intended for ROSHI and its clients to whom it has been delivered.

This report contains aggregated insights derived from various public sources including:

The analysis aims to provide perspectives on the Buy Now, Pay Later industry in Singapore and its developments and trends but may be incomplete or condensed. ROSHI makes no warranty to accuracy or assumes any responsibility for decisions made based on this report. Figures used are for illustration and do not bind ROSHI. ROSHI performs marketing and matchmaking services to connect clients with lending partners but does not directly offer any lending or financial advisory services under regulation by the Monetary Authority of Singapore. Users of this report should consult professional advisors before engaging in any transaction. This report is meant solely for insight purposes following Singapore laws and regulations around data privacy. Please contact ROSHI for authorization before reproducing or relying on the analysis.