HDB Flat Price Guide: What Type Can I Really Afford?

Fact-checked

Fact-checked

Click Image to Zoom

At a glance…

When you decide on a HDB flat as your place of residence, there are certain things you should take into consideration before deciding to purchase. You should be certain of your criteria for selecting the right HDB flat for you or your household.

Do you wish to purchase the largest flat you can afford comfortably? Or do you just want to live in the flat you have chosen until the Minimum Occupation Period (MOP) is over and you can sell it for profit? Would a 3-Room, 4-Room, or 5-Room flat be more suitable for you or your living conditions and financial situation?

When you take into account these factors, what kind of HDB flat can you really afford after all the calculations are done? The answer depends on your minimum monthly household income average, of course.

Now, how should you choose the right HDB flat that you can afford?

Here is an example on how you can calculate the probable type of HDB flat you can afford based on your minimum monthly household income average:

- Use the Sembawang February 2020 HDB BTO Launch prices (or any recent launch prices that include existing HDB flat types) as your point of reference.

- Ensure that you take into account the likelihood that you will be taking an HDB housing loan, and that you will need to put down a 10% downpayment.

- Don’t forget to apply the Mortgage Servicing Ratio of 30%.

- Make sure to calculate how much the Enhanced CPF Housing Grant will give you based on your household’s monthly income bracket.

