Understanding Mortgage Board Rate (MBR): What is it & How Does it Work?

Fact-checked

Fact-checked

At a glance

Mortgage Board Rates (MBR) in Singapore can offer advantages and disadvantages for potential homebuyers. While they can provide lower initial interest rates and stability than other loan packages, there are also significant downsides. Some critical disadvantages are that MBR rate calculations are unknown to the public, and the bank can change rates with minimal notice. However, they remain a relevant choice for some people in the Singapore housing loan market. This article provides a detailed explanation and breakdown of the pros and cons of MBR-pegged home loans, specifically focusing on OCBC Bank’s Mortgage Board rates and home loan packages.

Introduction

The OCBC Mortgage Board (MBR) falls under the umbrella of floating rates. It’s a reference rate set internally by the bank and can fluctuate according to certain benchmarks. Imagine a home loan put together by the bank, accompanied by its terms and conditions. That’s what the MBR is about.

OCBC offers comprehensive mortgage plans suitable for both HDB and private properties. One standout feature of OCBC home loans is their universal application, regardless of property type. They have three main home loan types: fixed rate, floating rate (tied to SORA) and floating rate (linked to board rate).

Discussing OCBC MBR: What you need to know

The OCBC MBR is a rate set and managed by the bank, influencing your home loan interest rates. Its adjustment is entirely up to OCBC, and they are not bound to provide any rationale behind rate changes.

This indicates that market conditions don’t directly influence the MBR. OCBC can adjust the board rate upwards or downwards as they deem fit. The exact mechanisms behind these rates remain elusive, which causes some potential homeowners to be wary. However, there are some instances when the rate can be pretty appealing.

On their end, OCBC only needs to provide a 30-day heads-up in case of any rate change. If customers are unsatisfied, they can switch plans without any penalty.

Important Info

As of Aug 2023, the prevailing OCBC rate is approximately 2.80%. However, you should look for the latest bank or mortgage broker rate. A unique code identifies each OCBC package in their Letter of Offer. Remember, the displayed rates might differ from what’s available online or to other customers.

Key features of MBR

The loan lock-in period period of the MBR is two years. You can also opt for partial prepayment during the lock-in period of 2 years. Here are the important standard fees that OCBC charges which you need to know:

| Loan Type | Full Redemption Penalty | Partial Repayment Penalty | Cancellation Fee |

|---|---|---|---|

| OCBC Mortgage Board Rate | 1.5% | No fees if the outstanding balance is more than 50% of the loan principal. Otherwise, the bank charges 1.5% as a fee | 1.5% |

For all OCBC home loans in Singapore, there is a minimum borrowing amount of $200,000 for HDB and $300,000 for private estates.

The mystery behind MBR rate calculation in Singapore

If you want to know how the MBR is calculated, guess what? No one knows. Not even the mortgage bankers or their direct superiors have any idea. It’s only the upper echelons of bank management who have any clue. And the way to calculate these rates is never revealed to the public, so no one actually knows when the following rate will change. However, historical trends suggest a correlation between MBRs and global interest rates. MBRs generally increase with increasing global interest rates. But it’s surprising to note that the opposite does not always happen. That means when the interest rates decline, the MBR rate does not fall proportionally.

