3M SORA or 1M SORA? All You Need to Know about SORA Rates

Fact-checked

Fact-checked

Click Image to Zoom

At a glance...

On 2 February 2021, Mr Leong Sing Chiong, Deputy Managing Director at the Monetary Authority of Singapore (MAS), announced during his keynote speech that the Singapore Overnight Rate Average (SORA) would be adopted as the new benchmark for interest rates for SGD financial markets by the end of the year.

For the layman: banks use these benchmarks to set the interest rate that they charge for loans. Because interest rate benchmarks can fluctuate from day to day, home loan interest rates change all the time. If you’re looking to get a home loan or a refinance home loan, it’s important to understand what the benchmarks mean and keep an eye on them.

What is SORA, and What Difference Does the Transition Make?

SORA is administered by MAS and is determined by the average rate of all transactions traded and booked in the unsecured overnight interbank SGD cash market in Singapore between 8 am and 6.15 pm.

MAS performs the computation at the end of every business day, and the SORA rate is then released on the MAS website by 9 am on the following business day. The calculation methodology is also regularly reviewed by MAS to ensure that it represents the actual interest rate well and adheres to the International Organisation of Securities Commissions (IOSCO) Principles for Financial Benchmarks. By meeting this international best practice standard, adopting SORA generates stronger confidence in the Singapore market among both local and foreign players.

Before SORA, the previous interest rate benchmark had been the Singapore Interbank Offered Rate (SIBOR). SIBOR was tied to the interest rates that banks charge to one another when they borrow money on the Singapore interbank market. However, this involved a more complicated system of ranking banks and then removing the top and bottom quartiles. SIBOR had, in turn, been an alternative to the Swap Offer Rate (SOR).

The transition to SORA was recommended in a consultation report by three major financial industry groups – the Association of Banks in Singapore (ABS), the Singapore Foreign Exchange Market Committee (SFEMC) and the Steering Committee for SOR Transition to SORA (SC-STS).

What are the 1M and 3M Compounded SORA Rates?

The historical SORA rates published daily on the MAS website are typically compounded with a compounding period of 1 month (1M) or 3 months (3M).

For a 1M compounded SORA rate on 4 February 2022, the daily SORA rates from 4 January 2022 are compounded over the next month.

Meanwhile, for a 3M compounded SORA rate on 4 February 2022, the daily SORA rates from 4 November are compounded over the next three months.

1M vs 3M SORA Rates: Which is Better?

Whether the 1M or 3M compounded SORA rate is better (lower) depends on many different factors. A good way to tell is to look at Singapore’s economic indicators, such as inflation rates (CPI or PPI indexes), unemployment levels and the SGD dollar value. These indicators give information on how the SORA rate might have changed in the past few months.

If the interest rate has been on an increasing trend, the 3M SORA rate would give a lower cost of borrowing since the lower past historical rates are included in the compounding. On the flip side, if the interest rate has been on a decreasing trend, the 1M SORA rate would give a lower cost of borrowing since only the more recent daily rates are taken into account.

Why is SORA Replacing SOR and SIBOR?

Talks to replace SIBOR began in December 2017. Following the global financial crisis in 2008, banks were subjected to some regulatory adjustments. These new rules had the effect of banks being less reliant on borrowing from one another as a funding source.

In July 2020, a computation methodology for the new interest rate benchmark was proposed, incorporating corporate deposit transactions. However, this methodology still required banks to exercise some expert judgment, albeit to a lesser extent. Year-long testing revealed that this way of computing the benchmark—while relatively robust—was more volatile than the SIBOR rate. It also did not track movements in SIBOR as closely as expected. The high volatility of this proposed benchmark rate would have made it unsuitable for end users.

As a result, the new proposed benchmark was evaluated to be unsuitable to replace SIBOR directly as extensive amendments to existing SIBOR-based financial contracts would be required. This process was deemed to be highly complicated and resource-intensive.

Meanwhile, the derivatives market had been steadily transitioning from SOR to SORA. In light of this, moving SGD financial markets to a single rate regime based on SORA was deemed to be a better strategy than rolling out two separate benchmark transitions for SOR and SIBOR.

SORA is based on the principle of a deep and liquid overnight interbank funding market. Basing the benchmark on SORA will thus improve liquidity while simultaneously achieving a better positioning for the SGD financial markets in future.

The SIBOR-to-SORA transition, in particular, will allow participants to enjoy enhanced market efficiency. Retail consumers, SMEs and other users of SGD floating-rate products which currently take reference from SIBOR will also benefit from greater transparency and a more competent market.

SC-STS is committed to developing SORA-based solutions and products that will not only meet the needs of all SORA users but also ensure a smooth transition for current SIBOR users.

When will SOR be Discontinued?

SOR used to be a key reference rate for SIBOR, but due to its high volatility, it has already been completely phased out and replaced with SORA. Home loans that were previously based on SOR interest rates have since been converted to SORA packages. The last home loan based on SOR was taken off the market in July 2017.