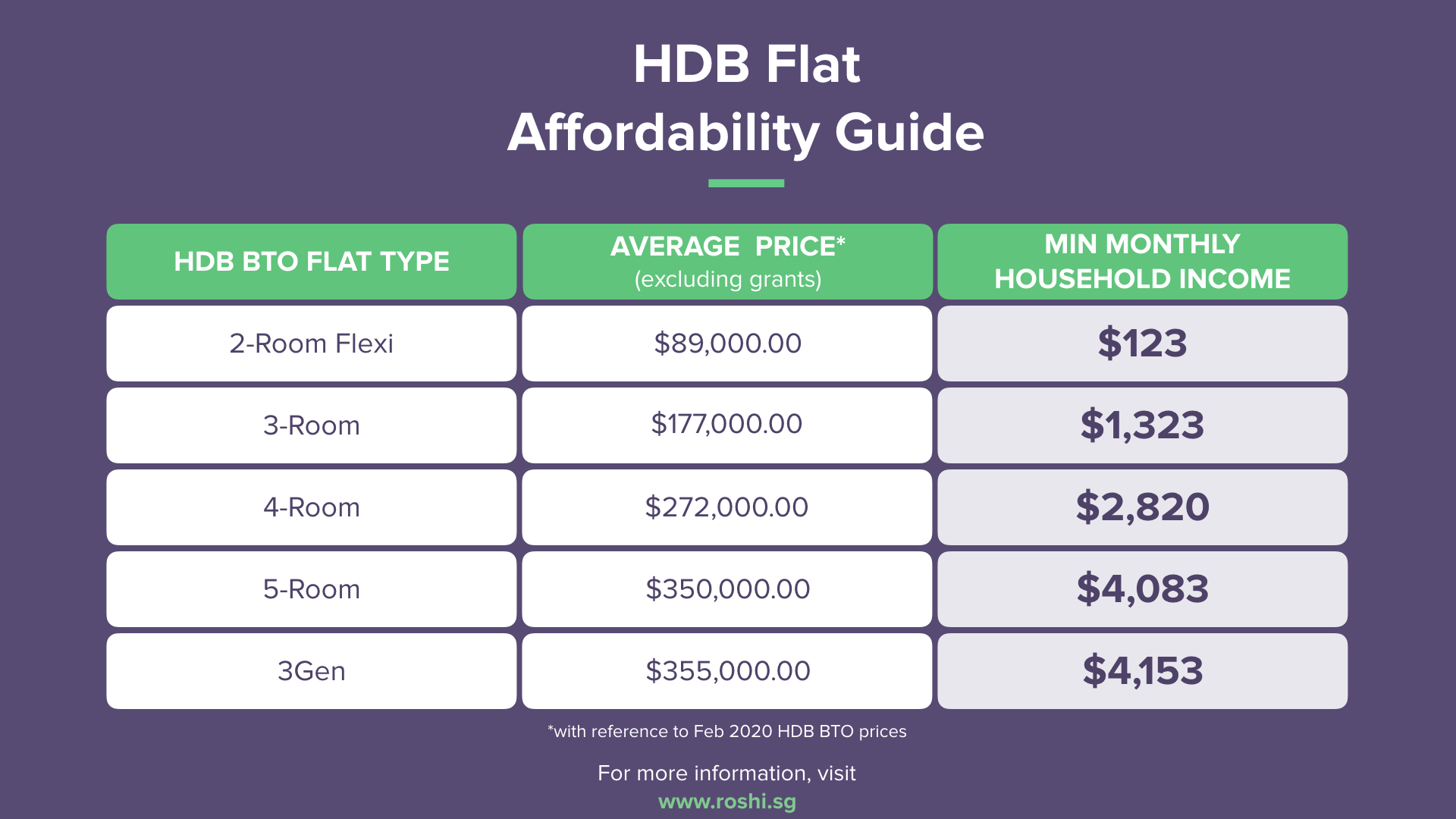

When you’ve taken all these into consideration, the likely outcome would be something like this table below:

| HDB BTO Flat Type | Average Price* (excluding grants) |

Min Monthly Household Income |

|---|---|---|

| 2-Room Flexi | $89,000.00 | $123 |

| 3-Room | $177,000.00 | $1,323 |

| 4-Room | $272,000.00 | $2,820 |

| 5-Room | $350,000.00 | $4,083 |

| 3Gen | $355,000.00 | $4,153 |

Still need a closer look at how you should choose the right HDB flat that you can afford?

Here’s a breakdown on the different aspects you should take into consideration.

What is the average cost of an HDB flat?

The average price of various HDB flat types such as a 2-Room Flexi, a 3-Room, a 4-Room, a 5-Room, or a 3Gen should be taken into consideration when deciding on the right HDB flat for you.

Besides that, the monthly household income holds an important part in your decision making scenario too. This is because the lower your household’s monthly income, the more grants you’ll potentially be able to receive. Thus, households with lower monthly incomes such as young couples or a small family with a pair of adults and two children will be likely to benefit from this.

For example, if your total monthly household income amounts to $2,500, then you will be able to qualify for $70,000 in EHG. On the other hand, if your monthly household income amounts to $6,000, then you will only be able to qualify for $35,000 in EHG.

What is the monthly mortgage amount you will need to pay?

If you leave aside the matter of whether a bank loan or HDB housing loan would be a better choice and only focus on the monthly mortgage, there are still aspects you will need to consider.

One of the aspects includes calculating how much you would be borrowing at an interest rate of 2.6% annum for 25 years after you’ve made the 10% downpayment.

For example, young couples who wish to keep expenses low or plan to upgrade to a larger property in the future while not planning to have children may be able to manage a monthly mortgage of $1,000 for a 3-room HDB flat.

This is based on the assumption that the monthly mortgage will be about 13% of a monthly household income that amounts to $6,000.

Based on your monthly income, what type of HDB flat should you choose?

So then, to measure what type of HDB flat would suit your financial planning and monthly income, you will need a realistic way to evaluate how much you can actually afford.

You can use the Mortgage Servicing Ratio (MSR) which caps the amount you could potentially spend on mortgage repayments to 30% of your gross monthly income.

If the MSR is more than 30% of your gross monthly income, then perhaps you might need to reconsider your options.

With that in consideration, you are likely to be able to afford a 2-room flexi or 3-room HDB flat without straining your finances. However, if you want a 4-room HDB, a 5-room HDB, or even a 3Gen HDB flat, then your minimum household income will need to be higher to pay off your monthly mortgage. Otherwise, it is best not to aim for a HDB flat that doesn’t suit your monthly household income.

Considerations

If you decide on using an HDB housing loan to service the mortgage, you will be using your monthly CPF contributions to pay for the monthly mortgage. For example, you could be using the CPF of one household income contributor to make payments for the HDB housing loan, which could be risky.

As such, you might encounter a situation wherein your monthly CPF contribution is not sufficient in covering the cost of your monthly mortgage.

While you may be able to top-up your CPF payments in order to afford the HDB flat of your dreams, it is not very advisable unless you are using passive income (such as from renting property) and not money from your monthly household income.

This way, should you encounter unfortunate circumstances such as losing your source of income, your finances won’t suffer as much in the long run.

To sum it up, when selecting the right kind of HDB flat that you can afford comfortably, you should always take into account certain factors such as the size of the flat and its average cost, the monthly mortgage you will need to pay off, and how much you can spend based on your monthly household income.

When you take into account these factors, the kind of HDB flat your finances can really afford after all the calculations are done will be clear to you.

Latest Mortgage Rates

Below tables present the latest mortgage rates from various lenders, including both fixed and floating options. Use this table as a starting point to explore available home loan options and prepare for your next steps.

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 01 June 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 01 June 2026