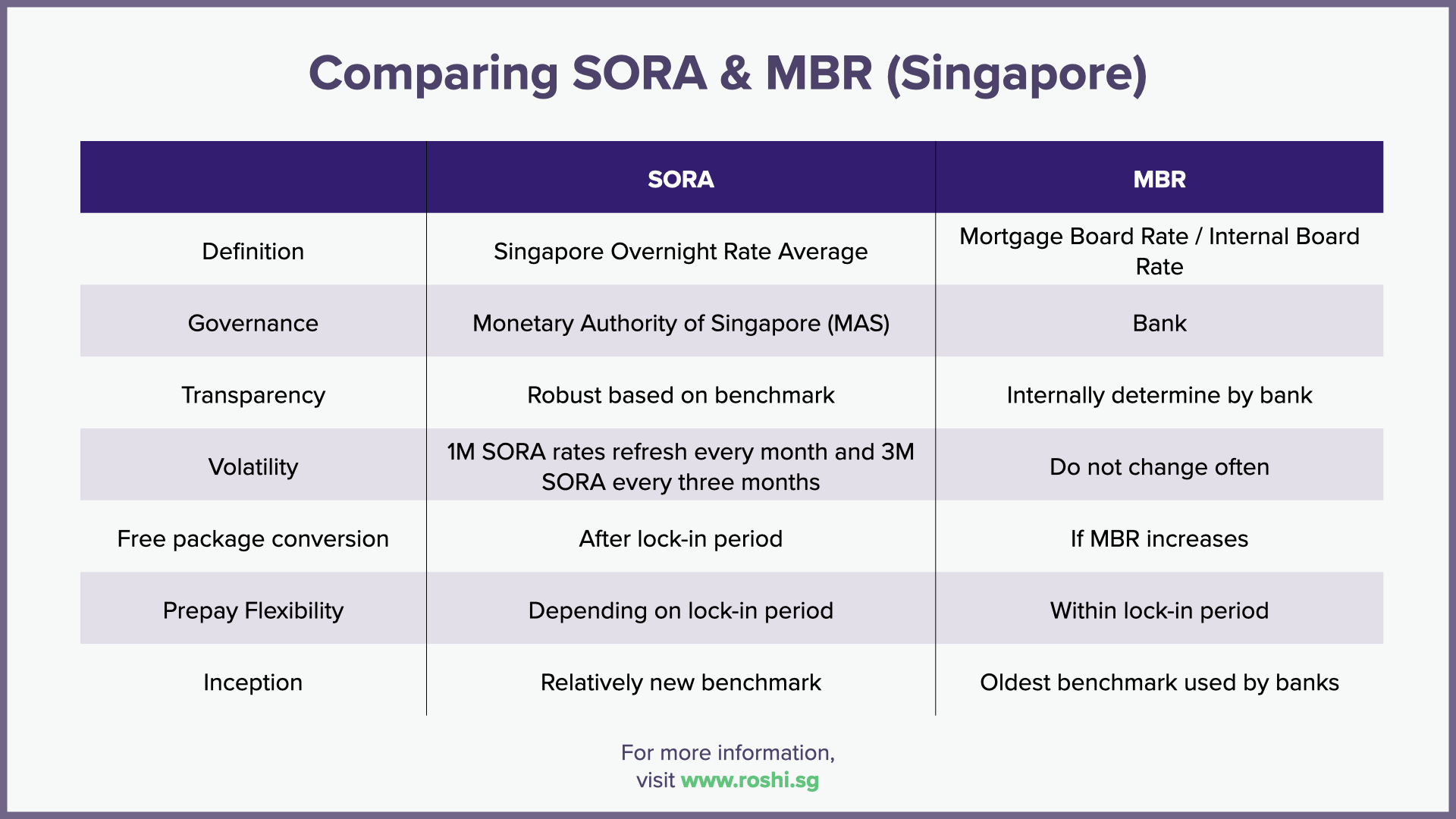

Comparing OCBC MBR and SORA

Floating home loan packages with OCBC bank are pegged to either MBR rates or SORA. When the MBR or SORA increases or decreases, the floating rates will change accordingly. Here is a quick snapshot comparison:

| Key Factors | SORA | OCBC MBR |

|---|---|---|

| Definition | Singapore Overnight Rate Average | Mortgage Board Rate / Internal Board Rate |

| Governance | Monetary Authority of Singapore (MAS) | Bank |

| Transparency | Robust based on benchmark | Internally determine by bank |

| Volatility | 1M SORA rates refresh every month and 3M SORA every three months | Do not change often |

| Free package conversion | After lock-in period | If MBR increases |

| Prepay Flexibility | Depending on lock-in period | Within lock-in period |

| Inception | Relatively new benchmark | Oldest benchmark used by banks |

So, what advantages do MBR rates hold for the homeowner?

Often referred to as “the bank’s own rate”, the MBR pegged home can emerge as the optimal choice for potential homeowners. Here are some key benefits:

1. Lowest interest rates

MBR rates can offer the most competitive interest rates for home loan packages. While there’s always a possibility of interest rates revised at any given time, banks have frequently kept the MBR relatively low during the first few years of a loan. This strategy is an attractive lure for prospective clients.

2. More stability

Homebuyers who look at floating-rate home loan packages might find the bank’s board rate appealing. Unlike market benchmarks, such as the SORA rate, susceptible to more volatile market shifts, board rates don’t experience frequent adjustments. Banks can modify board rates whenever they see fit, but the general tendency is to maintain stability to preserve the trust of clients who opt for MBR-pegged home loan packages.

3. Prepayment flexibility

As interest rates tend to rise over time, homeowners often look for strategies to reduce their outstanding amounts sooner. Recognising this, OCBC bank allows borrowers the flexibility to prepay up to 50% of the remaining loan amount during the lock-in period for its floating rate home loans pegged to either SORA or the board without imposing any penalty. This feature is invaluable for homeowners aiming to lessen their financial burdens.

4. Free interest rate conversion during lock-in

Free package conversion is a facility some banks provide, allowing clients to switch to another existing package without the typical conversion fees. Generally, this option is available when the lock-in period ends. Such an offer is an attractive incentive, especially when interest rates are expected to climb post-lock-in.

Nevertheless, OCBC sets itself apart with free package conversion for its MBR-pegged floating-rate home loans, even if the board rate rises during the lock-in period. This provision offers a safety net for homebuyers hesitant about aligning their home loan with the often non-transparent mortgage board rate. When the board rate increases, borrowers can transition to another OCBC home loan package at no extra cost. This flexibility is a massive advantage in an environment with constantly escalating interest rates.