SOR relies on the USD London Interbank Offered Rate (LIBOR) for its computational methodology. However, the Financial Conduct Authority (FCA) announced that LIBOR would be discontinued in mid-2023. Thus, SOR is also expected to be discontinued in mid-2023.

All financial institutions and their consumers were thus notified to terminate the use of SOR in new derivative contracts by mid-September 2021. The only exceptions in which SOR could still be used were for specified purposes related to the transition and risk management of legacy SOR arrangements to SORA.

When will SIBOR be Phased Out?

The long-term 6-month SIBOR was phased out on 31 March 2022. The more widely used 1-month and 3-month SIBOR rates would follow by the end of 2024. SORA will be used as the key interest rate benchmark in SGD financial instruments moving forward.

When will SIBOR be Discontinued?

While there is no clear indication of when SIBOR will be fully discontinued, the consultation report had recommended that all financial institutes and their consumers discontinue the use of SIBOR-related financial products in new contracts by mid-September 2021. During that transition period, many banks began launching SORA packages alongside SIBOR home loans. This helped to educate customers on the new benchmark rate, how it operated and how it would impact them.

What are the Differences Between SIBOR and SORA?

SIBOR and SORA are similar in that both measure the Singapore interbank lending interest rate for unsecured loans. However, the two benchmarks have some key differences.

SIBOR is a theoretical rate, meaning that it incorporates “term” or “credit” risk components. Unlike SIBOR, SORA is based on actual transactions, making SORA more transparent and less volatile.

Another difference is that compounded SORA is a backward-looking overnight rate. It is based on the volume-weighted average of all recorded transactions of interbank loans that have already been carried out. Meanwhile, SIBOR (and SOR) are forward-looking as they consider future estimated lending rates.

A 3-month compounded SORA (most likely to be used by banks for future home loans) will always be more stable and predictable because it is controlled by SORA rates in the past 90 days. When using SIBOR, however, users can be hit by unexpected spikes in the interest rate as banks (or other financial institutions) can increase interest rates without warning.

What are the Benefits of a SORA-Based Interest Rate Benchmark?

SORA was recommended by the consultation group for the following reasons:

- SORA facilitates more transparency in home loans, with volatility comparable to SIBOR.

- SORA allows easier comparison of loan pricing and lower risk to banks as different financial products do not have to use different reference rates.

- Access to long historical data (published since 1 July 2005) allows technical analysis and demonstrates trends for asset-liability pricing, risk management and trading purposes.

- Compounded SORA is significantly more stable when compared to SOR rates, which generally depended on idiosyncratic market elements on a single day.

- Computation of SORA is based on banks’ transactions that do not require any expert judgment, making SORA more sustainable.

- Use of SORA, particularly in derivatives, is aligned to the new best practices in other key global financial markets.

- Availability of SORA-based derivatives will benefit cash market products utilising compounded SORA as the reference rate, such as loans and bonds.