What are the drawbacks of MBR-pegged home loans?

MBR-pegged home loans receive a lot of skepticism from home buyers. Many have had poor experiences with them, leading to their poor reputation. Some banks strategically rebrand mortgage board rates under various names to complicate matters. Sometimes, they are referred to as “prime rates” or “variable rates”, which distracts borrowers from their real purpose. Here are some of the critical disadvantages potential borrowers must know:

- Lack of transparency

The main drawback of MBRs is their inherent need for more transparency. High-ranking bank officials determine the entire decision-making process and not known to anyone else. Therefore, both clients and mortgage brokers are in the dark about the way to calculate these rates. Many banks also opt not to publicly disclose their MBRs, so customers can only ascertain the current rate by checking with the bank.

- Unpredictable fluctuations

The unpredictable nature of MBRs is another cause for concern. Banks retain the authority to modify their board rate whenever they deem fit, without any obligation to provide a rationale to borrowers. This flexibility means that some banks might choose to adjust home loan interest rates frequently, even monthly. Although rapid changes are not standard practice, they remain a possibility. So, potential borrowers face the challenge of timing the exact moment to commit to an MBR-pegged home loan.

For instance, consider two individuals with an MBR-pegged home loan from the same bank but at different times, one in February 2022 and the other in November 2022. They might have differing interest rates. Moreover, one person’s rate may increase without affecting the other’s, leading to confusion and unpredictability.

- No advance warning on MBR hikes

To add to these issues, banks only need to provide a mere 30-day notice before altering their mortgage board rates. For individuals diligently trying to plan their finances, such short notice can be disruptive and unwelcome.

In light of all these disadvantages, borrowers need to consider the stability of the bank’s rates before choosing an MBR-linked home rate.

Should I choose a mortgage board rate home loan in Singapore?

The allure of mortgage board rates often lies in their competitively low rates, specifically designed to attract potential borrowers. But beyond this obvious advantage, there are specific scenarios where choosing an MBR-pegged home loan can be beneficial.

- Selling the property soon:

An MBR-linked loan might be the ideal choice if you plan to sell your property shortly. Some banks offer terms that allow borrowers to either sell their property or make full or partial repayments without any penalties during the lock-in period. However, it’s worth noting that this lock-in period is typically only relevant if you are considering refinancing your home loan with a different bank.

- Closely monitoring the market

For those with a keen understanding and close monitoring of the property market, taking on the internet risk of floating rates such as the MBR can be a strategic move. Mortgage board rate-linked loan packages provide flexibility that lets borrowers swiftly switch to a different loan package. Thus, for market aficionados who remain updated on the latest trends and shifts, these lock packages are an opportunity to capitalise on their insights.

- Anticipating financial inflows or not requiring a long-term loan:

If you foresee a substantial monetary inflow shortly or don’t require a long-term loan, then an MBR-pegged loan can be a viable choice. For instance, if you’re expecting a considering sum through sources like rental income or annual bonuses, utilise this amount to pay off a significant portion of the loan. That can be a wise financial decision.

Additionally, for those not seeking long-term loans, the typically lower interest rates associated with board rates make them an attractive option.

Conclusion

Sometimes, opting for an MBR-linked home loan might be your sole option. This could be due to the lack of available alternatives, with only a specific bank willing to offer you a housing loan.

Ultimately, mortgage board rates have an enduring presence as a home loan choice in the Singapore property landscape. Despite a recent dip in their popularity, it’s unlikely that Singaporean banks will entirely phase them out. The flexibility banks enjoy in setting these rates is a huge incentive to continue rolling MBR home loans out.

For the homeowner, the key is to choose the home loan that’s best for your financial circumstances. Whether it’s OCBC MBR pegged home loans or other home loans, compare them with Roshi’s loan platform first. Or contact us to find the choice that complements your financial standing.

Latest Refinance Rates

The following tables offer a comprehensive look at today’s refinance rates, featuring competitive rates from established banks. From fixed-rate refinance loans to floating options, these figures represent current rates in the market.

Refinancing Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.85% |

*Today's Mortgage Rates - 25 May 2026

Refinancing Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| SBI | 2 years | 1.88% |

*Today's Mortgage Rates - 25 May 2026

Refinancing Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| Standard Chartered | 2 years | 1.65% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 2 years | 1.80% |

| Bank of China | 2 years | 1.84% |

| OCBC | 2 years | 1.84% |

*Today's Mortgage Rates - 25 May 2026

Refinancing Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 2 years | 1.80% |

| OCBC | 2 years | 1.84% |

| Promotion | 2 years | 1.99% |

*Today's Mortgage Rates - 25 May 2026