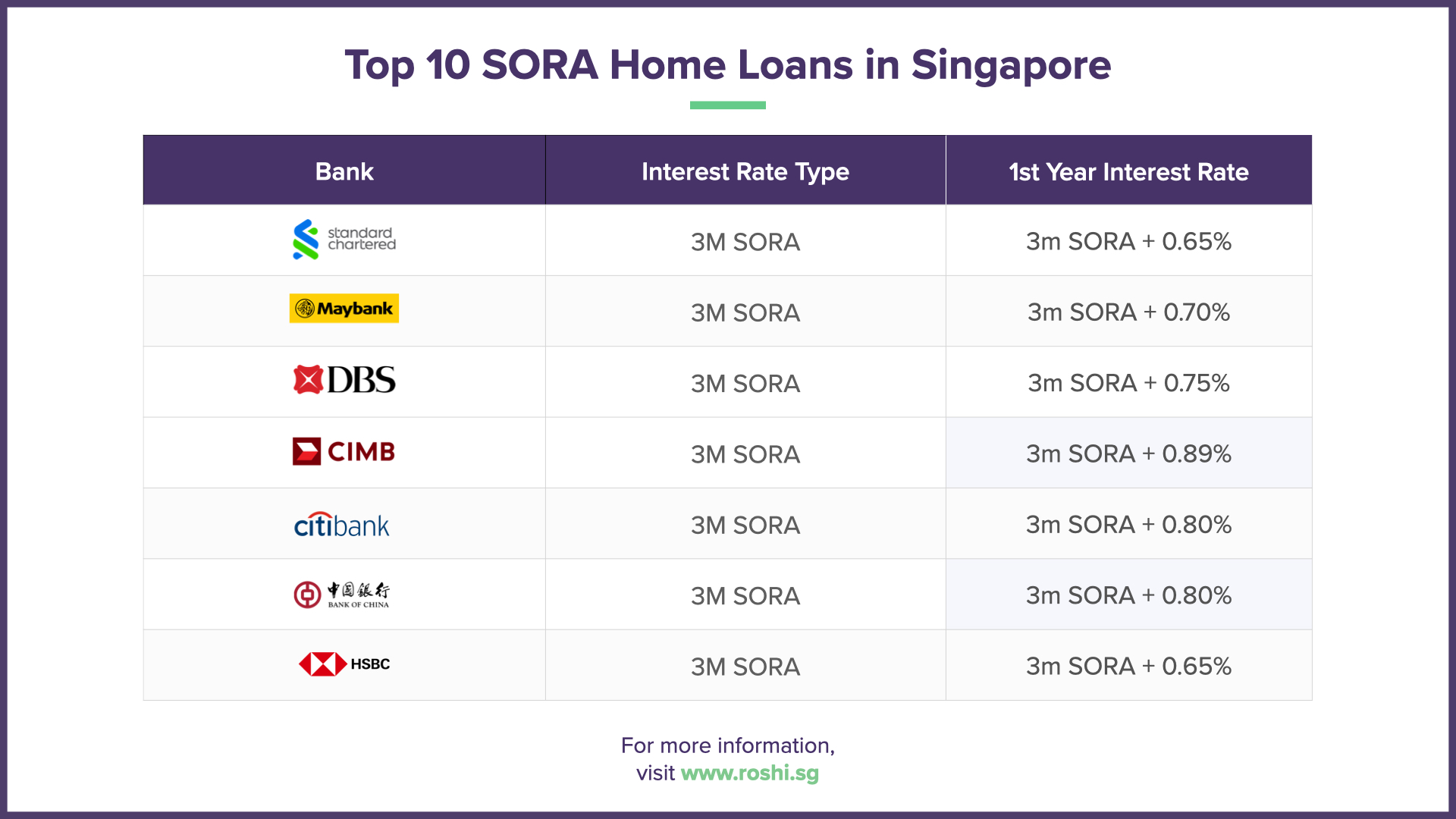

Which Banks in Singapore Offer 1M SORA and 3M SORA Home Loans?

Most banks have already launched SORA-pegged home loans. As banks start to explore the new housing loan options based on the SORA regime, homebuyers can expect a wider variety of home loan choices in the next few years.

Here is a list of the banks offering the top 10 SORA home loans in Singapore:

| Bank | Interest Rate Type | 1stYearInterest Rate |

|---|---|---|

| SCB | 3M SORA | 3m SORA + 0.65% |

| Maybank | 3M SORA | 3m SORA + 0.70% |

| DBS | 3M SORA | 3m SORA + 0.75% |

| UOB | 3M SORA | 3m SORA + 0.80% |

| CIMB | 3M SORA | 3m SORA + 0.80% |

| Citibank | 3M SORA | 3m SORA + 0.80% |

| Bank of China | 3M SORA | 3m SORA + 0.80% |

| HSBC | 1M SORA | 1m SORA + 0.65% |

As you can see, the most common home loan package currently offered is the 3M SORA floating home loan rates package. This means that your interest rate will only be refreshed once every three months. Banks will be releasing more SORA-related products this year.

Today's Mortgage Rates

The following tables offer a comprehensive look at today’s mortgage landscape, featuring competitive rates from established banks. From fixed-rate mortgages to floating options, these figures represent current rates in the market.

Fixed Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Bank of China | 2 years | 1.55% |

| Bank of China | 3 years | 1.60% |

| Bank of China | 2 years | 1.60% |

| Maybank | 2 years | 1.60% |

| Bank of China | 3 years | 1.65% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Promotion | 3 years | 1.85% |

*Today's Mortgage Rates - 21 May 2026

Fixed Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Maybank | 2 years | 1.60% |

| Promotion | 2 years | 1.75% |

| Promotion | 2 years | 1.80% |

| OCBC | 2 years | 1.80% |

| DBS | 3 years | 1.85% |

| Hong Leong Finance | 3 years | 1.85% |

| Hong Leong Finance | 2 years | 1.85% |

| Promotion | 2 years | 1.85% |

| Promotion | 3 years | 1.85% |

| DBS | 3 years | 1.90% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (Private Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 0 year | 1.60% |

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| RHB | 0 year | 1.70% |

| OCBC | 2 years | 1.70% |

| Bank of China | 0 year | 1.74% |

| DBS | 0 year | 1.79% |

*Today's Mortgage Rates - 21 May 2026

Floating Rates (HDB Properties)

| Bank | Lock In Period | 1st Yr Interest |

|---|---|---|

| Promotion | 2 years | 1.60% |

| OCBC | 2 years | 1.65% |

| RHB | 2 years | 1.65% |

| Standard Chartered | 2 years | 1.65% |

| Maybank | 2 years | 1.68% |

| OCBC | 2 years | 1.70% |

| DBS | 0 year | 1.79% |

| RHB | 2 years | 1.79% |

| Standard Chartered | 0 year | 1.80% |

| Standard Chartered | 2 years | 1.80% |

*Today's Mortgage Rates - 21 May 2026